This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The cruise line operator's revenue plunged in 2020 and 2021 as global travel ground to a halt during the pandemic, and it was forced to take on a lot more debt to stay solvent. On an adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) basis, it generated a profit of $3.3 NYSE: CCL).

billion in growth capex a year would allow it to pay its distribution while having money left over from its cash flow to pay down debt and/or buy back stock. million in EBITDA (earningsbeforeinterest, taxes, depreciation, and amortization) a year. billion in debt, $3.9 billion in minority interest.

Driven Brands has an enterprisevalue of $5 billion (for the record, this is technically a mid-cap stock, not a small-cap stock). And in 2024, management expects adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) of at least $535 million. Driven Brands has $2.9

billion in net debt, not including operating leases, an ill-advised investment was not a good use of cash. Healthcare segment was able to flip to positive adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) of $17 million and a modest adjusted operating loss of $34 million.

Over the past two years, its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) margins shrank and it racked up steep losses. billion in long-term debt and a staggering debt-to-equity ratio of 70. With an enterprisevalue of $23.4 It's also still saddled with $18.4

Even more disappointingly, the business has been at the forefront of management's corporate actions in recent years, with management buying M*Modal's health information services business for an enterprisevalue of $1 billion in 2018. billion in net debt. It then bought wound care business Acelity for a consideration of $6.7

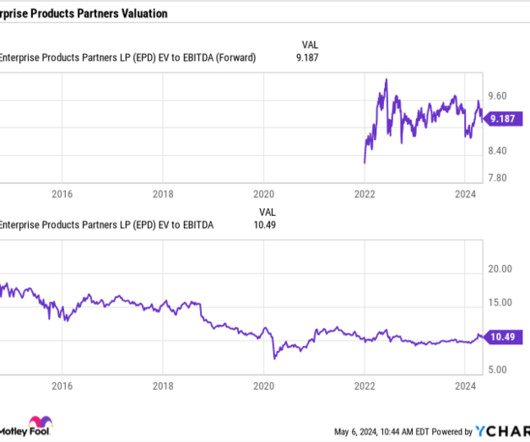

Solid Q1 results Enterprise once again turned in solid results when it reported its first-quarter results, as its total gross operating profit rose 7% to $2.5 Its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, rose 6% to nearly $2.5

That momentum continued in 2022, but the pressure of renovating and reselling those homes boosted its operating expenses, squeezed its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) margins, and caused its net losses to widen. With an enterprisevalue of $3.05 billion $15.6

The company now holds a significant amount of debt. Management plans to divest non-core assets to accelerate the paydown of that debt. Shares currently trade for an enterprisevalue/earningsbeforeinterest, taxes, depreciation, and amortization (EV/ EBITDA ) multiple of just 5x.

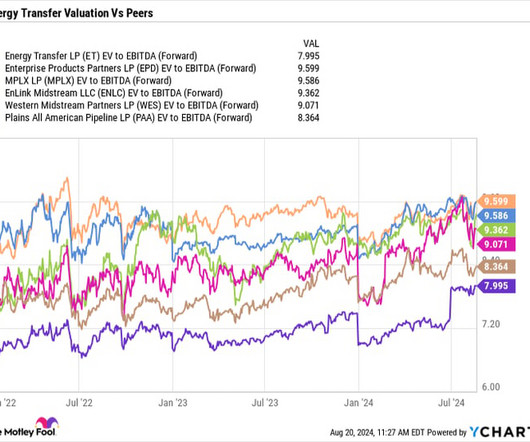

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 < Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earningsbeforeinterest, taxes, depreciation, and amortization) valuation of 9.6

Those growth rates are impressive, but the company's adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) missed its original expectations by a mile. With an enterprisevalue of $3.7 billion, Rocket Lab's stock still looks reasonably valued at 6 times next year's sales.

That said, it’s spent heavily to establish that position, taking on huge amounts of debt, and putting pressure on its balance sheet. To that end, management plans to sell off non-core assets to pay down debt, a playbook it's run throughout its recent history. That also makes Occidental a bit riskier than other oil and gas companies.

Coinbase's adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) margin also turned positive again in 2023 as it aggressively cut costs. billion -- which is more than half of its enterprisevalue of $25.3 Analysts expect its revenue to rise 80% for the full year.

In the second quarter, adjusted earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA) increased by 2.6%, while free cash flow of $4.6 Long plagued by a heavy burden of liabilities, AT&T is managing to deleverage with a decline in net debt supported by positive free cash flow. billion was up $0.4

Approximately 90% of Energy Transfer's 2024 earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) is projected to come from fee-based activities. This is important for investors because it allows the company to pay out its distribution while still being able to pay down debt.

It blamed that slowdown on the macro headwinds, which drove many of its enterprise customers to rein in their spending. However, its high debt-to-equity ratio of 3.1 At its current enterprisevalue (EV) of $496 million, it trades at 11 times that forecast. Can SoundHound maintain its momentum? million this year.

But in 2023, the company's revenue plunged, its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) margin declined, and it stayed unprofitable. Most of that pressure can be attributed to soaring interest rates and a cooling housing market. And with an enterprisevalue of $3.27

Management expects to generate about $80 billion in additional capacity for investments and shareholder returns through 2027 by maintaining its current leverage ratio and growing its earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA). They're still working to pay down debt, which eats up a lot of cash flow.

EBITDA = earningsbeforeinterest, taxes, depreciation, and amortization. Enbridge also plans to refinance about $7 billion of debt next year, which will result in higher interest expenses for the business. Still, the company's inflation-protected assets should position it well to absorb the higher interest cost.

It also declared its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) would turn positive by 2027. billion in cash, cash equivalents, and marketable securities, while its low debt-to-equity ratio of 0.1 Based on its current enterprisevalue of $2.54 billion in 2028.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earningsbeforeinterest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower.

