This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As the International Air Transport Association argues, "Even prior to the COVID-19 crisis, equity owners had not been rewarded adequately for risking their capital," because "average airline returns have rarely been as high as the industry's cost of capital." Using cash flow to pay down debt (adjusted debt fell from $32.9

That's because borrowing costs on new or floating-rate debt go up, making it more expensive to fund acquisitions. This affects short-term earnings, as the rising costs squeeze profits and require a higher return on investment to make acquisitions worthwhile. and is on solid financial footing, with no debt maturing until 2028.

The company's return on invested capital (ROIC), an important metric that measures operational efficiency, has been over 10% for nearly two decades. billion of long-term debt, Emerson's debt-to-equity ratio indicates an exceptionally healthy balance sheet, even if you exclude intangible assets associated with its previous acquisitions.

The best way to ensure you're always a step ahead of Wall Street is to hold shares of quality companies with great prospects for long-term growth. The stock returned 450%, beating the major indexes, as the company grew revenue and earnings at double-digit percentages on an annualized basis.

Investors can set themselves up for success by buying shares of companies with solid long-term prospects that are trading at reasonable valuations and holding on tight. IBM expects to grow revenue by 3% to 5% this year, driven by strong demand for digital-transformation projects that deliver clear returns on investment for customers.

Airlines aren't productive (at least for shareholders) The ultimate test of whether a company is allocating capital productively for shareholders is the comparison between its return on invested capita l (ROIC) and its weighted average cost of capital (WACC).

Given the rapid pace of additive technology evolution for both healthcare and industrial applications, we have great confidence in our longer-term growth prospects. The largest use of cash during the year was $87 million used to repurchase $111 million of debt in March. And I'm thrilled with the prospects.

S&P Global has a robust economic moat When companies borrow money from the public, it's important for prospective investors to understand the company's health, whether it will be able to repay its debts, and the risks associated with investing in that debt. Last year, S&P Global generated $3.9 billion in FCF.

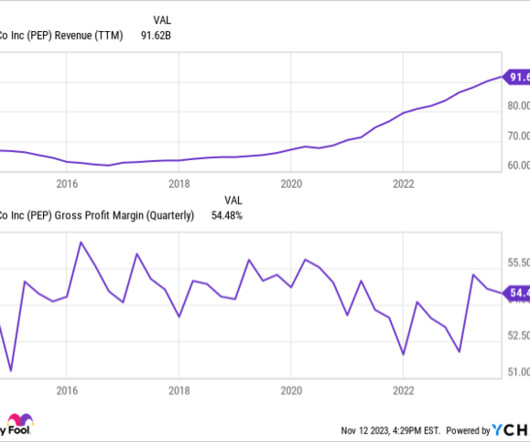

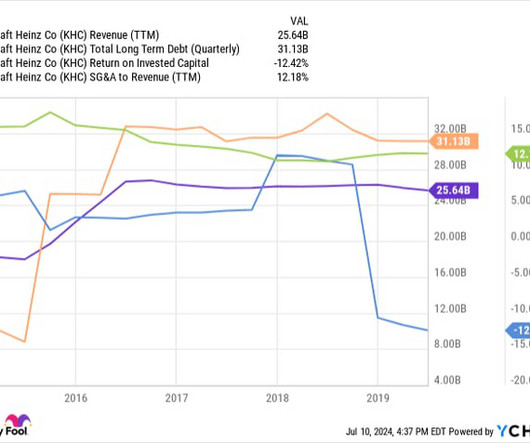

However, blue chip stocks like Kraft Heinz don't lose over half their value by accident; the company has battled through some serious challenges that prospective investors should know about first. The merger dumped tons of debt on the company's balance sheet.

Let's take a closer look at the midstream company's Q2 results, distribution, long-term prospects, and whether now is a good time to buy the stock. Over the past five years, Enterprise has averaged about a 13% return on invested capital, so these growth projects should provide meaningful growth to the company in the years ahead.

Pentair's growth prospects are long-term There are two key reasons to buy water solutions company Pentair. For example, the International Air Transport Association (IATA) estimates the industry will generate a return on invested capital of 5.7% They are more focused on its long-term profit prospects.

With the prospect of lower interest rates ahead, housing stocks are looking up. However, investors were pleased with the overall outlook thanks to low housing inventories and the prospect of interest rates falling later this year. One beneficiary has been D.R. Horton (NYSE: DHI) , which recently saw its shares hit an all-time high.

