This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Unlock the power of leverage in private equity. Discover the advantages of a relationship bank providing leverage on both fund and portfolio level, optimizing your investments for maximum returns. They enhance Internal Rate of Return, provide funding certainty in competitive situations, or cater for additional investments.

Fund investing, like adulting, is boring. That’s the first thing anyone trying to raise a fund needs to understand, as well as anyone thinking about investing in one. The partner at the fund, the VC, gets to do the fun part—the meeting with founders, vetting deals, negotiating, helping, etc. So what’s the point?

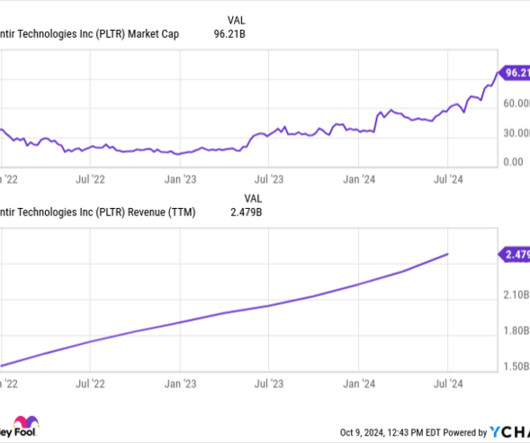

Moreover, I also think that more hedge funds may begin taking positions in Palantir. Such relationships can help strengthen Palantir's dealflow pipeline and provide many cross-selling opportunities, ultimately serving as lucrative catalysts for the company and the stock.

According to data from Pitchbook and Affinity’s annual predictions survey, more than a third of nearly 300 respondents identified due diligence criteria as a major factor impacting dealflow. With a 76% increase in the number of funds in operation from 2015 to 2023, the pressure to identify and close deals has never been higher.

Pantheon, a leading global private markets investor, is pleased to announce the successful closing of Pantheon Global Secondaries Fund VII and associated vehicles (PGSF VII), its latest flagship global private equity secondaries offering, with commitments totalling $3.25bn. Source: Businesswire Can’t stop reading?

Lexington Partners (“ Lexington “), a leading manager of secondary acquisition funds, today announced the completion of fundraising for Lexington Capital Partners X, L.P. (“LCP X”) with $22.7 billion of total capital commitments. per share, private equity firm Sycamore Partners.

Benefit Street Partners (BSP), a credit-focused alternative asset manager with approximately $75bn in AUM and a subsidiary of Franklin Templeton Investments, has closed its fifth flagship direct lending vehicle, BSP Debt Fund V, with $4.7bn of capital.

Not every VC used to get pitched by VC funds for a living and has seen hundreds and hundreds of VC pitch decks. How can we leverage them to help create the next generation of VCs? Aggregating these types of fund investors would make fundraising a lot easier. But what about investors? How are we supposed to get better?

Leveraged loan issuance meanwhile climbed 75% to $41bn in over the period, while high yield bond buyouts stalled in Q2, totalling $4.3bn, less than half of H1 2023’s volume. Direct lenders meanwhile, doubled their activity over the same period, funding $20.6bn in buyout financing in the first half of the year.

IAIM aims to leverage the origination and proprietary dealflow capabilities of Investec’s direct lending team to deliver private market investment solutions for investors. Investors can access this through IAIM via funds, mandates, and co-investment opportunities. Forry has been with Investec for almost seven years.

Oak Hill Advisors (“OHA”) served as a Lead Arranger for the unitranche financing to fund Bain Capital Private Equity’s (“Bain Capital”) acquisition of Harrington Industrial Plastics (“Harrington”) from Nautic Partners. OHA is the private markets platform of T. Rowe Price Group, Inc.

If we ever do get to the one-person unicorn, that’s going to be a lot of people trying to beat out Sequoia and Benchmark to fund its solitary round—a $2mm seed that it never looks back from for additional capital. When Roger Ehrenberg set out to professionalize his angel investing into a fund, he used “Data” as the theme.

