This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I have never been more excited about these prospects as we begin to unfold this multiyear strategy with the opening of Celebration Key in just about six months. times net debt to EBITDA, closing in on our expectation to reach investment-grade leverage metrics in 2026. billion of debt, over $8 billion off the January 2023 peak.

Since early 2024, we achieved significantly better results than in 2023 as our business, sales teams, and markets is on better footing, as evidenced by our ability to generate record Q3 results and accelerate our growth prospects by winning partnerships with some of the world's top companies. within their programmatic platform.

billion indirectly through share repurchases, all while reducing debt 35%. And we continue to improve our capital efficiency by leveraging technology and innovation across both our foundational and emerging assets. And it reflects our confidence in the increasing capital efficiency of our business going forward.

The oil company has been slowly monetizing that position to raise cash to repay debt. The MLP expects its leverage ratio to end the year at 3 times, down from 3.7 That's much lower than Energy Transfer, which expects its leverage ratio to be toward the lower end of its 4 times to 4.5 Occidental owns a 44.8% times target range.

During 2023, Medical Properties has found itself in need of de-leveraging and has sold off some properties to do so. Earlier this year, Medical Properties even cut its dividend almost in half in September in order to help it pay off debt and increase flexibility. What can turn the situation around? in earnings this year, but $0.85

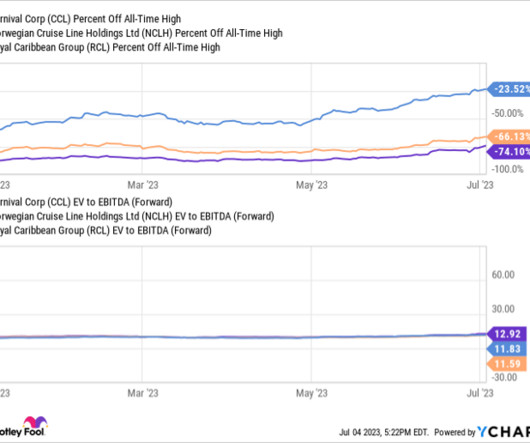

Analysts have been jacking up Carnival's fiscal 2025 prospects with every passing quarter. Carnival is tackling its debt problem Carnival and its peers had to do a lot of things to remain in business during the pandemic shutdown. Its long-term debt would go on to more than triple, peaking at nearly $33 billion a year ago.

per share, partly due to asset sales used to repay debt following a significant surge in interest rates. While adjusted FFO should improve in the next year, an analyst asked whether the company had thought more about reducing its dividend and reallocating that cash toward debt reduction. That gives it some breathing room.

KMI Financial Debt to EBITDA (TTM) data by YCharts That said, a part of the problem was Kinder Morgan's more aggressive use of leverage than its peers'. Kinder Morgan's leverage is lower today, but it still tends to use more leverage than Enterprise.

The leading North American pipeline and utility operator generates very durable cash flow and has very visible growth prospects. The company currently boasts an investment-grade credit rating backed by a leverage ratio toward the low end of its 4.5-5.0 times target range. That's less than the CA$8 billion-CA$9 billion ($5.9 billion-$6.6

But it's not bad news for debt providers because they have been rewarded for putting up capital, with their investment backed up by a relatively liquid asset, the airplanes themselves. I've also included its adjusted debt to earnings before interest, taxation, depreciation, amortization, and rent ( EBITDAR ) multiple.

Some of the information we provide during today's call regarding our future expectations, plans, and prospects may constitute forward-looking statements. As an operating business, we are able to use cash flows, as well as proceeds from equity and debt financing, to accumulate bitcoin, which serves as our primary treasury reserve asset.

Thanks to its strategy of using long-term, fixed-rate debt and keeping its leverage ratio low, it has an investment-grade credit rating. leverage ratio, which was in the middle of its 4.5-to-5.0 Enbridge also has a rock-solid financial foundation. It ended the second quarter with a 4.7 target range.