But based on those expectations and its enterprisevalue of $2.2 It's also unprofitable on a generally accepted accounting principles ( GAAP ) basis, and it doesn't even expect its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) to turn positive until 2025. million in 2024.

The stock currently trades at an enterprisevalue of 12.2 times its earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) and yields about 5.3%. As a REIT, it can benefit from falling interest rates. But MAA isn't waiting for rates to fall to invest in the future.

Its growth accelerated in 2021 as the housing market recovered but slowed again in 2022 and 2023 as inflation and rising interest rates drove away potential buyers and sellers. But its high debt-to-equity ratio of 2.9, With an enterprisevalue of $3.5 Metric 2020 2021 2022 9M 2023 Revenue $2.6 billion $8.0 billion $15.6

Its balance sheet isn't pretty ChargePoint insists it can turn profitable on an adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) basis by the fourth quarter of calendar 2024 (which lines up with the third and fourth quarters of fiscal 2024). However, its high debt-to-equity ratio of 2.9

WM Return on Invested Capital data by YCharts Measuring the company's profitability to its debt and equity, Waste Management's 10.5% gap between ROIC and WACC demonstrates Waste Management's ability to create value for shareholders by picking up smaller peers and successfully integrating their operations into the company.

That said, alongside Apple and Rockwell, it's hard to argue that Honeywell is an outstanding value stock. Enterprisevalue (EV, market cap plus net debt) to earningsbeforeinterest, taxation, depreciation, and amortization ( EBITDA ) is a common valuation. Data source: Honeywell presentations.

The analyst retained a buy rating on the stock and raised the price target to $425 from $400 following the announcement to buy SRS Distribution for an enterprisevalue, or EV, (market cap plus net debt) of $18.25 Cyclical companies typically trade on high earnings multiples when they are in a trough in their end markets.

The company claimed it could deliver a compound annual growth rate (CAGR) of 40%, taking revenue from $140 million in 2020 to $388 million in 2023 while expanding its gross margin from 30% to 50% and keeping its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) margins in the high teens.

Unfortunately, the price of oil has dropped considerably during the past six months, putting Occidental in a precarious position considering the amount of debt it took on to make the CrownRock acquisition. He has said that he has no interest in taking a controlling stake of the company.

billion revenue company with earningsbeforeinterest, taxation, depreciation, and amortization ( EBITDA ) of $2.9 billion revenue company with earningsbeforeinterest, taxation, depreciation, and amortization ( EBITDA ) of $2.9 As such, management believes it will create a $12.6

The company typically looks for at least a 12% return on its spending, which would help boost earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA) by more than $370 million per year once all the projects are fully ramped up. It plans to spend around $3.1 billion on growth projects this year.

It has a heavy debt load To save itself during the pandemic lockdowns, Royal Caribbean was forced to take on massive amounts of debt. The company has been able to pay down some of this debt in recent quarters, but total loans outstanding stood at over $20 billion at quarter's end, around double its debt load from before the pandemic.

It also turned unprofitable in both years and took on more debt to stay solvent. That rising leverage made Carnival a risky stock to hold as interest rates rose, and its stock sank to a 30-year low of $6.38 With an enterprisevalue of $46.6 Carnival's debt load is worrisome, but it already prepaid $6.6

Moreover, history suggests that the interest rate cycle will turn, and so will the demand for housing. That will help management achieve its aim of growing earningsbeforeinterest and taxation (EBIT) margin to 9% in 2026 from 6.8% Including those synergies means Owens Corning is buying Masonite at a value of 6.8

An attractive valuation Given the non-cash depreciation costs associated with long-term assets like pipelines and the debt companies carry, midstream companies are generally valued based on an enterprisevalue (EV) to earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) ratio.

billion, which equals roughly a quarter of MicroStrategy's enterprisevalue of $30 billion. On the bright side, they project its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) -- which excludes a lot of that noise -- to increase at a CAGR of 19% from 2023 to 2026.

When interest rates were near zero, many fast-growing companies operated at losses to scale up quickly. And they paid for this growth with debt, promising to become profitable someday when necessary. Well, interest rates shot higher, and it indeed became necessary. For perspective, its enterprisevalue is just $6.2

Despite this track record of success -- along with earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) and FCF growth of 81% and 73% over the last five years -- the share price for MTY stock trading over the counter in the U.S. is down 40% from its high.

Probably the bigger concern with these companies is just their debt loads. But you look at the debt loads on these companies. T-Mobile, long-term debt, $73 billion, Verizon long-term debt, $127 billion, AT&T's $137 billion. Sometimes when those debt loads get out of control, those dividends get cut.

It also narrowed its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) loss from $278 million to $269 million. billion in outstanding debt. That debt inflates Beyond Meat's enterprisevalue to $1.56 million in cash and equivalents and $1.1 times this year's sales.

Operating income rose to $560 million from $120 million a year ago, while adjusted EBITDA (earningsbeforeinterest, taxes, depreciation, and amortization) climbed over 75% to $1.2 Adjusted earnings per share (EPS) turned positive, coming in at $0.11. Before you buy stock in Carnival Corp., Image source: Carnival.

enterprisevalue -to- EBITDA ( earningsbeforeinterest, taxes, depreciation, and amortization) ratio, and funded with high-cost debt and equity sales. billion debt load, getting the company on its way toward its deleveraging target of 2.5 At first, the acquisition scared off investors, as the $4.4

It recently announced it was buying PFSweb for $181 million, or an enterprisevalue of $142 million, which includes the company's cash balance of $39 million. However, its PFS Operations' adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) were $23.2 A robot in a GXO warehouse.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content