This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The private equity firms aim to refinance or reprice Adevintas existing 4.5bn debt and may raise an additional 2bn, potentially for a shareholder dividend, according to sources familiar with the matter. The firms acquired Adevinta in 2023 in one of Europes largest leveraged buyouts backed by private credit.

And with ROIC ending 2024 at 11%, comfortably above our cost of capital, we are already delivering long-term value for our shareholders as we lay the foundation we'll build upon in 2025 and beyond. times net debt to EBITDA, closing in on our expectation to reach investment-grade leverage metrics in 2026. We ended 2024 with $27.5

I am incredibly excited about this acquisition, which enhances our footprint in some of the most bet-upon sports, including tennis, soccer, and basketball, and will deliver significant value to our clients, partners, and shareholders. The deal, once closed, is expected to be immediately accretive to our business and margins.

And many of the biggest companies in the industry are happy to return that cash to shareholders. billion to shareholders over the last 12 months. billion to shareholders over the past year. But one of its biggest competitors has returned even more cash to shareholders. It sports a 5% dividend yield, paying out $8.2

We've increased our regular dividend rate 160%; and including both regular and special dividends, paid or committed to pay more than $13 billion directly to shareholders; and $3.2 billion indirectly through share repurchases, all while reducing debt 35%. EOG continues to create long-term shareholder value. We generated $1.6

This strategy continues to pay big dividends for shareholders. With further improvements ahead, the company continues sending more cash to its shareholders. Sending more cash to shareholders Devon used some of its free cash flow to strengthen its already solid balance sheet. billion, putting its net leverage ratio at around 0.6

reflecting our lower volume and lower average sales price leverage. debt to total capital ratio. We are extremely well positioned to spin Millrose and to be able to continue to repurchase shares and reduce debt as we have driven strong overall operating results to date. million shares for over $2 billion in cash.

It was a cash bonanza for shareholders. But the benefit for shareholders of this dividend change was pretty intense. The remaining 25% is set to go toward debt reduction, which should position the company well for when the next material industry downturn comes along. To be fair, Pioneer isn't wildly over leveraged.

We have a packed agenda lined up for the next three days, and we're excited to see our customers, partners, analysts, shareholders, and employees, all in person to share our passion for BI, AI, bitcoin, and innovation. billion in equity in a manner that we believe to be creative to existing shareholders. Debt financing.

Trust in superior capital allocation Capital allocation in the oil space can be difficult because a company's survival is often prioritized over shareholder profits. How can we tell how good a company has done at investing shareholder wealth? Buffett likes companies that put shareholder interests first. of the company.

In his 1988 annual letter to shareholders, Buffett penned that when it comes to owning outstanding businesses with excellent management, "our favorite holding period is forever." As for why Buffett's love grew for Apple, the company returns an incredible amount of capital to its shareholders in the form of dividends and share buybacks.

Its long-term debt consequently skyrocketed from around $11 billion to over $35 billion in a matter of months. CCL total long-term debt (quarterly) , data by YCharts. But now that the company is sailing again, it has to get its debt down to something more manageable. What's encouraging is that its debt is already down $4.6

In the quarter, we continue to execute against our strategy that is driving long-term growth and shareholder value. We're very pleased with Enact's operational strength's capital levels and consistent shareholder distributions. Our first priority is to create shareholder value through Enact's growing market value and returns.

Despite achieving substantial debt reduction and strategic advancements, Viatris fell short of analysts' forecasts. Viatris made significant strides in reducing its debt by $3.7 billion, achieving a leverage ratio of 2.9. Despite these hurdles, Viatris reported a 26.1%

Following my comments, Dave and Ryan will provide additional comments regarding our investment strategy, investment portfolio, financial results, capital structure and leverage, and our expectations for the fourth quarter, after which we'll be happy to take your questions.

But shareholders will likely see huge dividend increases when oil prices are high. It also needs to have a sound financial foundation, otherwise cash will have to be put toward debt reduction and interest costs instead of dividend payments. Those European energy companies carry higher levels of debt than U.S.

