This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

After staring at the brink of bankruptcy, a debt restructuring deal rescued the stock. The company has now reported an earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) profit and positive net income for each of the first two quarters in 2024. billion at the end of Q2.

The cruise line operator's revenue plunged in 2020 and 2021 as global travel ground to a halt during the pandemic, and it was forced to take on a lot more debt to stay solvent. On an adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) basis, it generated a profit of $3.3 NYSE: CCL).

But it's not bad news for debt providers because they have been rewarded for putting up capital, with their investment backed up by a relatively liquid asset, the airplanes themselves. The table below shows the company's improvements in earnings and cash flow. Using cash flow to pay down debt (adjusted debt fell from $32.9

Yes, the company generated positive adjusted free cash flow and adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ). The company also managed to refinance debt that was set to come due, solidifying its financial situation.

The leading North American pipeline and utility operator generates very durable cash flow and has very visible growth prospects. Enbridge currently gets 98% of its earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA) from stable cost-of-service or contracted assets. billion-$6.6

Add in its financial strength and growth prospects, and the company is an ideal option for those seeking passive income. A strong start to 2024 Enbridge generated $5 billion in adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) during the first quarter and $3.4

Well, Carvana (NYSE: CVNA) has had an interesting last few years. After announcing a trifecta of improving earnings numbers, a debt restructuring, and an at-the-market (ATM) stock offering last week, shares of the online used car marketplace are now up about 780% year to date and were, at one point, up over 1,000%.

KMI Financial Debt to EBITDA (TTM) data by YCharts That said, a part of the problem was Kinder Morgan's more aggressive use of leverage than its peers'. There's been a lingering consequence from Kinder Morgan's decision to cut its dividend for investors as the midstream sector's growth prospects have shifted.

Lumen is a debt-riddled company whose stock became distressed earlier this year. However, an early-year deal to extend its debt maturities, combined with long-term deals for AI (artificial intelligence) networking, caused the stock to skyrocket in early August. billion in debt and pension liabilities. as of 2:23 p.m.

But some top consumer-oriented companies quietly delivered market-beating gains and still have bright prospects. Carnival's financial position improved steadily over the course of 2023, reducing its debt balance by $4.6 As it pays down debt and lowers its interest expense, the bottom line should also improve.

billion in adjusted earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA) and $1.2 However, growth prospects haven't improved as the country returns to normal. Sirius XM is also starting to pay down its long-term debt since that bearish leverage peaked in 2022. The model works.

The company reported a loss on Q2 adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) of $3.7 also has more than $134 million in net debt without a clear path for generating free cash flow anytime soon. Its lofty valuation is justified by the company's stronger growth prospects.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprise value (EV) -to- EBITDA (earningsbeforeinterest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower. and 7.2%, respectively.

Adjusted earningsbeforeinterest and taxes are now expected between $12 billion and $14 billion, a $1 billion bump over the company's previous guidance range; adjusted automotive free cash flow should come in between $7 billion and $9 billion, up $1.5 Adjusted automotive free cash flow came in at $5.5 billion; average U.S.

It has continued to reduce its leverage and now plans to finish the year with a net debt-to-adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) ratio of just 3.9. Full-year guidance calls for a 15% increase in earnings per share to $1.22 in dividends per share.

Shares trade for a forward price-to-earnings (P/E) ratio of 21.7, But Buffett would describe the prospects for Coca-Cola as “better than the average American corporation.” That said, it’s spent heavily to establish that position, taking on huge amounts of debt, and putting pressure on its balance sheet.

In fact, management thinks that Carnival will produce adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) of $4 billion (at the midpoint) this fiscal year. The company also has $33 billion of long-term debt on its balance sheet. Adjusted earnings per share of $0.63 Revenue of $41.5

Most importantly, you would expect it to have phenomenal prospects in a growing industry. If you have $500 after paying down debt and saving for an emergency fund, consider buying shares. What makes something the ultimate growth stock? I would say it needs to have a few features.

The best way to ensure you're always a step ahead of Wall Street is to hold shares of quality companies with great prospects for long-term growth. The stock returned 450%, beating the major indexes, as the company grew revenue and earnings at double-digit percentages on an annualized basis.

The company claimed it could deliver a compound annual growth rate (CAGR) of 40%, taking revenue from $140 million in 2020 to $388 million in 2023 while expanding its gross margin from 30% to 50% and keeping its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) margins in the high teens.

When a company that most have discarded or ignored changes its fortunes for the better, the prospect of outsize stock returns is large. Finally, Lumen recently reached a deal with creditors that hold $7 billion of the company's debt. In 2027, Lumen had a large maturity "tower" in which a lot of its debt would come due.

Approximately 90% of Energy Transfer's 2024 earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) is projected to come from fee-based activities. This is important for investors because it allows the company to pay out its distribution while still being able to pay down debt.

Chart Industries' improving prospects It's a positive step for a stock that's endured its fair share of volatility over the year. Taking on a significant amount of debt in a rising rate environment, when the economy is passing through an uncertain period, is questionable, and investors reacted negatively to the deal at the time.

The company typically looks for at least a 12% return on its spending, which would help boost earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA) by more than $370 million per year once all the projects are fully ramped up. It plans to spend around $3.1 billion on growth projects this year.

