This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And many of the biggest companies in the industry are happy to return that cash to shareholders. But one of its biggest competitors has returned even more cash to shareholders. T-Mobile (NASDAQ: TMUS) returned a total of $11.8 Share repurchases, on the other hand, are an indirect way to return cash to shareholders.

Over the last 20 years, Chipotle stock has put up monster returns. Posting a total return level of 7,000% since its initial public offering (IPO), the stock has crushed the S&P 500 's 459% return over that same time frame. So, what restaurant is the next Chipotle? I think a fantastic candidate is Portillo's (NASDAQ: PTLO).

Cruise lines took on a lot of additional debt during the pandemic-related shutdown in 2020 that lasted well into 2021. Its debt-saddled enterprisevalue is almost $50 billion. Reality can be kinder if Carnival uses its newfound profitability to pay down its debt and repurchase its shares. on Thursday.

Shares were issued, and debt was incurred to raise the cash needed to keep Carnival alive and see its recovery through. Investors can see Carnival's enterprisevalue below. That is Carnival's market cap plus debt minus cash on hand. Management has stated that they're pulling back on spending to pay down debt.

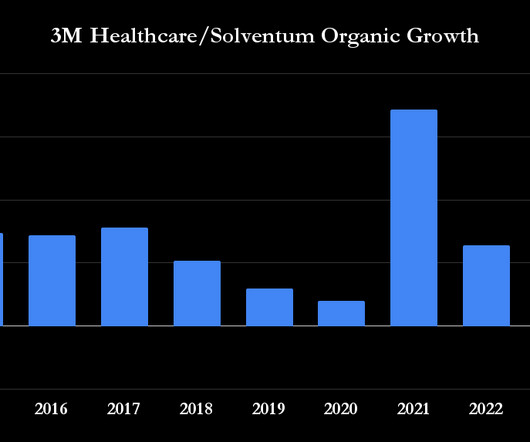

First, 3M saddled Solventum with debt to shore up the balance sheet of the former as it faces multibillion-dollar legal settlements. Wall Street expects Solventum to end the year with $7 billion in net debt, and servicing the interest on the debt is eating into FCF. In 2020, 3M sold the majority of its drug delivery business.

While operations are recovering, Carnival's stock is trading near its decade lows, and it's not clear if the company will be able to pay down debt quickly. The pandemic overhang Improving operations is good, but below you can see that Carnival's enterprisevalue (market cap plus debt) is still about the same as it was before the pandemic.

That's more than 40% of MicroStrategy's current enterprisevalue of $9.4 However, its rising BTC impairment charges also caused it to stay unprofitable over the past three years, while its issuing of fresh debt to fund its BTC purchases boosted its debt-to-equity ratio to 3.0. And with an enterprisevalue of $2.9

billion in growth capex a year would allow it to pay its distribution while having money left over from its cash flow to pay down debt and/or buy back stock. For example, a $100 million project with an 8x multiple would generate an average return of $12.5 Price at 10x multiple $26 $27 $28 $29 $30 * Enterprisevalue is based on 3.42

When it recently bought Seagen, a cancer biotech with advanced therapeutic technology, it was willing to take on $31 billion of debt to make the purchase. billion in debt, giving it a debt-to-equity ratio of 0.7. The 10 stocks that made the cut could produce monster returns in the coming years. It also has just over $68.7

The cruise line operator's revenue plunged in 2020 and 2021 as global travel ground to a halt during the pandemic, and it was forced to take on a lot more debt to stay solvent. billion, and for it to return to full-year profitability with $1.2 billion in long-term debt, but that figure hit a whopping $29.5 NYSE: CCL).

MicroStrategy's Bitcoin holdings now account for 30% of its enterprisevalue of $46.9 That rally would boost the value of its current Bitcoin holdings to $2.94 That's 35% of its enterprisevalue of $4.83 It ended its latest quarter with a seemingly low debt-to-equity ratio of 0.1,

However, Chevron is by far the largest, with a nearly $320 billion enterprisevalue compared to Occidental's at over $80 billion. billion of debt. billion of debt and about $1.2 That exceeded the company's long-term target to get debt below $15 billion. billion of CrownRock's existing debt. billion of cash.

