This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Let's start with leverage. Cruise lines took on a lot of additional debt during the pandemic-related shutdown in 2020 that lasted well into 2021. Leverage isn't typically a positive thing, but let's play this out. Its debt-saddled enterprisevalue is almost $50 billion. Carnival's market cap is $20 billion.

Carnival (NYSE: CCL) is one of the companies that's still being affected by the pandemic, both by the aftereffects of restrictions and by the financial leverage it took to get through the pandemic. The biggest change has been a huge increase in debt, which currently stands at $31.3 billion last quarter.

Private equity firms Apollo Global Management and BC Partners have joined forces to agree a deal to acquire GFL Environmentals Environmental Services business at an enterprisevalue of CAD8bn ($5.59bn). The remaining funds, up to CAD2.25bn, are earmarked for opportunistic share repurchases, enhancing shareholder value.

The cruise line operator's revenue plunged in 2020 and 2021 as global travel ground to a halt during the pandemic, and it was forced to take on a lot more debt to stay solvent. billion in long-term debt, but that figure hit a whopping $29.5 billion in long-term debt, but that figure hit a whopping $29.5 NYSE: CCL).

However, Chevron is by far the largest, with a nearly $320 billion enterprisevalue compared to Occidental's at over $80 billion. billion of debt. That put its leverage ratio at 12%, or 8.8% billion of debt and about $1.2 That exceeded the company's long-term target to get debt below $15 billion.

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 times (one of the most common ways to value midstream stocks) is attractive and well below the 13.7 The stock sports an attractive 8% yield based on its most recent distribution and had a robust 1.6

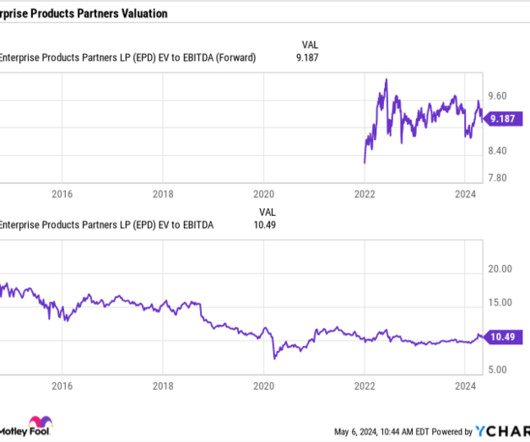

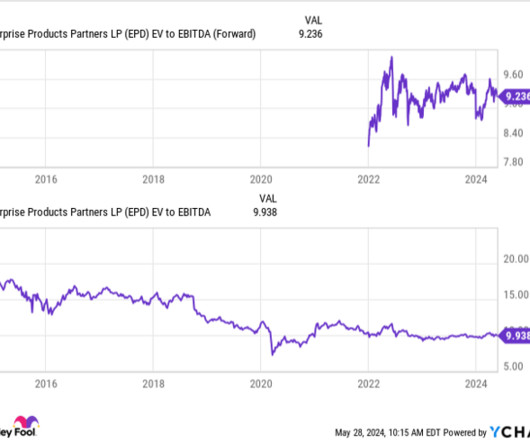

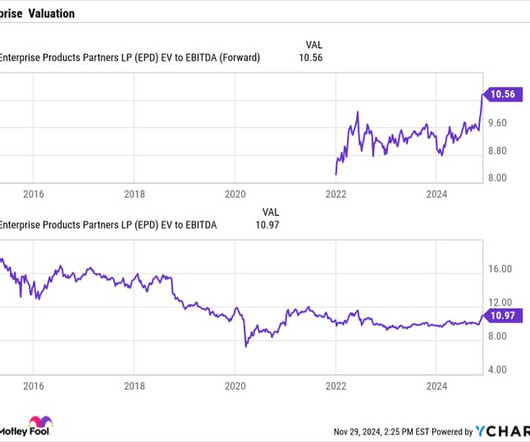

Enterprise ended the quarter with leverage of 3x. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. What this means for investors in simpler terms is that Enterprise's distribution payout is well covered by its cash flow.

During 2023, Medical Properties has found itself in need of de-leveraging and has sold off some properties to do so. Earlier this year, Medical Properties even cut its dividend almost in half in September in order to help it pay off debt and increase flexibility.

It's trading for 26 times trailing earnings, and given its debt-bloated balance sheet, that multiple jumps to nearly 60 if you swap out market cap for enterprisevalue as the numerator. Carnival and its peers had to load up on debt at high rates or sell new shares at low prices to stay afloat. cruise was able to set sail.

Microstrategy (NASDAQ: MSTR) continues its incredible run as the company sells more debt and equity to buy more Bitcoin (CRYPTO: BTC). As Microstrategy becomes a pure Bitcoin play, if the enterprisevalue of the company exceeds the value of the Bitcoin on the balance sheet, it will issue shares to buy Bitcoin.

