This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I have never been more excited about these prospects as we begin to unfold this multiyear strategy with the opening of Celebration Key in just about six months. times net debt to EBITDA, closing in on our expectation to reach investment-grade leverage metrics in 2026. billion of debt, over $8 billion off the January 2023 peak.

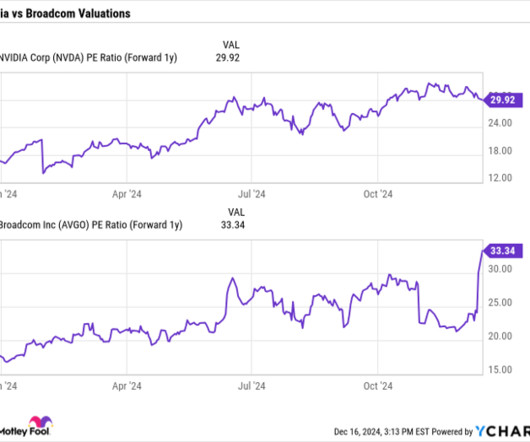

With AI models needing exponentially more computing power as they become more advanced, Nvidia's future growth prospects also look promising. billion in net debt. Through the first nine months of its fiscal 2025 ending in January 2025, Nvidia's revenue surged 135% to $91.2 billion, while last quarter its revenue soared 94% to $35.1

On top of that, interest rates surged, affecting the company's ability to refinance maturing debt at acceptable rates. A significant percentage of its properties had leases with two tenants : Steward Health Care and Prospect Medical Holdings. For example, last year, it reconstituted its investment in properties related to Prospect.

During the third quarter, we continued to advance our strategy of generating additional liquidity to accelerate debt paydown and enhance financial flexibility. During the quarter, MPT and our JV partner increased the equity investment in infracore by retiring approximately 50 million Swiss francs in maturing third-party debt.

not leased to Steward Health Care or Prospect Medical Holdings. This stabilized portfolio generates steady cash flow that the company uses to pay dividends and repay debt. portfolio, excluding hospitals leased to Steward and Prospect, is seeing increased admissions. billion) and Prospect ($1.1 Meanwhile, its U.S.

billion indirectly through share repurchases, all while reducing debt 35%. To optimize EOG's capital structure going forward, we intend to position our balance sheet such that our total debt-to-EBITDA ratio equals less than one times at $45 WTI. Now, here's Jeff to review operating results. This is a new wrinkle from the company.

From 2002 to 2013, she served as CFO and COO of Kronos Foods , a Chicago-based food manufacturer and former Prospect Partners portfolio company. Debt financing for the transaction was provided by Proterra Investment Partners. CenterPoint M&A Advisors served as the financial advisor to Felbro Food.

Investors hammered it as debt costs and growth struggles weighed on the telecom stock. Consequently, Verizon managed to rack up nearly $147 billion in debt, and that is without the costly moves into pay TV and content that have hurt AT&T. That move could reduce the effect of the higher rates as it issues new debt.

With that said, MicroStrategy is not like any other publicly traded company on the market because, facing limited growth prospects in its software business, it decided to purchase $250 million of Bitcoin in 2020 -- and hasn't stopped buying it since. Still, prospective buyers should know a few things before investing in MicroStrategy today.

Granted, the company slashed its distribution in 2020 because it needed to pay down debt. However, Energy Transfer's debt load isn't as problematic now. Earlier this year, Fitch and S&P (upgraded the company's senior unsecured debt rating. Good growth prospects Energy Transfer has perhaps surprisingly good growth prospects.

Analysts have been jacking up Carnival's fiscal 2025 prospects with every passing quarter. Carnival is tackling its debt problem Carnival and its peers had to do a lot of things to remain in business during the pandemic shutdown. Its long-term debt would go on to more than triple, peaking at nearly $33 billion a year ago.

Earlier this year, Medical Properties even cut its dividend almost in half in September in order to help it pay off debt and increase flexibility. One such sale was the sale of three hospitals to Prospect Medical Holdings. However, that sale was conditioned on Prospect then selling the hospitals to Yale New Haven Health.