Driven Brands has an enterprisevalue of $5 billion (for the record, this is technically a mid-cap stock, not a small-cap stock). That means the company is valued at just 9 times its profits. I mentioned enterprisevalue and EBITDA because these are metrics commonly used for companies with high levels of debt.

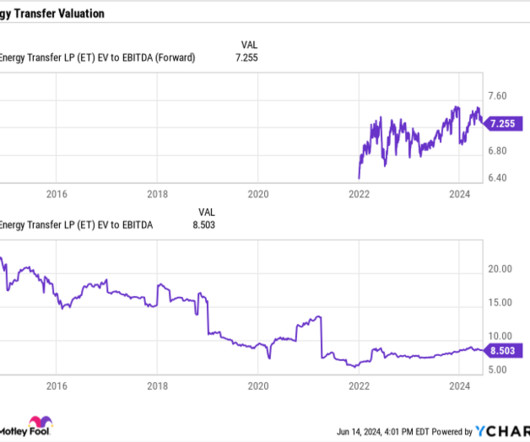

However, I appreciate the significant help that strong dividends provide in achieving solid total returns. Granted, the company slashed its distribution in 2020 because it needed to pay down debt. However, Energy Transfer's debt load isn't as problematic now. It's not that I depend on dividends for income right now.

As for the cost of acquiring Sierra Wireless, Semtech paid an enterprisevalue of $1.2 At the end of July, Semtech reported cash and short-term investments of $148 million, and total debt of $1.86 In October, management noted it sold another $250 million of convertible debt to help fund operations. Data by YCharts.

Momentum has returned in favor of the cruise lines, accolades long overdue after the prolonged shutdown of leisure fleets since the onset of the COVID-19 crisis. There's been a lot of dilution since the pandemic forced the industry into taking out more debt and issuing more stock to stay afloat. Its debt load has more than tripled.

It's trading for 26 times trailing earnings, and given its debt-bloated balance sheet, that multiple jumps to nearly 60 if you swap out market cap for enterprisevalue as the numerator. Carnival and its peers had to load up on debt at high rates or sell new shares at low prices to stay afloat. cruise was able to set sail.

Ongoing challenges for Carnival Unfortunately for Carnival, the legacy of the pandemic continues to haunt the cruise line -- namely, in the form of its $35 billion total debt, most of which it accumulated to survive an extended shutdown during the pandemic. The debt hurts Carnival in numerous ways, and not just with its ongoing net losses.

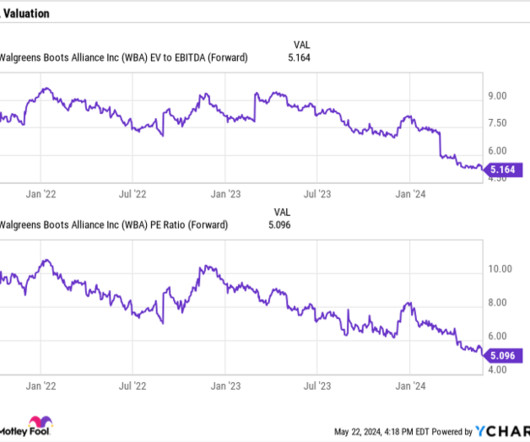

billion in net debt, not including operating leases, an ill-advised investment was not a good use of cash. At a forward price-to-earnings (P/E) ratio of about 5 and enterprisevalue (EV)- to-EBITDA ratio of 5, Walgreens stock is inexpensive. The latter metric takes into account its net debt and takes out non-cash items.

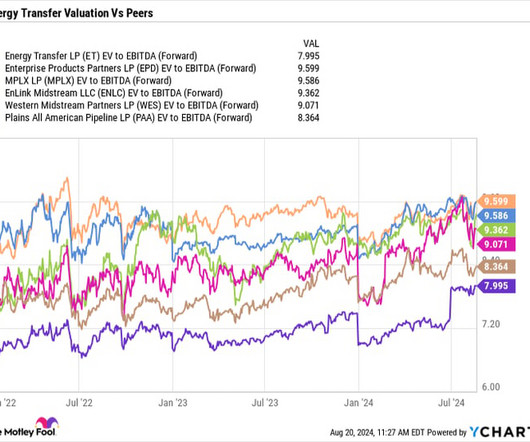

times on an enterprisevalue (EV) -to-forward EBITDA basis, the stock is attractively valued both compared to its midstream peers and on a historical basis. I prefer to use this metric when valuing midstream companies, as it takes their debt into consideration, and excludes non-cash items such as depreciation.