As tantalizing as these growth prospects are, Dutch Bros' nearly positive free cash flow (FCF) is what makes the company so interesting to me right now. Trading at 21 times forward earnings , Chewy's budding profitability, devout customer base, and veterinary growth potential look reasonably priced for prospective investors.

Despite the Q1 profit miss, management still reiterated its full-year adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) guidance of $500 million to $550 million. billion but net debt around $1.6 That confidence was spurred by the signing of new contracts for its rigs. That amounts to a 6.2%

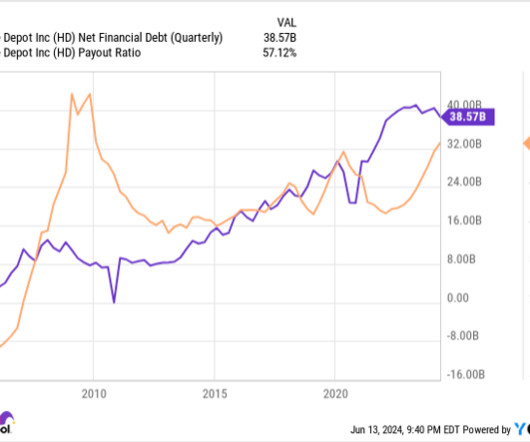

billion in adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) annually. As for when the housing cycle might reverse, the Federal Reserve recently signaled it could cut interest rates at least once in the second half of 2024. Currently, Home Depot pays a quarterly dividend of $2.25

Probably the bigger concern with these companies is just their debt loads. But you look at the debt loads on these companies. T-Mobile, long-term debt, $73 billion, Verizon long-term debt, $127 billion, AT&T's $137 billion. Sometimes when those debt loads get out of control, those dividends get cut.

Given that Bretthauer's prior estimate called for the pharmacy chain's shares to trade around $27, her update signifies increasing bearishness about its prospects for growth and profitability. At the same time, its debt load of $34.7 And there's more than one culprit for darkening sentiment. Will things start to look up?

Adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) surged 39% to $180 million. billion in cash and cash equivalents, short-term investments, and zero debt. In short, The Trade Desk's growth prospects will remain bright in the coming years. It also ended the quarter with $1.4

However, management has successfully reduced net debt to $2.8 EPR net debt (quarterly), data by YCharts; TTM = trailing 12 months. Prospects look promising for LTC Properties because America's aging population should keep demand for its services high. O net financial debt (quarterly); data by YCharts.

The company also specializes in venture debt for start-ups in the technology, life sciences, and sustainable energy industries. Revenue, EBITDA (earningsbeforeinterest, taxes, depreciation and amortization), and free cash flow saw some dips that resulted in a modest sell-off of the stock. Horizon Technology: 11.1%

Adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, soared 80% to $601 million. billion in net debt. The latter metric takes into account its net debt and removes noncash items. Gross margins for the quarter came in at 73.8%, a huge jump from 65.5% a year ago.

billion, while adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) advanced by $52 million to reach more than $162 million. Free cash flow and no debt Chewy also boasts strong free cash flow -- more than $52 million in the quarter -- and has more than $1.1 billion in cash and no debt.

It still faces headwinds, including price inflation and the prospect of an economic recession in Europe, which the company says it can tackle. The company had net debt of 550 million euros ($600 million) as of the end of March. Silver Lake declined to comment, while Global Blue did not immediately respond to a request for comment.

GXO Logistics (NYSE: GXO) was spun off from XPO (NYSE: XPO) in 2021 with a lot of promise and bright prospects. Separating from XPO, the argument went, would allow the company to focus on acquisitions that best serve its own goals and use debt and equity compensation to advance the business.

Does it make sense to take on debt to buy a company in a declining market? billion acquisition, at a 38% premium to the share price before the announcement, with Owens Corning taking on $3 billion in debt financing. The deal values Masonite at an enterprise value (market cap plus net debt) of 8.6

Analysts earlier this year estimated a sale of WGSN could fetch more than 800 million pounds including debt or 16-18 times its expected 2023 earningsbeforeinterest, tax, depreciation and amortisation (EBITDA). A bid by Apax would see the private equity firm return to the company.

The debt burden has always been an issue, so much so that the stock's alarming drop from August 2021 to December 2022 was influenced by the fear that Carvana was about to enter bankruptcy. To help alleviate the situation, management entered into a deal with creditors last year that lowered interest payments and extended maturities.

declining revenue/profits or high debt loads). It is predicted that Centene's net debt position will come in around $3.4 billion in earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) that is expected for the year, this equates to a net-debt-to-EBITDA ratio of just 0.6.

Supporting this argument, it is projected that the retailer's net debt will come in at around $397 million in its fiscal year 2023. Measured up to the $578 million in earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ), this works out to a debt-to-EBITDA ratio of 0.7-- less than its average of 0.8

Management's primary goal at the moment is to break even on its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) before the close of 2026. Furthermore, while it currently has no long-term debt, it does have $452.2 million in capital lease obligations.

It also reported a record adjusted earningsbeforeinterests, taxes, depreciation, and amortization ( EBITDA ) of CA$3.4 In September, the pot grower announced it had repurchased $9 million in convertible debt the month before. Aurora Cannabis's prospects would remain uncertain. Its revenue of 63.4

Let's take a closer look at the midstream company's Q2 results, distribution, long-term prospects, and whether now is a good time to buy the stock. Its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, climbed 10% to nearly $2.4 It generated distributable cash flow of $1.8

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content