Small partnership, big share sale Moving past the Milton morass, two recent news items should help prospective investors evaluate Nikola's future prospects. Finally, there's no getting around the implications of Nikola's recent debt-issuance disclosure. Should you invest $1,000 in Nikola right now?

After shutdowns left it without a significant revenue source for over a year, massive debts and a long process of returning to normalcy left its stock without an obvious catalyst. However, debt levels are the one effect of the pandemic that remains visible. 31), the total debt stood at $29.6 Nonetheless, this debt has fallen $1.7

Prospect Medical remains behind on paying rent on its California facilities and was recently hit by a ransomware attack. Medical Properties Trust reported net debt of more than $10.2 While the company's debt matures over a multiyear period, higher interest rates led to concerns about the increased costs of refinancing.

The oil company has been slowly monetizing that position to raise cash to repay debt. Those sales enabled it to recycle capital by paying down debt following its $855 million acquisition of Meritage Midstream Services. The MLP has a similarly strong financial profile and solid growth prospects. Occidental owns a 44.8%

billion of long-term debt. However, consider the fact that the debt burden is more than offset by $16.2 Not a steal anymore After the stock's 41% rise in the past six months, it's no longer a screaming bargain for prospective investors. As of Sept. 30, PayPal carried $12.4 billion in cash, cash equivalents, and investments.

After staring at the brink of bankruptcy, a debt restructuring deal rescued the stock. Should car sales fall back to last year's levels or lower, Carvana would likely return to net losses, a prospect that could derail its recovery. Moreover, despite its restructuring, the company's debt load is an ongoing concern.

You have high-interest debt If you're carrying around high-interest debt, the best investment you can make with your money is to pay off that debt. You could use that money to pay off your $5,000 in credit card debt with a 20% APR, or you could invest in a 12-month CD with a 5% APY. What counts as "high interest" here?

Any time a stock surges like that in a relatively short period, prospective investors may wonder how much bigger the company can get. So let's examine the company's recent financial results, potential risks, and prospects for growth. COST Net Financial Debt (Quarterly) data by YCharts. billion and $38.5 billion, respectively.

Credit card debt Almost a third (30%) of women in the Laurel Road survey said that they're feeling behind on credit card debt repayment. High-interest credit card debt is a poster child for "bad debt." If you have credit card debt, it's never too late to make a plan to pay it off. of average annual returns.

T data by YCharts AT&T's debt burden Moreover, AT&T has a strong incentive to make that move thanks to the company's massive long-term debt. This debt level now stands at $138 billion, up $4 billion from year-ago levels and well above stockholders' equity of about $118 billion.

debt problem. has $35 trillion in debt, and that figure increases by $1 trillion about every 100 days. At some point, that debt load is simply unsustainable. To pay off all that debt, the U.S. debt collapse for nearly 35 years now. Right now, the U.S. But remember -- people have been warning about a calamitous U.S.

Let's look at some important points that prospective investors must appreciate before choosing to plug this stock into their portfolios. In other words, management isn't confident the company can continue to meet its financial obligations -- something few prospective investors want to read.

A historically beaten-down valuation A company's growth prospects are only one-half of the equation. But keep an eye on the debt Outside of competitive pressure, there's one thing that AT&T investors should be concerned about: Debt. AT&T took this a step further and funded some of its media buying spree with debt.

It's not just this growth, however, that makes Cava stock such a compelling investment prospect. Lack of debt Even more impressive is that the company's expanding without taking on debt. In fact, it's free of any long-term debt. That is, while the restaurant chain might remain debt-free, it's still raising money.

billion means it trades at less than eight times its lowest FCF in the last three years, an extremely low valuation for a company that arguably has growth prospects now its freed from a struggling parent company. Management is candid that paying down debt is a strategic priority over the next two years.

Over the past six years, we have been privileged to help shepherd the tremendous growth and industry-leading performance of Combined Caterers, both of which made the company such an attractive prospect for CCMP Growth, said Marc Oken , co-founder and chairman of Falfurrias. 2024 Private Equity Professional | December 10, 2024

Many top healthcare stocks provide investors with long-term stability, promising growth prospects, and in some cases even a dividend. It has around $37 billion in long-term debt on its books at a time when interest rates are high. It's not hard to see why investors might not be all that thrilled.