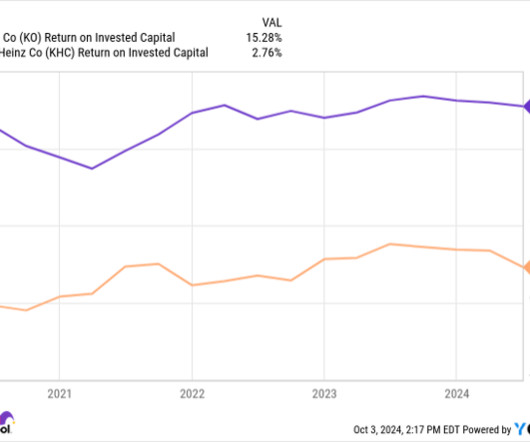

It makes Coca-Cola a more efficient business that generates a far higher return on invested capital (ROIC) than Kraft Heinz: KO Return on Invested Capital data by YCharts A high ROIC can compound for a business over time, leading to more efficient earnings growth and potentially higher investmentreturns.

The world's biggest cruise operator's stock is down by more than 18% since the start of July -- even though it reported positive news in its latest earnings report, such as record bookings and progress on reducing its debt load. This is great news because this free cash flow will help the company attack its debt problem.

Even better, Cava carries no debt on its balance sheet, reducing financial risk. Cava's return on invested capital (ROIC) of 7.4% Another key factor that will get in the way of generating outsized investmentreturns through the rest of the decade and beyond is Cava's current valuation. It's already profitable.

It allows a specific company to outcompete rivals and earn higher returns on invested capital. Does it carry minimal debt? Are there meaningful growth prospects? This is a single competitive advantage, or a combination of them, that has proven to be durable over an extended period. Is the management team skillful?

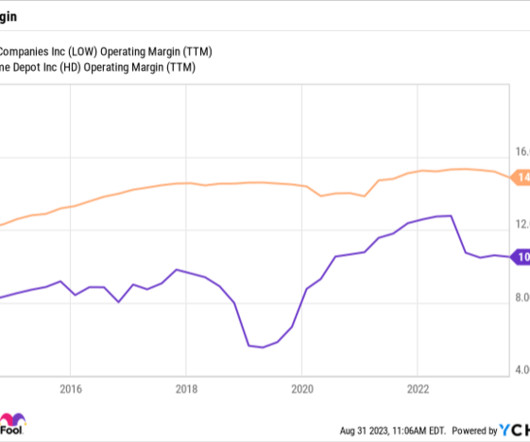

LOW Operating Margin (TTM) data by YCharts Home Depot's return on invested capital (ROIC) also towers above its smaller rival's. Home Depot has a proven track record on this score, including the company's use of low-interest-rate debt to help fund aggressive stock buybacks. Lowe's is aiming for a margin between 13.4%

However, with credit card balances at all-time highs and student loan debt repayments restarting, many customers have been effectively forced to finance their solar systems at today's unsightly rates if they deem the project essential. However, prospecting investors may want to consider the cyclical company as its share price bottoms out.

This is a brilliant way to bring prospective Polaris enthusiasts into the fold and has been proven to double the odds of a customer buying from the company in the future. Polaris Adventures lets customers rent the company's vehicles at over 200 outfitters across North America and explore the surrounding scenery.

The prospect of lower interest rates could accelerate economic growth and help the oil and gas industry, as well as the renewable energy industry. Renewables were hit hard by high interest rates because the cost of capital went up and the return on investment of many projects went down. and a yield of 3.5%.

Or does The Trade Desk possess qualities that make it a good investment over time despite the roller coaster of the past few months? Digging into the factors that drive the company's performance can answer these questions and provide insight into The Trade Desk's long-term prospects. What's more, The Trade Desk's financials are strong.

Various remarks that we may make about the company's future expectations, plans, and prospects constitute forward-looking statements for purposes of the safe harbor provisions under the Private Securities Litigation Reform Act of 1995. billion in cash and short-term investments and $31.3 billion of total debt. in Q4 and 10.5%

A consistently high return on invested capital (ROIC) also offers convincing evidence of ASML's competitive advantage and operational excellence. The company boasts an exceptionally clean balance sheet with a long-term-debt-to-equity ratio of 0.4 and plenty of liquidity, rounding out its impressive set of fundamental ratios.

Recycling capital in this way keeps our portfolio competitive, lower its capital expenses, and accelerates our return on invested capital, driving long-term core FFO growth. Wage growth has outpaced rent growth for the past couple of years, strengthening our resident's financial prospects and improving rent-to-income ratios.

billion in debt and returned $1.6 Interest expense of $206 million in the quarter was up $82 million versus last year primarily reflecting the issuance of $7 billion in debt to fund the NFP acquisition. billion of debt in 2024 and coupled with earnings growth, lowered our debt-to-EBITDA leverage from 4.1

In line with our stated financial strategy, after funding our dividend, Core continued to dedicate free cash to paying down debt. During the third quarter, Core's net debt was reduced by nearly $12 million or 9%. This reduction in our outstanding debt also decreased our leverage ratio to 1.47, down from 1.66 last quarter.