Will Turner, Director – Fund Services, chats to Private Equity Wire about industry trends and some of the current challenges and opportunities facing the firm and its clients… PEW: Can you outline the industry trends which have been driving growth and development within your firm over the past year?

One item of note is that while technology was ranked only the fourth highest industry as it relates to total dealflow in Axial in 2023, deals in the tech sector had the leading pursuit rate at 8.92%.

Laura Benitez and Nishant Kumar of Bloomberg report hedge funds draw pension money to riskiest corner of a $1.3 Laura Benitez and Nishant Kumar of Bloomberg report hedge funds draw pension money to riskiest corner of a $1.3 billion in assets, said the attraction of low default rates for leveraged loans, estimated at 1.5%-2%

Following my comments, David and Jesse will provide additional comments regarding our investment strategy, investment portfolio, financial results, capital structure and leverage, and our expectations for the third quarter, after which we'll be happy to take your questions. We are very pleased with our performance in the second quarter.

Following my comments, David and Jesse will provide additional comments regarding our investment strategy, investment portfolio, financial results, capital structure and leverage, and our expectations for the first quarter of 2024, after which we'll be happy to take your questions.

When it comes to the middle market, the deals usually fall in the $50 million to $500 million rangelarge enough to garner serious investor attention, yet small enough to often fly under the radar of the mega-funds. In the middle market, where every deal counts, you need to be both methodical and a bit opportunistic.

Lower incentive compensation and distribution and servicing costs were partially offset by higher direct fund expense. Direct fund expense increased 13% year over year and 9% sequentially as a result of higher rebates in the prior-year quarter and higher average index AUM. government money market funds.

We believe the continued path of central bank normalization will support sustained inflows across bond funds, ETFs, and institutional accounts. Sales, asset, and account expense increased 6% compared to a year ago, driven by higher direct fund expense. This approach is yielding profitable growth and operating leverage.

In addition, we discuss non-GAAP financial measures, including core funds from operations or core FFO, adjusted funds from operations or AFFO, and net debt to recurring EBITDA. Our conversion rate of deals approved by our investment committee to letters of intent signed is the highest in over two years at approximately 38%.

Importantly and atypically, over half of our Q1 debt brokerage dealflow was on non-multifamily assets in retail, hospitality, industrial, and office. While some deals will need to be adjusted or even reworked, many deals remain on track. They have done this in the past and are doing this today.

We also continue to drive share gains in our markets by leveraging a multi-brand, multichannel approach at scale to differentiate ourselves competitively. Additionally, we are leveraging the scale of our Orkin brand across North America to effectively serve commercial customers coast to coast in both the U.S. and Canada.

Paula Sambo of Bloomberg reports Canada pension fund's credit head wants to take advantage of leveraged buyout boom: Canada’s largest pension fund plans to nearly double the size of its credit holdings over the next five years, and it’s counting on an upturn in leveraged buyouts to generate some of that growth.

See the 10 stocks *Stock Advisor returns as of April 15, 2024 Also, note that nothing on this call constitutes an offer to sell or a solicitation of an offer to purchase an interest in any Blackstone fund. And our growth equity fund invested in 7 Brew, an innovative quick service coffee franchisor. billion or $0.98

Their network, dealflow and ability to evaluate companies is limited by the number of hours they have after all their other professional obligations are met. I invest with the speed of an angel but with the capacity of a fund. When these angels make investments, it's often a one-time binary decision. No committees.

Also, please note that nothing on this call constitutes an offer to sell or a solicitation of an offer to purchase an interest in any Blackstone fund. In terms of future harvesting, the third quarter marked the highest amount of overall fund depreciation in three years. Our $30 billion global flagship fund is now nearly 40% committed.

Click here to read the recap 📝 Since the fund started in January 2021 we have deployed $8.1m In addition to the fund which is my primary vehicle, Super Angel Syndicate provides an opportunity for investors to contribute more, from time to time, into individual companies via special purpose vehicles (SPVs).