The refinancing effort includes a bid to raise an additional 40m ($51.93m) in borrowing capacity, which will help fund the companys business plan, alongside discussions to refinance 110m in existing debt. Prospective lenders are expected to engage in talks in the coming days.

The company's debt-to-equity ratio stands at 75%, and it generated operating cash flow of $35 billion over the prior 12 months. Its debt-to-equity ratio also stands at a hefty 144%, indicating that the retailer has a highly leveraged balance sheet. Target's financial picture, on the other hand, isn't quite as robust.

Over the last year or two, some of the major catalysts driving the market higher have included the prospect of lower inflation, lower interest rates, and accelerated growth in the tech sector. In the past, it has over-leveraged and left itself vulnerable to downturns. Investors looking for different ideas have come to the right place.

It has investment-grade credit, backed by a low leverage ratio and primarily long-term, fixed-rate debt. million debt maturity. That provides some visibility into its future growth prospects. EPR Properties also has a solid financial position. It ended the third quarter with $35.3

As long as demand remains strong, the cruise lines should be able to begin digging themselves out of the large debt holes they find themselves in. Given how leveraged the cruise companies are now, the prospect of a stronger-than-expected recovery in profits could juice a strong stock recovery.

But some top consumer-oriented companies quietly delivered market-beating gains and still have bright prospects. Carnival's financial position improved steadily over the course of 2023, reducing its debt balance by $4.6 As it pays down debt and lowers its interest expense, the bottom line should also improve.

The cruise line operator's revenue plunged in 2020 and 2021 as global travel ground to a halt during the pandemic, and it was forced to take on a lot more debt to stay solvent. billion in long-term debt, but that figure hit a whopping $29.5 billion in long-term debt, but that figure hit a whopping $29.5 NYSE: CCL).

The company also has a solid investment-grade balance sheet backed by a reasonable leverage ratio in the range of 4.5 billion) of annual debt capacity to fund new investments while remaining within its target range. The company also has solid growth prospects. That gives it about CA$2 billion ($1.5

Today's conference call may include forward-looking statements, including statements regarding Lennar's business, financial condition, results of operations, cash flows, strategies and prospects. reflecting our lower volume and lower average sales price leverage. debt to total capital ratio. We ended the quarter with $4.7

That's because borrowing costs on new or floating-rate debt go up, making it more expensive to fund acquisitions. Agree Realty has a strong balance sheet, and its use of leverage is low compared to its peers. and is on solid financial footing, with no debt maturing until 2028. It's been a tough stretch for real estate investors.

Chevron also has one of the strongest balance sheets in the sector, with a debt-to-equity ratio of 0.12 This is vital because it allows management to take on debt during industry downturns to keep funding the business and the dividend. When the energy market improves again, as it always has historically, leverage is reduced.

Balance sheets were stretched earlier this year, but higher stock prices could help with financial prospects. Companies will now find it easier to raise cash through share offerings or even convertible debt offerings to finance solar projects. If that's the case, any improvement would provide operating leverage if demand does return.

Its balance sheet is loaded with debt ($169 billion in net debt at the end of the most recent quarter), its near-term growth prospects are minimal due to emerging competition, and the telecom space is rapidly changing as a result of low-cost, wireless technologies that have significantly lowered the barrier to entry for newer companies.

Toolmaker Stanley Black & Decker went on an acquisition spree and ended up with too much leverage and an unwieldy product portfolio. It has been working on slimming down, trimming debt, and improving its productivity. This has been a multiyear effort, but the process is moving slowly forward.

Let's take a closer look at its most recent results, together with its future prospects and valuation, to find out. billion from $395 million a year ago, as the company continues to leverage this high-fixed-cost business. billion in debt. That was just ahead of the $84.2 billion in revenue that analysts expected.

So when you consider today's dividend yield, it may not be nearly as important as the prospects for that payout's growth. When it comes to growth prospects, there's nothing like the technology sector. This is because the company achieved its leverage target last year after five years of paying down debt.