This move, while not directly affecting the value of shareholders' portfolios, opened the door to more investors who lack access to fractional shares and therefore couldn't afford the hefty share price before the split. Nvidia, for example, has a debt-to-equity ratio of just 0.5, The stock is up over 10% since the split.

Filling them up, therefore, allows the company to leverage these high fixed costs and turn a higher profit. With its strong profitability, the cruise line rewarded shareholders with share repurchases and a high-yield dividend. It made good progress in fiscal 2023 by bringing its debt down by $4.6 billion from its peak.

That should enable them to produce more free cash to reduce debt and support their dividends. times leverage ratio , down from 2.7 Verizon plans to continue using its excess free cash to repay debt. The company's long-term target is to get leverage between 1.75 Verizon ended the second quarter with a 2.6

GFL plans to use approximately CAD3.75bn of the CAD6.2bn net proceeds from the sale to reduce its debt, aiming to bring its net leverage ratio down to 3.0x. The remaining funds, up to CAD2.25bn, are earmarked for opportunistic share repurchases, enhancing shareholder value.

for the full year, strong levels of NII per share and DNII per share to fund our record level of annual shareholder dividends, and a new record for NAV per share for the 10th consecutive quarter. Our positive performance in all four quarters for the year resulted in a return on equity of 19.4%

The strategy includes investing fresh software-business cash flows into more Bitcoin holdings, taking on new debt, and selling stock on the open market to finance further cryptocurrency buys. The ETFs simply buy and sell Bitcoin to match their shareholders' demand for the cryptocurrency.

Dividends compensate patient shareholders for enduring the cyclicality of the oil patch. Operating a massive portfolio of green energy assets, Brookfield Renewable has demonstrated a strong commitment to rewarding shareholders, and its 4.8% The energy and utilities sectors are known for their high yields.

Invesco S&P 500 Quality ETF: Up 240% over the last decade The Invesco S&P 500 Quality ETF measures the performance of the S&P 500 Quality index, which itself attempts to track the highest-quality S&P 500 companies as measured by three metrics: return on equity (ROE), balance sheet accruals (BSA) ratio, and financial leverage ratio.

We continued our impressive debt reduction journey in 2024 as well, ending the year with $790 million in holding company debt, down from $4.2 Our first priority is to create shareholder value through our approximately 81% ownership stake in Enact. billion at the beginning of 2013 and from $856 million at the end of 2023.

Why the stock scares off some investors The debt-to-equity (D/E) ratio of DigitalOcean is a negative 675% due to total debt of $1.47 billion and negative shareholder equity of $217.7 This ratio measures a company's financial leverage. You can calculate it by dividing the company's total debt by shareholder equity.

billion of that company's debt. Furthermore, the company is on pace to reach its leverage ratio target of around 2.5 The investment bank believes the company will see improved revenue in the future and could potentially start buying back its shares, given the improvement in its leverage ratio.

Between now and then, it'll need to repay more than $6 billion in debt. Even if it devoted 100% of its CFO toward paying down its debt -- which would mean cutting its dividend to zero -- it would still take more than 11 years to fully repay its loans. Refinancing higher-interest-rate debt would be a necessity.

Apple has the cash to step in and buy its stock, thereby reducing the share count and giving existing shareholders greater ownership of the company. Granted, it only yields 0.6%, but it's still a massive capital commitment for Apple to its shareholders. billion, while its term debt was $106 billion.

Debt and dividends leave AT&T and Verizon vulnerable Because they have paid out such hefty dividends and made the expensive C-band investments, AT&T and Verizon also have larger debt loads. While AT&T was able to offload some of its debt to Warner Bros. Image source: Getty Images. Verizon $152.9 $2.2

Leveraging the balance sheet to drive investment returns A franchise network of thousands of pizzerias creates durable cash flows. Domino's has taken advantage of that by strategically using its balance sheet to return money to shareholders. DPZ Financial Debt to EBITDA (TTM) data by YCharts.