Unlike other Maple Eight investors, AIMCo’s client funds decide their own asset allocation and most of them have reached their target in private markets. The board has oversight of the risk parameters of every underlying product, and review and set the appetite for risk tolerance and the total fund risk budget. AI is just one example.

In addition, we discuss non-GAAP financial measures, including core funds from operations or core FFO, adjusted funds from operations or AFFO, and net debt to recurring EBITDA. At quarter end, leverage stood at just 3.6 This provides us with $925 million of hedged capital to fund investment activity into 2025.

Click here to read the recap 📝 Since the fund started in January 2021 we have deployed $8.6m In addition to the fund, Super Angel Syndicate provides an opportunity to contribute more, from time to time, into individual companies via special purpose vehicles (SPVs). across 159 investments into 107 companies. gross multiple.

We're also joined this quarter by senior members of our team, including Alexis Maged, our chief credit officer; and Logan Nicholson, who joined the firm in September and served as a portfolio manager for several of our diversified direct lending funds, including OBDC. billion, and we ended the quarter with net leverage of 1.13

Financing led by RA Capital Management with participation from Insight Partners, NVentures, Catalio Capital Management, Eli Lilly and Company, Gaingels, and Cooley LLP Funds to support clinical development of lead programs and expansion of small molecule pipeline focused on high-value GPCR targets BOSTON, Sept.

2020: Black Swan Moment Coronavirus, the black swan of 2020, had a significant impact on the private equity industry, causing uncertainty and volatility in financial markets, disrupting deal-making, and affecting portfolio companies across various sectors.

Inbound Platforms Inbound platforms specialize in helping firms source deals from a variety of sources, including venture capital firms, angel investors, and other private equity funds. Deal volume: The PE deal origination platform should offer a sufficient volume of deals to allow firms to find suitable investment opportunities.

Features like private equity dealflow, valuation capabilities, and analysis tools are key for identifying and landing lucrative opportunities. Despite rising interest rates and market volatility, private equity firms must work hard to deploy these funds and create value in times of uncertainty.

Turning to the broad trends we saw this quarter, as I met with customers around the globe, I saw a strong desire to leverage AI to improve business processes and elevate customer experiences. To add more context around overall dealflow, EMEA grew the fastest during the quarter, followed by the Americas and APJ.

A new survey of investors and deal advisers conducted by Private Equity Wire found high asset prices were the number one challenge when considering tech firms. In March, Permira made a final close of its latest flagship buyout fund, Permira VIII with total capital commitments of €16.7bn.

Read the Q1 2023 Recap here 📝 Since the fund started in January 2021, we have deployed $6.9 On March 14th, AngelList’s CEO also sent a formal update to managers regarding their new banking process for funds, GPs and LPs, which they are calling Networked Banking. million across 119 investments into 91 companies.

Technology ranked 4th in dealflow but had the highest average pursuit rate, 8.76%, of all sectors. See below for the full Q3 deal activity overview on the Axial platform, and for a more detailed breakdown by industry, check out The SMB M&A Pipeline: Q3 2023. .” Tortora hold securities licenses Series 79 and 63.”

We believe that in time, every organization, big and small, will leverage the power of AI to transform their businesses. To add more context around dealflow during the quarter, we saw a healthy balance across our solutions and continue to maintain a similar solution mix in annual contract values versus the prior quarter.

That said, on the positive side, if you look across the US high yield and leveraged loan issuer market, we have had eight consecutive quarters of positive, albeit decelerating, revenue and earnings growth. I’d say on balance, the leveraged space and the economy generally have been trending better than one might have expected.

Buck Hartzell: As an asset manager, you guys are out there launching different products or different funds, you're raising capital around there. The returns that we're focused on are all coming from operational excellence as opposed to excess leverage. But as you mentioned, you're a participant in that. Buck Hartzell: That's awesome.

However, despite increasing numbers of independent sponsors, family offices, search funds, and other less conventional buyers, private equity funds remain the most prominent type of financial buyer in the market. billion of committed capital across four funds. .” billion of committed capital across four funds.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content