This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Enterprise ended the quarter with leverage of 3x. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. What this means for investors in simpler terms is that Enterprise's distribution payout is well covered by its cash flow. It currently has $6.9

Best-in-class profitability In addition to this advantage from monetizing the by-product of its core collections business, Waste Management has historically held higher return on invested capital (ROIC) figures than its two most prominent peers. ROIC shows that it is the best in its industry at reinvesting in its business.

Over the last decade, MTY has averaged a return on invested capital (ROIC) of 15%, generating high levels of FCF compared to the debt and equity it uses to fund its M&A ambitions. Compared to its weighted average cost of capital (WACC) of 7%, the company consistently creates value for investors.

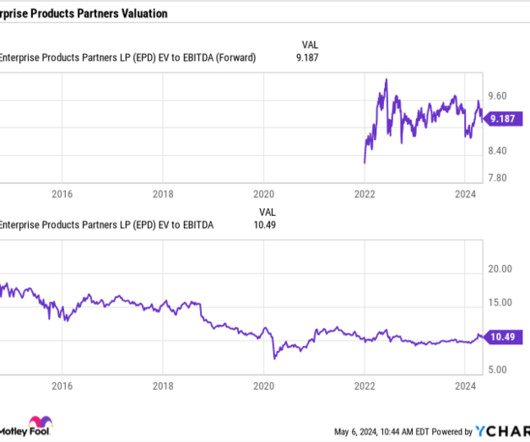

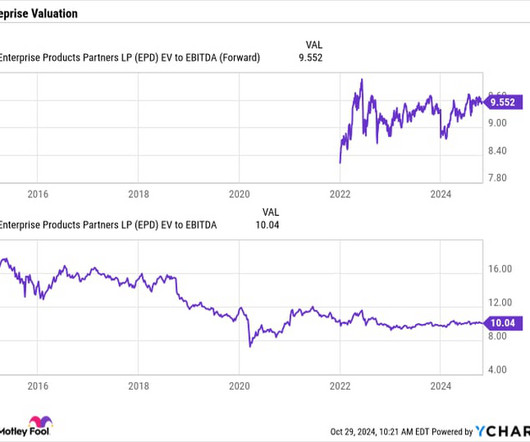

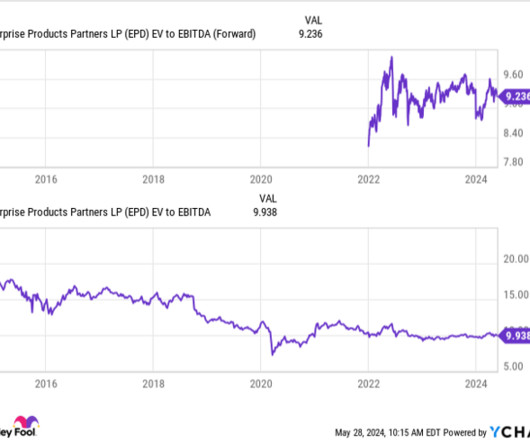

It has averaged a return on invested capital (ROIC) of about 12% over the past decade. Enterprisevalue takes into consideration a stock's net debt, while EBITDA removes non-cash expenses. On that basis, Enterprise is trading at just over a 9x multiple. The company currently plans to spend between $3.25

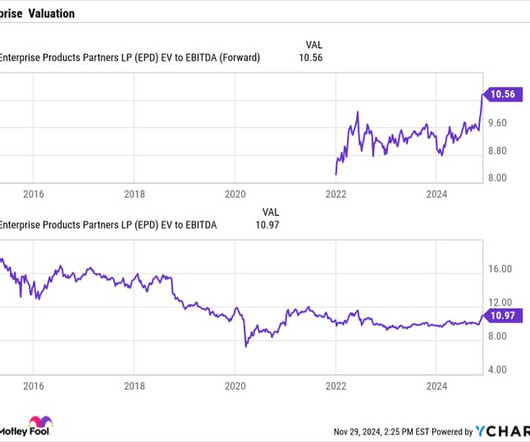

Last quarter, Enterprise Products Partners had a distribution coverage ratio of 1.7. The company's balance sheet also remains in good shape, with net debt (adjusted for equity credit in junior subordinated notes) standing at three times adjusted EBITDA. Its enterprise-value -to-EBITDA (EV/EBITDA) multiple stands at 10.5,

