This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

billion means it trades at less than eight times its lowest FCF in the last three years, an extremely low valuation for a company that arguably has growth prospects now its freed from a struggling parent company. Management is candid that paying down debt is a strategic priority over the next two years.

Granted, the company slashed its distribution in 2020 because it needed to pay down debt. However, Energy Transfer's debt load isn't as problematic now. Earlier this year, Fitch and S&P (upgraded the company's senior unsecured debt rating. Good growth prospects Energy Transfer has perhaps surprisingly good growth prospects.

Earlier this year, Medical Properties even cut its dividend almost in half in September in order to help it pay off debt and increase flexibility. One such sale was the sale of three hospitals to Prospect Medical Holdings. However, that sale was conditioned on Prospect then selling the hospitals to Yale New Haven Health.

The cruise line operator's revenue plunged in 2020 and 2021 as global travel ground to a halt during the pandemic, and it was forced to take on a lot more debt to stay solvent. billion in long-term debt, but that figure hit a whopping $29.5 billion in long-term debt, but that figure hit a whopping $29.5 NYSE: CCL).

With that said, MicroStrategy is not like any other publicly traded company on the market because, facing limited growth prospects in its software business, it decided to purchase $250 million of Bitcoin in 2020 -- and hasn't stopped buying it since. Still, prospective buyers should know a few things before investing in MicroStrategy today.

billion and a market value of $24.5 MicroStrategy's Bitcoin portfolio is equal to about a third of the company's enterprisevalue of $73.3 If we only look at its software business, MicroStrategy's near-term prospects aren't impressive. It's also taking on a lot more debt and issuing more shares to fund those purchases.

The prospects continue to improv. It's true that Carnival's multiple is substantially higher if we base it on enterprisevalue instead of the garden variety market cap. Carnival and its rivals had to raise a lot of debt when they weren't issuing new shares to literally and figuratively stay afloat in the wake of the pandemic.

With so much cash pouring in, the company's balance sheet is rock-solid: over $58 billion in cash and equivalents with only $38 billion in debt, for a net cash position of about $20 billion. Monday.com has proved itself to be a winner, which should have investors salivating at the company's still-bright long-term prospects.

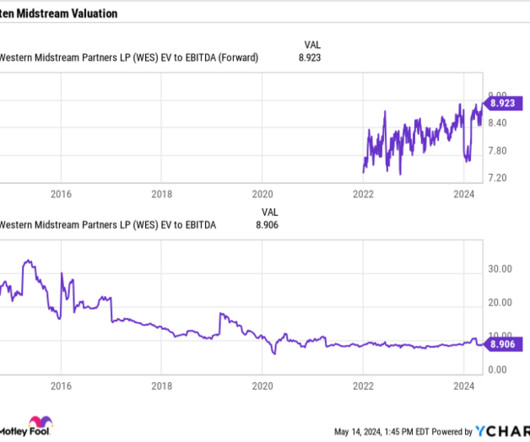

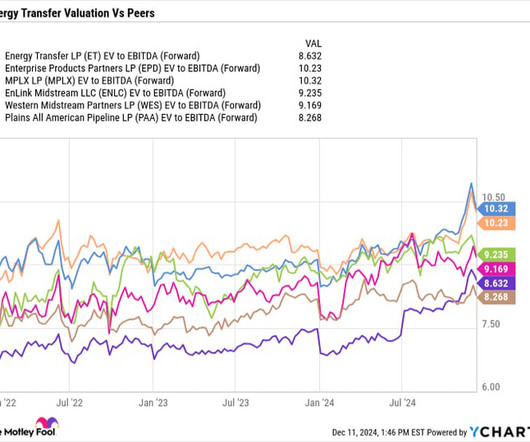

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 It and Enterprise also have the most attractive yields of the group at 8.1% and 7.2%, respectively.

But Buffett would describe the prospects for Coca-Cola as “better than the average American corporation.” That said, it’s spent heavily to establish that position, taking on huge amounts of debt, and putting pressure on its balance sheet. Shares trade for a forward price-to-earnings (P/E) ratio of 21.7,

This is important for investors because it allows the company to pay out its distribution while still being able to pay down debt. When Energy Transfer cut its distribution in 2020, it was because its leverage became too high, and it needed to pay down debt. cents is now higher than the 30.5 cents it was before the distribution cut.