What current and prospective investors should be focused on is AT&T's steadily improving operating performance. Discovery , AT&T earned more than $40 billion in concessions -- most of which involved the new media entity taking on select debt lots previously held by AT&T. court system, which is often slow to issue rulings.

Over the past few years, high commodity prices have padded ExxonMobil's pockets with cash, reinforcing a massive balance sheet with nearly $400 billion in assets versus just $6 billion in net debt. The company's success stems from astute management that doesn't let the balance sheet take on too much debt.

The benefits for Main Street included significant dividend income, fair value appreciation, and the realized gain, resulting in best-in-class returns on our equity investment, in addition to the attractive interest income provided by our debt investments. This compares favorably to the 4.4 times money invested return on our equity investment.

The most-aggressive rate-hiking cycle in four decades has made it costlier for companies to refinance or consummate debt-based deals. Legacy telecom companies like AT&T are carrying around quite a bit of debt. Discovery , this new media entity assumed debt lots that AT&T had previously been responsible for.

This premier protection allows AGNC to prudently deploy leverage to its advantage. AT&T closed out the March quarter with nearly $133 billion in total debt. The prospect of a big bill is worrisome for telecom companies that are already lugging around a lot of debt on their balance sheets. billion of its $63.3

Takeda's low valuation reflects a handful of important risks, such as key patent headwinds for top-selling drugs like Vyvanse, along with the company's highly leveraged balance sheet. Large-cap pharma stocks, after all, trade at an average earnings multiple of 15.1. The stock trades at a forward price-to-earnings ratio of 5.8,

This is one of the metrics most commonly used to value these companies, as it takes into consideration their net debt and the depreciation expenses associated with building out pipelines. Of the stocks highlighted above, Energy Transfer stands out for its low valuation and growth prospects and is my favorite stock in the space.

Palantir Long before AI and machine learning became buzzwords, Palantir's cutting-edge software solutions -- including Gotham, Apollo, and Foundry -- were leveraging these technologies to analyze huge troves of data and derive actionable insights for its government and commercial clients. billion total debt.

Adapting to and leveraging new technologies has been in our DNA from the start, and generative AI is pushing the pace of technology innovation faster than ever. in the fourth quarter was up versus last year by about 320 basis points due primarily to leverage from adjusted fixed operating expenses and marketing expenses.

However, growth prospects haven't improved as the country returns to normal. Sirius XM is also starting to pay down its long-term debt since that bearish leverage peaked in 2022. It's telling that revenue declined in 2023, and not 2020 or 2021. The depressed shares are currently yielding a record 3.4%.

BigBear.ai (NYSE: BBAI) and SoundHound AI (NASDAQ: SOUN) are two small-caps attempting to leverage unique AI-powered applications into long-term growth. also has more than $134 million in net debt without a clear path for generating free cash flow anytime soon. Let's explore which stock could be a better buy for your portfolio.

It has continued to reduce its leverage and now plans to finish the year with a net debt-to-adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) ratio of just 3.9. yield, another factor driving Kinder Morgan is its future earnings prospects. in dividends per share.

When we entered fiscal 2024, we were sitting with over $73 million in total debt. This followed the adverse Seaguard ruling, which added $42 million in debt, which was already too high given contributing losses at that time. This provided us with $48 million in gross proceeds, which we used to pay down debt. 1 priority.

The company also has $33 billion of long-term debt on its balance sheet. However, there are reasons for investors to be optimistic about this top auto stock 's prospects. Once these sales ramp up, and the business can benefit from operating leverage, profitability should hopefully follow. Revenue of $41.5 were up 66%.

The best way to ensure you're always a step ahead of Wall Street is to hold shares of quality companies with great prospects for long-term growth. The stock has good prospects to beat the market again. After a disappointing year for stocks in 2022, the markets have rebounded this year.

This is important for investors because it allows the company to pay out its distribution while still being able to pay down debt. When Energy Transfer cut its distribution in 2020, it was because its leverage became too high, and it needed to pay down debt. cents is now higher than the 30.5

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content