The cruise line operator's revenue plunged in 2020 and 2021 as global travel ground to a halt during the pandemic, and it was forced to take on a lot more debt to stay solvent. billion in long-term debt, but that figure hit a whopping $29.5 billion in long-term debt, but that figure hit a whopping $29.5 NYSE: CCL).

But on the other hand, it could get a big one-time payday from a part of the business with low prospects for growth. As of the first quarter of 2024, Kraft Heinz had nearly $20 billion in long-term debt -- an exorbitant amount that cost the company over $900 million in interest expenses in 2023. Would it be a good move for Kraft Heinz?

Spirit stock subsequently fell by more than 20% as investors get more and more pessimistic about its prospects. The company's balance sheet is ugly, with $316 million in short-term debt, $3 billion in long-term debt, and over $3 billion in operating lease liabilities.

But it's not bad news for debt providers because they have been rewarded for putting up capital, with their investment backed up by a relatively liquid asset, the airplanes themselves. I've also included its adjusted debt to earnings before interest, taxation, depreciation, amortization, and rent ( EBITDAR ) multiple.

While AT&T faces intense competition from other telcos, perhaps bigger concerns linger around the company's high level of debt on the balance sheet. This has led to increasing revenue, and more importantly, a steadily declining debt load. 30, AT&T's total debt was $138 billion -- down from $143 billion at the end of Q2.

The company's debt-to-equity ratio stands at 75%, and it generated operating cash flow of $35 billion over the prior 12 months. Its debt-to-equity ratio also stands at a hefty 144%, indicating that the retailer has a highly leveraged balance sheet. Target's financial picture, on the other hand, isn't quite as robust.

Prospect Medical Holdings 14 7.5% That became an issue as Steward Health Care and Prospect Medical Holdings ran into financial troubles. billion investment in properties leased to Prospect Medical Holdings in a series of transactions. It has had to sell properties leased to financially stronger tenants to repay maturing debt.

Still, shareholders and prospective investors are reasonable to ask the question: How much bigger can Microsoft get? billion in net cash (cash and cash equivalents minus total debt) as of its most recently reported quarter. So, let's look at its recent key financial metrics, what could go wrong, and its future growth potential.

In the past 12 months, Amgen's stock has risen by only 8%, as investors don't appear to be overly enthusiastic about its prospects, despite its potential in the GLP-1 drug market. billion while leaving plenty of money to reinvest in its operations and pay down its debt. Last year, the company also generated $10.4

So when you consider today's dividend yield, it may not be nearly as important as the prospects for that payout's growth. When it comes to growth prospects, there's nothing like the technology sector. This is because the company achieved its leverage target last year after five years of paying down debt.

It has investment-grade credit, backed by a low leverage ratio and primarily long-term, fixed-rate debt. million debt maturity. That provides some visibility into its future growth prospects. It ended the third quarter with $35.3

The good news for Signet Taking the company's broader competitive position and future prospects into account, the sell-off seems exaggerated. Finally, the company is improving its balance with debt repayment, and the preferred share repurchase program should continue to pay off into next year. Image source: Getty Images.

Today's conference call may include forward-looking statements, including statements regarding Lennar's business, financial condition, results of operations, cash flows, strategies and prospects. debt to total capital ratio. And then turning to our debt position, we had no redemptions or repurchases of senior notes this quarter.

If you have market research expertise, you can also make good money with an online side hustle to help companies and organizations understand their brand reputations, their prospective customers' opinions, and make better-informed decisions. More companies than ever before are open to hiring people like you to work from home in flexible ways.

When investors are optimistic about a company's near-term growth prospects, they may be willing to pay a premium price for the stock. It has an impeccable balance sheet , with more cash, cash equivalents, and marketable securities than long-term debt. Investors may be wondering why a company at the cutting edge of AI is such a bargain.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content