This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

On top of that, interest rates surged, affecting the company's ability to refinance maturing debt at acceptable rates. A significant percentage of its properties had leases with two tenants : Steward Health Care and Prospect Medical Holdings. For example, last year, it reconstituted its investment in properties related to Prospect.

I have never been more excited about these prospects as we begin to unfold this multiyear strategy with the opening of Celebration Key in just about six months. times net debt to EBITDA, closing in on our expectation to reach investment-grade leverage metrics in 2026. billion of debt, over $8 billion off the January 2023 peak.

not leased to Steward Health Care or Prospect Medical Holdings. This stabilized portfolio generates steady cash flow that the company uses to pay dividends and repay debt. portfolio, excluding hospitals leased to Steward and Prospect, is seeing increased admissions. billion) and Prospect ($1.1 Meanwhile, its U.S.

During the third quarter, we continued to advance our strategy of generating additional liquidity to accelerate debt paydown and enhance financial flexibility. During the quarter, MPT and our JV partner increased the equity investment in infracore by retiring approximately 50 million Swiss francs in maturing third-party debt.

Spirit stock subsequently fell by more than 20% as investors get more and more pessimistic about its prospects. The company's balance sheet is ugly, with $316 million in short-term debt, $3 billion in long-term debt, and over $3 billion in operating lease liabilities.

Investors have become excited about the company's long-term prospects, as it has a promising weight-loss drug in its portfolio. Viking's balance sheet looks strong While Viking has an exciting asset in its portfolio, the numbers still have to work for a prospective buyer. And its total liabilities were just $20 million.

This is a function of investors being concerned following a July report from The Wall Street Journal that alleged legacy telecom companies utilizing lead-sheathed cables could face large environmental/health liabilities, as well as replacement costs. Furthermore, any potential liabilities would likely be determined by the U.S.

AT&T closed out the September quarter with $138 billion in total debt. The intimation is that the replacement of these cables, along with potential health-related liabilities, could be quite costly for telecom companies. It also fails to consider that any liability costs (if there are any) would be determined in the U.S.

The most-aggressive rate-hiking cycle in four decades has made it costlier for companies to refinance or consummate debt-based deals. Legacy telecom companies like AT&T are carrying around quite a bit of debt. Discovery , this new media entity assumed debt lots that AT&T had previously been responsible for.

AT&T closed out the March quarter with nearly $133 billion in total debt. The other reason its shares have been weighed down relates to a July report from The Wall Street Journal that alleges legacy telecom companies may face steep health-related liability and cleanup costs tied to their use of lead-sheathed cables. court system.

If we only look at its software business, MicroStrategy's near-term prospects aren't impressive. It's also taking on a lot more debt and issuing more shares to fund those purchases. dollar, the value of its Bitcoin holdings should easily cover its dollar-based debt. If Bitcoin's price skyrockets against the U.S.

billion indirectly through share repurchases, all while reducing debt 35%. To optimize EOG's capital structure going forward, we intend to position our balance sheet such that our total debt-to-EBITDA ratio equals less than one times at $45 WTI. Now, here's Jeff to review operating results. This is a new wrinkle from the company.

With its liabilities totaling $33.6 million as of the end of March, Viking doesn't have a ton of obligations or debt on its books and its has close to $1 billion in cash and short-term investments. Its strong financial position could sweeten the deal for a prospective acquirer looking to add a promising GLP-1 drug to its portfolio.

Lumen is a debt-riddled company whose stock became distressed earlier this year. However, an early-year deal to extend its debt maturities, combined with long-term deals for AI (artificial intelligence) networking, caused the stock to skyrocket in early August. billion in debt and pension liabilities. as of 2:23 p.m.

But the most exciting development for Philip Morris and its prospective and existing shareholders is the growth it's seen in its smokeless tobacco products. This concern, coupled with rapidly rising interest rates (legacy telecom companies are lugging around quite a bit of debt), weighed heavily on the industry.

The business carries a whopping $7 billion of debt and operating lease liabilities. It's hard to have any sort of confidence as it pertains to Spirit's prospects. And they all registered positive operating income in that period. It also should surprise no one that Spirit's balance sheet leaves much to be desired.