BigBear.ai's prospects sounded promising, but it broadly missed its rosy pre-merger targets. Its low enterprisevalue of $670 million might even make it a compelling takeover target for a larger tech company. That flexible approach helped the company carve out a tiny niche in the crowded analytics market. Where is BigBear.ai

It has worked closely with its two largest tenants (Steward Health Care and Prospect Medical) to assist them during their financial challenges. The REIT helped provide both with loans while deferring some of Prospect's rent. The company has also reduced its exposure to those troubled tenants by selling properties leased to Prospect.

The company currently holds 402,100 Bitcoins, presently valued at $39.1 For investors interested in seeing if MicroStrategy's rise is a fluke or just the beginning, let's explore how and why MicroStrategy is hoarding Bitcoin and its future prospects to see whether MicroStrategy stock is a buy, sell, or hold. year-over-year decline.

Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple. The first is that enterprisevalue takes into consideration the amount of net debt a company carries on its balance sheet. The reason for this is twofold. ET EV to EBITDA (Forward) data by YCharts.

Probably the bigger concern with these companies is just their debt loads. But you look at the debt loads on these companies. T-Mobile, long-term debt, $73 billion, Verizon long-term debt, $127 billion, AT&T's $137 billion. Sometimes when those debt loads get out of control, those dividends get cut.

It took some of that cash and bought back about $150 million in debt. Without reducing debt any further, the company is on track to get to 3 times leverage (net debt/adjusted EBITDA) by year end. Image source: Getty Images. While this valuation gap will not close overnight, it is a long-term opportunity for investors.

The total enterprisevalue of the deal is $7.9bn, which was adjusted for working capital balances at the close and resulted in a final enterprisevalue of $8.2bn. billion in outstanding debt commitments stemming from its 2017 Chapter 11 bankruptcy, which reduced the equity cost of the acquisition.

The deal values Wincanton at 450p a share, a premium of approximately 52 per cent to the pre-deal closing price and an 82 per cent premium to its average share price over the past 12 months. The acquisition implies an enterprisevalue multiple of approximately 6.8 times Wincanton’s underlying Ebitda.

More to the story But while Moderna's near-term prospects don't look as good as many of us expected, there is more to the story. The mRNA innovator's long-term prospects still seem bright. However, Moderna's enterprisevalue (EV) is $10.75 I think that's an attractive valuation, considering Moderna's growth prospects.

Staszak also feels that Carnival's improved liquidity will make it easier to pay down its debt, a big deal since Carnival's long-term debt has more than tripled to nearly $32 billion since the pandemic shut down operations for a long time. Carnival's near-term prospects have never been stronger than they are right now.

That CrownRock deal also left Occidental with a high level of debt on its balance sheet. Management is strategically divesting assets to accelerate its debt paydown. CEO Vicki Hollub expects to reduce the debt on its balance sheet from around $19.7 billion to $15 billion by the end of 2026 or the first quarter of 2027.

billion in net debt. Despite its transformation and solid long-term growth prospects, the company only trades at a forward price-to-earnings (P/E) ratio of under 14 times 2025 analyst estimates and a forward enterprisevalue -to-EBITDA (EV/EBITDA) ratio of under 11. It ended the quarter with just under $3.1

It's not always a pleasure cruise Cruise line operators had to take on gobs of new debt and issue new shares in 2020 and 2021 when they were unable to fully operate their ships. One can argue that the multiples are low because the enterprisevalues are much higher than the debt-saddled market cap. It's a fair knock.

Does it make sense to take on debt to buy a company in a declining market? billion acquisition, at a 38% premium to the share price before the announcement, with Owens Corning taking on $3 billion in debt financing. The deal values Masonite at an enterprisevalue (market cap plus net debt) of 8.6

I decided to dig into the business to uncover why Affirm's long-term prospects aren't just promising -- they signal that investors could have a perennial market-beater on their hands. credit card debt. Credit Card Debt data by YCharts Affirm's total transaction value was just $6.3 Here is what you need to know.

Its debt ballooned after the $2.5 It's easy to see why this was a hot IPO in 2018 given its heady growth prospects at the time. billion in net cash on its debt-free balance sheet. billion in net cash on its debt-free balance sheet. Huya trades at an enterprisevalue of negative $490 million.

Let's take a closer look at the midstream company's Q2 results, distribution, long-term prospects, and whether now is a good time to buy the stock. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. The stock now has a forward yield of about 7.2%

Last quarter, Enterprise had a robust distribution coverage of 1.7 Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ).

Because NextEra either has to raise money from the debt markets or sell some of its stock to fund projects, a downward spiral in its stock price could be self-fulfilling. However, with the Fed easing off the brakes, the prospect of that rate-headwind trend reversing pushed NextEra's stock higher this week. NEP data by YCharts.