It ended the quarter with leverage of 3x, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. Enterprise currently has $6.9 It noted that it has produced about a 12% return on invested capital over the past decade.

Yet, on the other hand, inflation and higher interest rates are a big counterweight to the bull case, as all major cruise companies are now loaded with debt -- a result of the emergency borrowing during the pandemic -- while also battling higher labor costs. In 2023, investors in the largest cruise company in the world, Carnival Corp.

Over the past five years, Enterprise has averaged about a 13% return on invested capital, so these growth projects should provide meaningful growth to the company in the years ahead. At a similar return, the approximately $10.5 billion in growth capex spent between 2023 to 2025 should lead to about $1.4

The company defines leverage as net debt adjusted for equity credit in junior subordinated notes divided by adjusted EBITDA.) Enterprise currently has a robust forward yield of 7.2% The company typically has gotten a 13% return on invested capital over the past several years. based on its $0.515 quarterly distribution.

The company defines leverage as net debt adjusted for equity credit in junior subordinated notes divided by adjusted EBITDA.) Enterprise currently has a robust forward yield of 7.2% The company typically has gotten a 13% return on invested capital over the past several years. based on its $0.515 quarterly distribution.

Furthermore, its enterprise-value-to-free-cash-flow (EV/FCF) ratio is well below its average over the same time, highlighting the market's uncertainty around the company. Cash ROIC measures a company's FCF generation compared to its debt and equity, meaning that higher figures show outsized returns on capital deployed.

The second thing that this gets rid of is the debt. When we get to this return number, why are we getting debt out of this thing? Asit Sharma: Let's now extend net tangible assets by one letter, unlevered net tangible assets and that is getting rid of the debt. That's your return piece. of long term debt.

compounded annually, which will allow us to use our cash flow generation to pay down debt and rebuild the balance sheet as we work toward investment-grade leverage metrics. During the quarter, we used excess liquidity to opportunistically prepay over $1 billion of debt while still retaining $7.3 billion off the peak.

But then, so whether that's price or whether it's enterprisevalue, we can, there's applications for each. They were piling up the cash, tremendously cash generative debt free. Here's our target return on invested capital. He founded the company 32, 33 years ago. Then the stock got continually whacked.

And following the Fitch upgrade in July, our balance sheet now has two investment-grade ratings and our dividend yield is in line with the S&P 500. Strong cash generation has supported debt repayment of $2.4 Congrats on the investment grade here. I'm incredibly proud of the Delta people for delivering these results.

per share, reflecting current market interest rates on both fixed and variable debt assumptions; and cash balances contribution from other property -- other platform investments of approximately $0.10 And they're open to buying -- their return on investment in stores is a proven financial model. They're doing that.

Deidre Woollard: They don't have a lot of debt, so they've got runway, they've got time. How do you think investors earn that right if they want to practice this expectations investing approach? Return on invested capital is posited by lots of investors as being a really simple and grounded and rational way to look at a company.

billion stays on the balance sheet to fund the future investments? And how much additional debt you expect to take on in order to get to the 6.5 We think our unique asset set allows us to drive enterprisevalue and gives us advantage in fiber. How much of the $4.9 Mike Sievert -- President and Chief Executive Officer OK.

Trades around 55 times free cash flow, 31 times enterprisevalue to forward EBITDA so the value of its debt and equity compared to its forward earnings. What it might be going on here is a bit of investment. When you invest in your capital base and make it bigger, that lowers your return on invested capital.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content