In short, there's a lot of leverage in the investing world. PubMatic For investors worried about what the global economy might do, it can be a good idea to invest in cash-rich and debt-free companies. It has $174 million in cash with no debt, which is quite substantial for a company that's valued at less than $1 billion.

This is because the company achieved its leverage target last year after five years of paying down debt. The high debt load was the result of its massive $10.3 Since the company brought its debt down to comfortable levels, it has been increasing its payouts to shareholders methodically every quarter.

The company's debt-to-equity ratio stands at 75%, and it generated operating cash flow of $35 billion over the prior 12 months. Its debt-to-equity ratio also stands at a hefty 144%, indicating that the retailer has a highly leveraged balance sheet. Valuation, shareholder rewards, and outlook Walmart stock trades at 28.9

During this time, I have connected with shareholders, customers and clients. The combination of these measures will ultimately deliver greater shareholder value. We're also leveraging AI to create a more intuitive workflow and faster turnaround times to reduce frustrations for our members and provider partners.

Companies that regularly dole out a dividend to their shareholders tend to be profitable on a recurring basis, are time-tested, and can provide investors with transparent long-term growth outlooks. What this added protection does is allow AGNC to deploy leverage to bolster its profits and sustain its juicy payout. All but $0.1

In the past, it has over-leveraged and left itself vulnerable to downturns. However, ExxonMobil has improved its balance sheet significantly since then, taking advantage of outsize gains in recent years to pay down debt. Despite its dominant position, ExxonMobil isn't a perfect company. for every dollar in earnings toward the dividend.

Companies that pay dividends display a commitment to shareholders and tend to have prudent capital management. dividend yield The Blackstone Secured Lending Fund is a business development corporation ( BDC ) that invests in private company debt to generate income for dividend-focused investors. Ares Capital has a 9.7%

Meanwhile, it pays out a reasonable percentage of that stable cash flow to shareholders in dividends (60% to 70%). leverage ratio , putting it at the low end of its 4.5-5.0 The natural gas infrastructure giant pays out a conservative portion of that steady cash to shareholders (its dividend payout ratio should be around 53% of its $4.8

Over the next several years, the company expects to free up another $1 billion in annual free cash flow due to cost savings related to its midstream and downstream assets, plus reductions to its total debt levels. Over the past decade, oil prices have fallen by around 18%, yet Chevron stock has risen by nearly 100%.

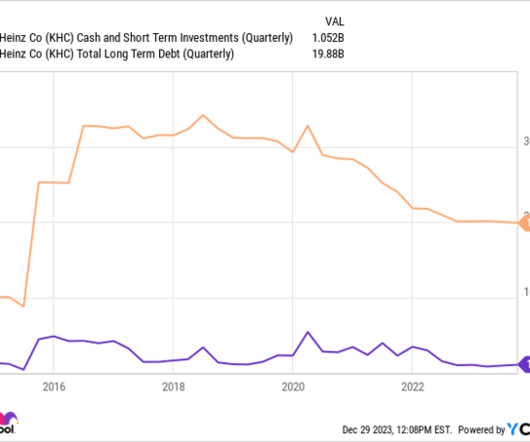

Here are three reasons why the future looks bright for Kraft Heinz and its shareholders in 2024 and beyond. However, the merger also loaded up the new entity with debt. Below, the merger more than tripled the company's debt to over $30 billion. But management has brought leverage down to 2.9 Is it stubbornness?

And we'll have more to come on our plans to increase awareness and consideration for our brands as we leverage our underexposed portfolio of Caribbean destinations. While we were not actively looking to sell the ship, the offer was in the best interest of our shareholders. billion of debt maturities for the remainder of 2025 and 2.7

Though a 15% yield is typically viewed as unsustainable for most companies, Annaly has supported an average yield of around 10% over the past two decades and returned $25 billion to shareholders since its initial public offering in 1997. This leverage allows Annaly to maximize its profit potential and sustain a double-digit yield.

Private credit has become an integral part of the financing solutions available to support corporate growth and there is an increasing demand for debt capital from well-established and high-growth software and technology businesses, which typically have leading market positions, resilient customer base and strong financial fundamentals.”

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content