This is important for investors because it allows the company to pay out its distribution while still being able to pay down debt. When Energy Transfer cut its distribution in 2020, it was because its leverage became too high, and it needed to pay down debt. cents is now higher than the 30.5

The company now holds a significant amount of debt. Management plans to divest non-core assets to accelerate the paydown of that debt. Shares currently trade for an enterprisevalue/earnings before interest, taxes, depreciation, and amortization (EV/ EBITDA ) multiple of just 5x. By comparison, Chevron trades for a 6.6x

That marked the first time its total cash and BTC holdings exceeded its total debt. Marathon's revenues are soaring, but it isn't consistently profitable on a generally accepted accounting principles ( GAAP ) basis, and it's taking on a lot of debt to expand its mining operations. With an enterprisevalue of $6.1

However, its high debt-to-equity ratio of 2.9 That stock offering won't increase its leverage, but it will cause significant dilution for a company with an enterprisevalue of only $1.4 It secured a new $150 million revolving credit facility back in late July to broaden its safety net.

At the same time, Energy Transfer continues to trade at a forward enterprise-value -to- EBITDA multiple of 8 times based on 2025 estimates, which is well below historical levels, not to mention one of the lowest valuations in the MLP space. Its second-quarter results reported a distribution coverage ratio of over 1.8

Management expects to generate about $80 billion in additional capacity for investments and shareholder returns through 2027 by maintaining its current leverage ratio and growing its earnings before interest, taxes, depreciation, and amortization (EBITDA). They're still working to pay down debt, which eats up a lot of cash flow.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower.

Lastly, it continued to rack up steep losses while increasing its leverage with more convertible debt offerings. With an enterprisevalue of $17.5 Second, it issued several safety-related recalls. All of those weaknesses made it an easy target for the bears in a high interest rate environment.

The analyst retained a buy rating on the stock and raised the price target to $425 from $400 following the announcement to buy SRS Distribution for an enterprisevalue, or EV, (market cap plus net debt) of $18.25 times EBITDAR and adjusted debt to $55 billion to $69 billion; this looks manageable. It generated $1.1

With an enterprisevalue of $50 billion, Atlassian doesn't seem cheap at 13 times this year's sales. Investors should also recall that Atlassian is still unprofitable on the basis of generally accepted accounting principles ( GAAP ) and has an alarmingly high debt-to-equity ratio of 5.3.

The company will remain unprofitable on a generally accepted accounting principles ( GAAP ) basis, but it's still shouldering $194 million in long-term debt while holding just $33 million in cash and equivalents on its balance sheet at the end of 2023. Analysts expect revenue to rise 31% in 2024 only for it slow to 13% in 2025. stock headed?

It took some of that cash and bought back about $150 million in debt. Without reducing debt any further, the company is on track to get to 3 times leverage (net debt/adjusted EBITDA) by year end. Image source: Getty Images. This is something I firmly believe.

It also turned unprofitable in both years and took on more debt to stay solvent. That rising leverage made Carnival a risky stock to hold as interest rates rose, and its stock sank to a 30-year low of $6.38 With an enterprisevalue of $46.6 Carnival's debt load is worrisome, but it already prepaid $6.6

I consider Enterprise's distribution extremely safe. The two biggest areas to look at when it comes to dividend safety are its distribution coverage ratio and leverage ratio. On that front, Enterprise had a robust 1.7x When the leverage at companies gets too high, there's a risk they may cut their dividend.

And they paid for this growth with debt, promising to become profitable someday when necessary. For perspective, its enterprisevalue is just $6.2 In recent months, management lowered guidance, the company decreased its dividend, Advance was removed from the S&P 500 , and S&P Global Ratings downgraded its debt.

Unfortunately, the price of oil has dropped considerably during the past six months, putting Occidental in a precarious position considering the amount of debt it took on to make the CrownRock acquisition. Its leveraged exposure to oil production has pushed down Occidental's share price to levels it hasn't seen since the beginning of 2022.

An elevated leverage ratio led the master limited partnership (MLP) to slash its distribution to retain more cash for debt reduction in 2020. However, as leverage improved, the company's priority shifted back to rebuilding its payout. With an enterprisevalue (EV) of $98.5 billion and $13.4 billion for 2023.

The company's balance sheet is currently in good shape, with leverage (as used by rating agencies) toward the low end of its 4x to 4.5x Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple. target range. times distribution coverage ratio in the second quarter.

It recently announced it was buying PFSweb for $181 million, or an enterprisevalue of $142 million, which includes the company's cash balance of $39 million. The company continues to focus on paying down debt to position itself for other acquisitions. Now, GXO has made another promising deal. A robot in a GXO warehouse.