It will allow the healthcare REIT to retain additional cash for debt reduction. Because of that, investors will need to be patient as the company works to rebuild shareholder value. The company has repeatedly demonstrated the value of these properties through monetization transactions for values at or above its initial purchase price.

Lockheed Martin's valuation That said, every stock has its value, and a quick look at Lockheed Martin's valuation suggests it's being priced with some pretty positive assumptions in mind. In addition, on a price-to-free cash flow basis, the stock trades at slightly less than 22 times Wall Street estimates for free cash flow (FCF) in 2024.

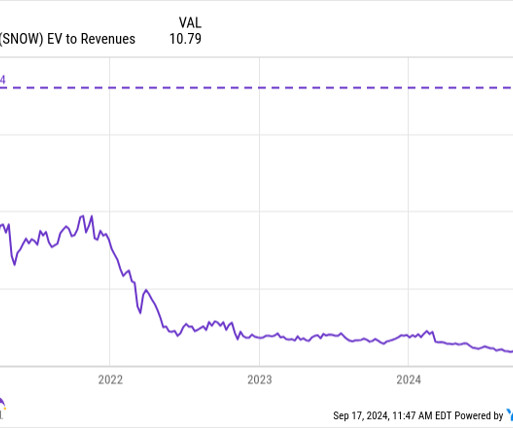

The good news is that Snowflake has now fallen far enough that it could completely change the stock's long-term investment prospects. At its peak, investors paid an enterprisevalue (EV) -to-revenue ratio of nearly 216. billion in cash and zero debt, so the financial risk isn't as bad as it looks at first glance.

The investment case for Siemens rests on the idea that its mobility business (rail rolling stock, rail infrastructure, and services) and Siemens Healthineers are relatively stable businesses with good growth prospects through the economic cycle. WHR Days Inventory Outstanding (Quarterly) data by YCharts.

billion in long-term debt. Instead, it expanded its wireline business, rolled out new fiber plans, and bundled more cloud, security, and collaboration services into its enterprise-oriented plans. However, with an enterprisevalue of $22.8 Its free cash flow turned negative, and it ended its latest quarter with $18.1

It has also received requests from more than 40 prospective data centers in 10 states that could use 10 BCF a day of natural gas. Attractive valuation Besides having some of the best growth opportunities in the pipeline space, Energy Transfer is also one of the most attractively valued MLPs. Image source: Getty Images.

In fact, roughly 30% of the debt of companies in the Russell 2000 small cap index is floating-rate , compared with only 6% in the S&P 500. Second, the prospect of a healthy economy but with lower-interest rates could be in the cards -- a so-called "soft landing." in only one or two end markets.

Investors have gotten more optimistic about the company's prospects as it skirted bankruptcy, refinanced its debt, and inched closer to profitability. billion in long-term debt, giving it a precarious financial position. Add its net debt of approximately $5 billion, and its enterprisevalue ( EV ) is $15 billion.

Interestingly, Dassault trades at a current enterprisevalue (market cap plus net debt), or EV, to earnings before interest, taxation, depreciation, and amortization ( EBITDA ) valuation of nearly 30. That's a reasonable valuation for a company with excellent long-term growth prospects.

Meanwhile, the stock has an enterprisevalue of $5.1 It could be difficult for the stock to continue at its current pace, so prospective shareholders should look for a pullback before buying. billion and zero debt. Unfortunately, that growth is on a small scale; Q3 revenue was only $25.2

There is a cliche that price is what you pay, and value is what you get. All a stock price tells you is what other investors or prospective investors or soon to be former investors are willing to transact at the moment. But then, so whether that's price or whether it's enterprisevalue, we can, there's applications for each.

Funds raised money, bought businesses, loaded them with debt, exited at a profit and convinced happy investors to do it all over again — at ever greater scale. Some top industry figures don’t dispute the perils of gulping down more and more varieties of debt. “On Surging borrowing costs have stalled that engine.

In the broad strokes, the earnings multiple valuation method involves applying an industry-based multiple to the earnings of a business to arrive at an implied enterprisevalue. From this enterprisevalue, subtracting net debt gives the equity value.

Some of the information we provide during today's call regarding our future expectations, plans, and prospects may constitute forward-looking statements. As with prior programs, we may use the proceeds for general corporate purposes, which include the purchase of Bitcoin as well as the repurchase or repayment of our outstanding debt.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content