This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

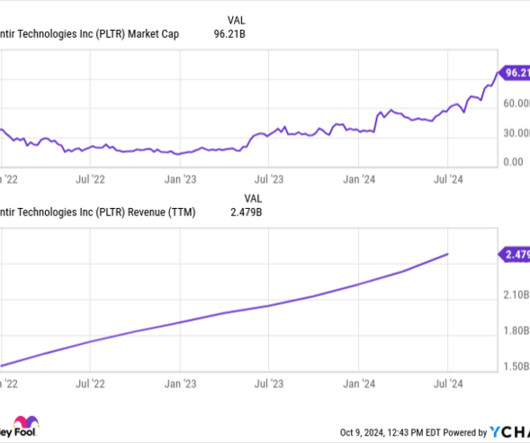

For example, high-profile investmentbanks such as JP Morgan or Wells Fargo could begin covering the stock from an equity research perspective. If more analysts from Wall Street's largest banks begin to regularly report on Palantir and its prospects, the company has a good chance to land on more investors' radar.

Discover the advantages of a relationship bank providing leverage on both fund and portfolio level, optimizing your investments for maximum returns. They enhance Internal Rate of Return, provide funding certainty in competitive situations, or cater for additional investments.

Axial is excited to release its Q3 2023 Lower Middle Market InvestmentBanking League Tables. These quarterly league tables reveal the top 25 investmentbanks active on the Axial platform in Q3. In Q3, 571 sell-side investmentbanks and M&A advisors brought a total of 2,360 deals to market.

Oak Hill Advisors (“OHA”) served as a Lead Arranger for the unitranche financing to fund Bain Capital Private Equity’s (“Bain Capital”) acquisition of Harrington Industrial Plastics (“Harrington”) from Nautic Partners.

Union Square Advisors, a technology-focused investmentbank, is expecting to see an increase in technology sector deal-making in 2024, with recent positive momentum continuing over the course of the year.

One item of note is that while technology was ranked only the fourth highest industry as it relates to total dealflow in Axial in 2023, deals in the tech sector had the leading pursuit rate at 8.92%.

Importantly and atypically, over half of our Q1 debt brokerage dealflow was on non-multifamily assets in retail, hospitality, industrial, and office. If banks simply extend loans because they are performing and the bank is making SOFR plus 300, for example, there will be no 2024 refinancing of that loan.

We're committed to getting these right, and we look to self-fund the necessary investments to do so. The rebound in Banking gained speed during the quarter, led by near-record levels of investment-grade debt issuance as improved market conditions enables issuers to pull forward activity. Turning to the quarter.

Seneca Partners was formed in 1999 as a merchant bank, doing both investmentbanking and investing into privately held companies. In 2003, we formed Seneca Health Partners, a small, committed healthcare fund focused on growth stage investing. We will work on transactions with $3M-20M+ of EBITDA.

We also expanded Zelman's investmentbanking capabilities into the commercial market in 2023. And in the fourth quarter, the investmentbanking team closed three transactions, albeit all in the single-family sector, that boosted revenues and expanded the W&D brand significantly. billion of bridge business.

Investmentbanking revenue of 1.6 Gross investmentbanking and markets revenue of 924 million was up 32% year on year, primarily reflecting increased capital markets and M&A activity. So, the hope and expectation of continued rebound in the investmentbanking wallet and our share of that is part of that.

Limited partners are gravitating towards Independent Sponsors given their lower management fees, and the flexibility that comes with co-investing on a deal by deal basis. Family Office and SBIC InvestmentFunds rank in the top 3 sources of equity financing for Independent Sponsor deals.

At one point in time, Jack Bogle, founder of, of Vanguard was chairman of their mutual funds. He is uniquely situated because he has run both public mutual funds as well as privates, including late stage venture private equity credit down the list. Everybody knows what a hedge fund is, but let’s talk about liquid alts.

Eva Shang co- founded Legalist while she was in Harvard and then subsequently dropped out with her co-founder to launch what essentially became an alternative credit fund that specialized in litigation financing along with two other types of credit related to litigation outcomes. What a fascinating conversation. What were you thinking?

So that was a while back, but nonetheless, I don’t know if it was love at first sight, but we got to get along pretty well, and after a few years working for investmentbanks, he then joined Goldman Sachs. I joined, effectively, Deutsche Bank. We decided to try to have a go on our own. We were 28, 30 respectively.

I found this to be just a masterclass in everything you need to know about distressed credit investing, private credit, the role of the economy, the fed interest rates, inflation, bottoms up, credit picking, and how to manage a firm and a fund in light of just massive dislocations in your space, as well as the overall economy.

And what was fascinating about Drexel and kind of the diaspora, if you will, of that era was that we all basically went out looking to take that experience, particularly in high yield and kind of buyouts and financing, and do it at either banks or other investmentbanks. KENCEL: It’s the investmentbanking affiliate.

UK sponsor-backed financing activity experienced a modest slowdown in Q3 2024, as ongoing M&A sluggishness and seasonal dynamics impacted dealflow, according to the latest data from global investmentbank, Houlihan Lokey.

We will continue to invest in these businesses by hiring and retaining the very best bankers in our industry, improving the processes and systems we use to underwrite and fund loans, and continuing to integrate all of the products and service offerings Walker & Dunlop has built to bring one-stop shopping to our clients across the country.

The great tightening started by the Federal Reserve in March of 2022 has added 525 basis points to the Fed funds rate and dramatically reduced transaction volumes across the commercial real estate industry. Private capital is coming into the CRE market to replace bank capital. We appear to have averted a meltdown of the U.S.

Ralph Berg, chief investment officer at OMERS for nearly two years, brings a fresh perspective to pension fund management with a history and work pedigree different to what you might expect from a Canadian fundinvestment boss. billion) funds approach to investing. billion ($97.2

And as property sales volumes pick up, it will benefit investment sales, debt placement, valuation services, investmentbanking, and our affordable housing business. Finally, Zelman Research and InvestmentBanking revenues were down slightly on the quarter but will grow as the market recovers and transaction volumes accelerate.

Made the decision to leave just to try something new at that point, went to Harvard for my MBA and then had made the ch his choice at that point to switch out of biotech and interviewed with a whole bunch of of firms and ended up getting into the hedge fund world, doing capital raising for two large hedge funds. I use that day to day.

No, we always had, and we do have at Oak HCFT one Fund that everything, and, and we would choose the allocation, 00:06:57 [Speaker Changed] Huh. How much service does Oak provide to the companies you work with besides funding? And you talk about five levers of change that the fund looks at. Put some flesh on those bones.

Companies have been thinking twice about acquisition pipelines Before I became a writer at The Motley Fool, I spent a decade working on M&A deals at investmentbanks and start-ups. Broadly speaking, companies rarely have enough cash on the balance sheet to finance a large-scale acquisition (deals in excess of $10 billion).

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content