billion in long-term debt and a staggering debt-to-equity ratio of 70. With an enterprisevalue of $23.4 billion (which includes all of its long-term debt), it trades at just 1.8 The 10 stocks that made the cut could produce monster returns in the coming years. It's also still saddled with $18.4

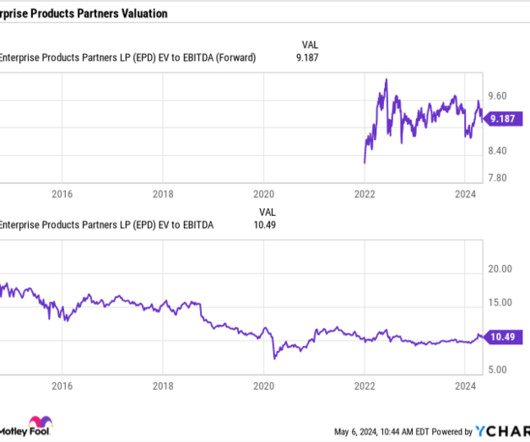

Enterprise ended the quarter with leverage of 3x. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. What this means for investors in simpler terms is that Enterprise's distribution payout is well covered by its cash flow. It currently has $6.9

Earlier this year, Medical Properties even cut its dividend almost in half in September in order to help it pay off debt and increase flexibility. However, Medical Properties also has a massive amount of debt, as most real estate companies do, making the valuation on an enterprisevalue basis much higher.

Microstrategy (NASDAQ: MSTR) continues its incredible run as the company sells more debt and equity to buy more Bitcoin (CRYPTO: BTC). As Microstrategy becomes a pure Bitcoin play, if the enterprisevalue of the company exceeds the value of the Bitcoin on the balance sheet, it will issue shares to buy Bitcoin.

Even more disappointingly, the business has been at the forefront of management's corporate actions in recent years, with management buying M*Modal's health information services business for an enterprisevalue of $1 billion in 2018. billion in net debt. It then bought wound care business Acelity for a consideration of $6.7

But investors should know the company does have a lot of debt on its balance sheet. This brings its enterprisevalue up to around $37 billion compared to its market cap of $24 billion. I think a better earnings ratio for Delta is enterprisevalue-to-free cash flow (EV/FCF) instead of the traditional P/E.

At 27 times free cash flow (and Disney is even more expensive when debt is considered -- its enterprisevalue-to-free cash flow ratio is closer to 32x -- investors are crediting Disney stock with much more than the 17% long-term annual growth rate it's projected to achieve. .* The Motley Fool has a disclosure policy.

billion in net debt since its spending spree began. The company's debt and share dilution will likely continue, as Microstrategy recently announced two convertible notes at $800 million and $600 million to fund its latest Bitcoin spending spree. The 10 stocks that made the cut could produce monster returns in the coming years.

It's true that Carnival's multiple is substantially higher if we base it on enterprisevalue instead of the garden variety market cap. Carnival and its rivals had to raise a lot of debt when they weren't issuing new shares to literally and figuratively stay afloat in the wake of the pandemic. It has repurchased $6.6

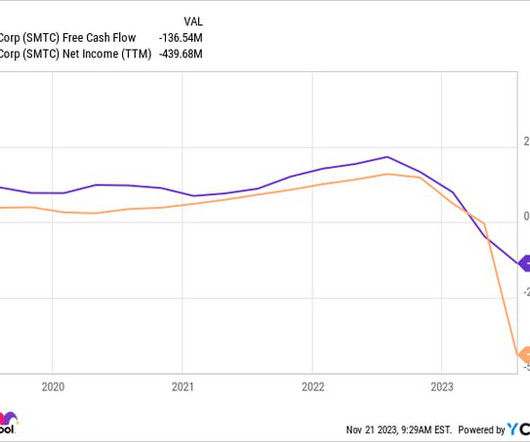

While it may not sound like much, a 25-year-old adding $100 monthly at the S&P 500 index's average return of 10.2% (from 1957 to 2022) would wind up with $591,000 in 40 years. Though the company's SBC returned to normal(ish) levels in the first quarter of 2023, it still equaled roughly 26% of sales. Data by YCharts.