As a result, the new integration will position both of our companies to expand market share, streamline benefits, and drive higher return on investment for joint clients. Only through Zeta's data cloud and CDP can a brand see its existing customers and prospects in one platform. And third, the replacement cycle.

All a stock price tells you is what other investors or prospective investors or soon to be former investors are willing to transact at the moment. They were piling up the cash, tremendously cash generative debt free. Here's our target return on invested capital. That is the market just doesn't care about the prospects.

All of these actions have positioned our company to be in a stronger financial position, with our balance sheet rightsized and our net debt position at the lowest level since becoming a publicly traded company. Debt less cash on hand as of October 31, 2023 was $37.4 Long-term debt as of October 31, 2023 was $40.6

During today's call, Emergent may make projections and other forward-looking statements related to their business, future events, their prospects, or future performance. We have strengthened our balance sheet and will exceed our expectations to reduce our net debt by more than $200 million this year. Turning to Slide 3.

Additionally, we continue to build these direct and long-term relationships with current and prospective customers, thanks to our new podcast, In the Garage by CarParts.com, and our YouTube channel featuring an expanding number of proprietary educational and instructional videos, which to date have received hundreds of thousands of views.

With these last couple of acquisitions, it's starting to speak that same language about cost and opportunity and return on investment. Dylan Lewis: To be clear, the market is rewarding them for that investment today. They're cooling off as a business prospect for these companies, they're still investing.

We generated free cash flow of $2 billion while investing 5.3 Return on invested capital was 13.4%, a 5-point improvement from 2022. As we continue to grow earnings and reduce debt, we will further reduce leverage and advance our balance sheet toward investment-grade metrics. billion of higher-cost debt.

Following the expected close of NFP, free cash flow will be impacted in the near term by deal and integration costs and higher interest expense for transaction-related debt and as we take steps to delever our balance sheet and return metrics to levels consistent with our current credit ratings profile.

During this conference call, management will make forward looking statements based on current expectations and assumptions, including statements regarding our business outlook and prospects, as well as our pending transaction with Teads. We also focus on deploying AI into our internal processes. While we maintain an authorized amount of 6.6

On operating expenses, we need to improve return on investment. For R&D, while innovation requires investment, those investments must be focused, efficient, and offer high return. Today, our R&D investment is spread too thin. Total debt at the end of FY '24 is 4.17 billion and 1.35

We will also offer some perspective on our strengthened balance sheet position with the recent divestiture of one of our noncore businesses, which underscores our focused product strategy and our commitment to driving a strong return on invested capital. Our senior-term debt is now $92.7 We drove a 125% IRR and 9.5

Today's conference call may include forward-looking statements including statements regarding Lennar's business, financial condition, results of operations, cash flows, strategies, and prospects. debt to total capital capitalization ratio, down from 14.2 They truly operate under the banner of One Lennar. We've repaid about 5.6

Customers are excited about this, and as more companies find they're employing a mix of custom-built models along with leveraging existing LLMs, the prospect of these two linchpins services in SageMaker and Bedrock working well together is quite appealing. The top of the stack are the GenAI applications being built.

We have a healthy balance sheet and no debt. This, in combination with our enviable order economics, will enable us to invest in the areas of the business that we believe will drive sustainable, profitable growth in the future. And we'll do that while balancing the necessary investments to drive growth into the future.

Finally, as capital has become more scarce in a higher interest rate environment, companies are exploring partnership opportunities for their embedded infrastructure assets to improve their returns on invested capital or to raise capital to reinvest in their core businesses.

Various remarks that we may make about the company's future expectations, plans and prospects constitute forward-looking statements for purposes of the safe harbor provisions under the Private Securities Litigation Reform Act of 1995. billion in cash and short-term investments, and $35.3 billion of total debt.

As we've noted before, the customer acquisition spend, we invest to drive returns and cash flow has synergy across more than just senior shopping for Medicare Advantage policies. Could you comment on the on the prospects for continued synergies between that business and the senior segment. Just wanted to get your take on that.

The driving force behind Copilot's adoption is the measurable return on investment it offers. Going forward, we will expand Copilot's use beyond prospecting to support key use cases for account executives and account management teams. billion in gross debt.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content