Decrease in net sales was driven by a 12% decrease in the volume of megawatts sold and the aforementioned increase in our Series 7 product warranty liability, partly offset by expected payments associated with contract terminations in the U.S., billion net of debt. Net sales in the third quarter were $0.9 billion, a decrease of $0.1

Since early 2024, we achieved significantly better results than in 2023 as our business, sales teams, and markets is on better footing, as evidenced by our ability to generate record Q3 results and accelerate our growth prospects by winning partnerships with some of the world's top companies. million in Q3 2023. in Q3 2024, compared to $0.09

Modest growth prospects, rising interest rates that have made bonds more attractive, and macroeconomic headwinds that have dissuaded consumers from spending more on phone plans have led to increased price competition among the big three telecoms, which also includes T-Mobile. billion-$12.5

In 2023, the company's shares have plunged by nearly 23% over concerns about its free-cash-flow generation in the back half of the year, potential liability over legacy infrastructure, a high debt load, limited growth prospects, as well as the emergence of low-cost competitors.

On the institutional side, our continued leadership in pension risk transfer was reinforced through a second transaction with IBM, this time to reinsure $6 billion of pension liabilities. We also maintain a well-diversified, high-quality portfolio and disciplined approach to asset liability management.

A company uses FCF for activities such as investing in its business, paying debt, performing share buybacks, and funding a dividend. billion in total assets on its balance sheet versus $119 billion in total liabilities. Factors such as its growth prospects and competitive strength should also play a role in a decision to invest.

In both cases, so-so demand for the iPhone 15 now portends so-so prospects for the iPhone 16 likely to debut later this year. It's cash-rich with modest debt It might be growth-challenged right now, but there's no company better equipped to shrug off the impact of such a headwind. But what about debt? Chart by author.

The company's total liabilities are just a little more than that amount, with practically none of that being long-term debt. High risk, high reward Again, a prospective buyout alone is a lousy reason to own any company; the rumors don't seem to come to fruition as often as investors may like.

Today's conference call may include forward-looking statements, including statements regarding Lennar's business, financial condition, results of operations, cash flows, strategies and prospects. debt to total capital ratio. And then turning to our debt position, we had no redemptions or repurchases of senior notes this quarter.

Given the rapid pace of additive technology evolution for both healthcare and industrial applications, we have great confidence in our longer-term growth prospects. The largest use of cash during the year was $87 million used to repurchase $111 million of debt in March. And I'm thrilled with the prospects.

When we entered fiscal 2024, we were sitting with over $73 million in total debt. This followed the adverse Seaguard ruling, which added $42 million in debt, which was already too high given contributing losses at that time. This provided us with $48 million in gross proceeds, which we used to pay down debt. 1 priority.

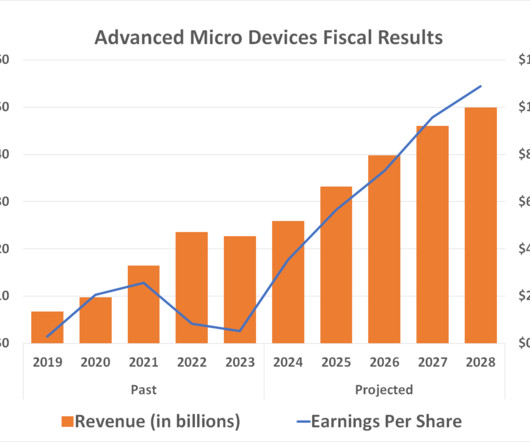

This may be an instance, however, where the second-place name is actually the top investment prospect among the companies in question. Advanced Micro Devices is practically debt-free Last but certainly not least, AMD carries very little debt, and could be debt-free if it chose to be. Four charts illustrate why.

First, rising interest rates made the prospect of future debt-financed acquisitions less appealing. It also meant refinancing the company's existing debt could be costlier. Further, any liability would almost certainly be determined by the U.S. Verizon faced something of a double whammy last year.

Some of the information we provide during today's call regarding our future expectations, plans, and prospects may constitute forward-looking statements. As an operating business, we are able to use cash flows, as well as proceeds from equity and debt financing, to accumulate bitcoin, which serves as our primary treasury reserve asset.

So, how exactly does Intuitive Surgical make money, and what are the prospects for its shares going forward? The company has a solid operating margin of 26%, no debt, and over $4.7 Intuitive also has full power to create a more optimized capital structure by adding debt to reduce its cost of capital if interest rates fall.