Chevron managed the ongoing tensions, and the stock's total return -- including dividends -- outpaced that of the S&P 500 through the third quarter last year. But management has been able to keep its debt under control while not being afraid to use debt to expand the business. they offer a slight discount to Chevron (6.3)

The company now holds a significant amount of debt. Management plans to divest non-core assets to accelerate the paydown of that debt. Shares currently trade for an enterprisevalue/earnings before interest, taxes, depreciation, and amortization (EV/ EBITDA ) multiple of just 5x. By comparison, Chevron trades for a 6.6x

That marked the first time its total cash and BTC holdings exceeded its total debt. Marathon's revenues are soaring, but it isn't consistently profitable on a generally accepted accounting principles ( GAAP ) basis, and it's taking on a lot of debt to expand its mining operations. With an enterprisevalue of $6.1

Many of these companies rely on debt instruments for financing, which becomes more expensive when rates rise. Consequently, some small-cap stocks are currently trading at negative enterprisevalues -- a rare occurrence. The 10 stocks that made the cut could produce monster returns in the coming years.

billion in long-term debt with $1.6 With an enterprisevalue of $21 billion, Lumen might seem cheap at 1.6 billion in long-term debt from its streak of big acquisitions across the chip and software sectors. The 10 stocks that made the cut could produce monster returns in the coming years.

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 < Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6

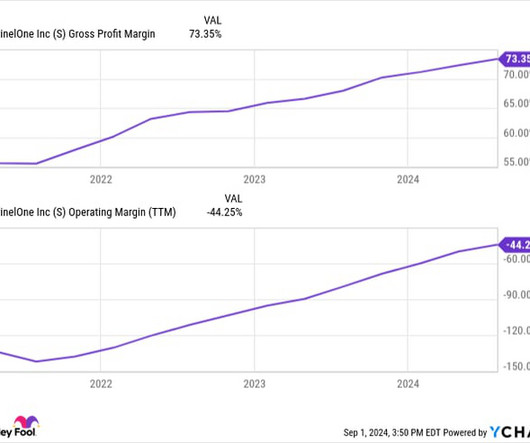

On an enterprise-value -to-revenue basis, SentinelOne is the cheapest relative to its peers by a wide margin. If improvements in its financials lead the market to conclude the company merits a dramatically higher valuation, market-beating returns should follow. Yet Wall Street apparently disdains this top-tier security company.

billion and a market value of $24.5 MicroStrategy's Bitcoin portfolio is equal to about a third of the company's enterprisevalue of $73.3 It's also taking on a lot more debt and issuing more shares to fund those purchases. dollar, the value of its Bitcoin holdings should easily cover its dollar-based debt.

Also noteworthy: According to data from S&P Global Market Intelligence , if you net out Planet Labs' cash and debt, the company's enterprisevalue drops to just $591 million -- less than 3x trailing-12-month sales. See the 10 stocks *Stock Advisor returns as of June 5, 2023 Rich Smith has positions in Planet Labs Pbc.

One, Infinera does have a notable debt load of $683 million against $165 million in cash. So on an enterprisevalue basis , it's not quite as cheap. See the 10 stocks *Stock Advisor returns as of August 1, 2023 Billy Duberstein has no position in any of the stocks mentioned. and Infinera wasn't one of them!

Analysts see a return to revenue growth in the second half of this year, followed by a bottom-line recovery in 2025. Disney returned to box office dominance this summer with the world's two highest-grossing films of 2024, and it has two movies coming out over the holidays that should fare even better. Disney+ is finally profitable.

At its peak, Nikola had an enterprisevalue of $28.7 Instead, it was being valued based entirely on the ambitious production targets it set during its pre-merger presentation in March 2020. Nikola ended the second quarter of 2023 with $615 million in total liabilities, which gave it a debt-to-equity ratio of 1.2.

Chevron's capital discipline shone through in 2022, when its return on capital employed (ROCE) hit 20%, a level last seen in 2011. While that reveals Chevron's capital efficiency, it also means large potential returns for shareholders. Pare debt and maintain a strong balance sheet. billion, including debt.

Carnival's enterprisevalue already sits within shouting distance of pre-pandemic highs. Enterprisevalue is important because there is more to a company than how much people are willing to pay for its stock -- like debt, for example. Carnival had modest debt before the pandemic and earned $4.42

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content