Qualcomm also generates most of its profits from its higher-margin licensing business, which leverages its massive portfolio of wireless patents to squeeze royalties and licensing fees from every smartphone sold worldwide (including those that don't use Qualcomm's SoCs). It has an enterprisevalue of nearly $190 billion with 1.1

The company generates a lot of cash flow, and has historically taken a conservative posture with leverage , which is also why it has been able to consistently increase its distribution. Leverage currently stand at 3, which is low for the midstream industry. Enterprise currently has a robust forward yield of 7.2%

The company generates a lot of cash flow, and has historically taken a conservative posture with leverage , which is also why it has been able to consistently increase its distribution. Leverage currently stand at 3, which is low for the midstream industry. Enterprise currently has a robust forward yield of 7.2%

Centerbridge invests between $50 million and $300 million in US-based leveraged buyouts and distressed securities. Pine Island makes control equity, minority equity, and structured equity investments of $30 million to $250 million in US and Canadian-based companies with enterprisevalues ranging from $50 million to $500 million.

Lincoln International has reported that the Lincoln Private Market Index (LPMI), which tracks the enterprisevalue of U.S. contraction in enterprisevalue due to investor uncertainty surrounding interest rates and potential tariffs. “Rising debt levels and lower buyout multiples may impact private equity returns.”

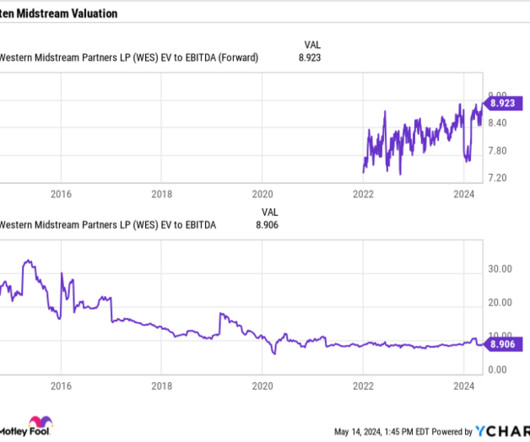

It ended the quarter with leverage of 3 times. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. This leverage is considered low in the midstream space given the strong cash flow these companies generate. It had a distribution-coverage ratio of 1.6

government reached a deal to increase the federal debt limit, many student loan borrowers were caught by surprise. Additionally, Carnival also took on a massive amount of debt to raise even more cash. CCL EnterpriseValue data by YCharts Carnival simply isn't as cheap as it looks. trillion in loans they owe.

billion and boost its debt-to-equity ratio to 1.2. Its enterprisevalue of $2.5 It ended its latest quarter with just $243 million in cash and equivalents, and its high debt-to-equity ratio of 3.3 That lifeline will keep Plug Power's business alive, but it will also roughly double its total liabilities to $3.45

billion in net debt on its balance sheet, generating cash flow and lowering that debt will be important. From a valuation perspective, the company trades at a forward price-to-earnings (P/E) ratio of about 17 and a forward enterprisevalue (EV) -to-EBITDA multiple of about 9. It reported adjusted free cash flow of $1.3

times average enterprisevalue (EV) -to- EBITDA multiple between 2011 and 2016, while today most midstream stocks trade at under a 10 times multiple. EV/EBITDA tends to be the most used metric to value midstream companies, as it takes into consideration their debt positions and takes out non-cash expenses.

Its earnings growth has also helped drive down its leverage ratio , which it expects will be toward the low end of its 4.0-4.5 That lower leverage recently gave two credit rating agencies the confidence to upgrade Energy Transfer's credit rating to BBB with a stable outlook. billion) to pay down debt and repurchase units.

At its peak, Nio's enterprisevalue reached $91.4 But as of this writing, Nio trades at about $6 per share with an enterprisevalue of $12.1 That's a grim outlook for a company that ended its latest quarter with a high debt-to-equity ratio of 5.2. The Chinese electric vehicle (EV) maker went public at $6.28

The macro headwinds also throttled the growth of its enterprise-facing services, while its widening losses and soaring debt forced it to eliminate its dividend last November. Lumen originally planned to leverage the increased scale of its wireline business to generate slow but stable growth. respectively.

That's nearly half of MicroStrategy's current enterprisevalue of $9.7 billion in long-term debt and a debt-to-equity ratio of 3. But its enterprisevalue is getting a bit overheated at 19 times this year's sales. As a result, its Bitcoin holdings swelled from $250 million to $4.7

Enterprise's consistency stems from its largely fee-based model, where the company only takes on minimal commodity or spread risk. Meanwhile, it has historically been conservative with its leverage, distribution coverage ratio, and growth capital expenditure (capex) spending. Currently, the stock carries a forward yield of about 6.2%.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content