Under the conditions of bankruptcy, it is very improbable that Steward will be able to pay its $9 billion in total liabilities, $6.6 At first glance, the prospects appear to be gloomy. Right now, its debt load totals $10.1 In that period, Steward accounted for 20.3% of the total, or roughly $68.3 million in cash and equivalents.

Mastercard has no direct liability to loan losses since it doesn't lend. Regulated utilities avoid the prospect of potentially volatile and unpredictable wholesale pricing. S&P has the utmost confidence that Johnson & Johnson can service and repay its outstanding debt. Should you invest $1,000 in Mastercard right now?

billion in total debt. Lugging around a sizable amount of debt is pretty common for legacy telecom companies. With so much debt already on their balance sheets, the last thing telecom companies need is a potential multibillion-dollar liability. Discovery taking on select lots of debt previously held by AT&T.

subsidiaries and a $190 million increase in our net liability on the former Fieldwood properties. In 2024, we made significant progress strengthening our balance sheet and are close to returning to pre-Callon debt levels only nine months after closing the acquisition. Your capital structure is getting close to 4% to 5% debt.

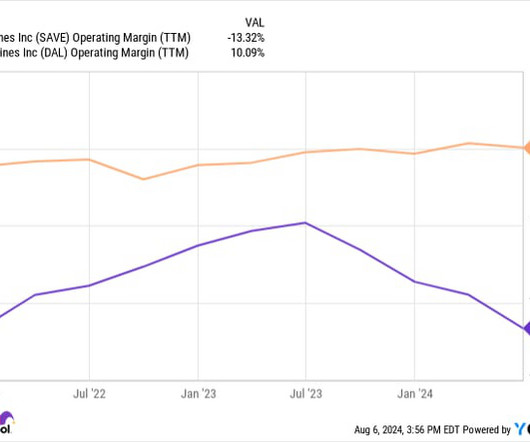

SAVE Operating Margin (TTM) data by YCharts A teetering balance sheet means trouble ahead Bad cash burn means Spirit has taken on a lot of debt in order to operate. At the end of last quarter, Spirit had less than $1 billion in cash compared to over $3 billion in long-term debt and close to $4 billion in operating lease liabilities.

But a company filing raised the prospects of bankruptcy, and the final settlement amount still remains in question. The prospect of a settlement encouraged investors that a deal would be reached that might hurt Hawaiian, but keep it solvent. So after July's run, any hiccup had the potential to send Hawaiian's stock back down.

NAV is defined as total assets minus total liabilities and is also reported on a per-share basis. We expect that these follow-on investments will provide the opportunity for additional future fair value appreciation, in addition to providing us the highly attractive incremental debt investments in these high-performing portfolio companies.

However, management has successfully reduced net debt to $2.8 EPR net debt (quarterly), data by YCharts; TTM = trailing 12 months. Prospects look promising for LTC Properties because America's aging population should keep demand for its services high. O net financial debt (quarterly); data by YCharts.

Its business bounced back , but the inflated debt burden remains. Less risk than presumed, more reward than believed There are risks with this stock; the prospect of more serious economic headwinds is one of them. billion worth of debt to less expensive interest rates. Another pandemic is always a potential tripwire as well.

Granted, it's also got a little over $3 billion worth of debt and other liabilities on the books, making its technical liquidation value less than zero. While some of that debt would be wiped out in the event of a bankruptcy, some of it wouldn't.) Apple has been floated as a prospective suitor. The company has $1.1

Telecom stocks are often lugging around a lot of debt. telecom companies could face hefty cleanup and health-related liabilities tied to their use of lead-clad cables. Even if AT&T and its peers were to have some sort of financial liability in the future, a settlement figure would be determined by the notoriously slow U.S.

During today's call, Emergent may make projections and other forward-looking statements related to their business, future events, their prospects, or future performance. However, the company needed to reduce its debt, improve profitability, and pursue future growth at a rapidly evolving landscape. Turning to Slide 2.

That means it may have wiggle room to invest in the CEO's turnaround plan and continue to pay down debt. As of last quarter, the company had roughly $9 billion in debt, along with another $5.9 As of last quarter, the company had roughly $9 billion in debt, along with another $5.9

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content