This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Resale company Winmark is a franchisor that owns concepts including Plato's Closet, Play It Again Sports, and Once Upon a Child. Mary Long: I'm Mary Long and that's Brett Heffes CEO of Winmark, a franchiser of resale concepts, including Plato's Closet, Play It Again Sports, and Once Upon a Child. You've got some debt.

The resale company's capital allocation strategy and growth expectations. As I've mentioned earlier, we're Winmark the resale company and our mission is to provide resale for everyone. It's the franchisor of resale brands, including Plato's Closet, Once Upon A Child, and Play It Again Sports.

Dividend-paying companies often demonstrate financial stability and a commitment to shareholder value, making them a reliable choice for long-term investors seeking income and capital appreciation. billion more in cash than debt, Costco emerges as an essential holding for long-term dividend-focused investors.

This is good for the miners because they don't have to sell stock or take on debt to build out their operations. It earns money by offering the cut-price metals it buys for resale at market prices. Wheaton is really a financial partner that gets paid in precious metals, when you step back and look at the big picture.

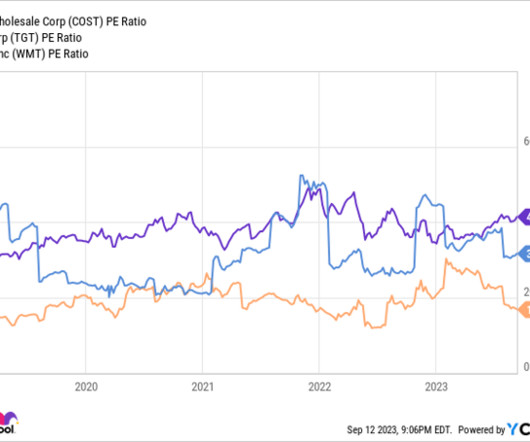

Two excellent examples are home improvement juggernaut The Home Depot (NYSE: HD) and resale goods franchisor Winmark (NASDAQ: WINA). With a 34% return on invested capital (ROIC) , Home Depot generates outsize profitability compared to its debt and equity. But the shareholder returns don't stop here. Image source: Getty Images.

And we returned a record $22 billion in cash to our shareholders, up 45% year on year through dividends, buybacks, and eliminations. Measure on resales, Q4 industrial resales of $173 million declined 27% year on year. billion of gross principal debt. Now, excluding VMware, our revenue grew over 9% organically.

Finally, Q2 industrial resale of $234 million declined 10% year on year. And for fiscal '24, we now expect industrial resale to be down double-digit percentage year on year, compared to our prior guidance for high single-digit decline. billion of cash and 74 billion of gross debt. So, to sum it all up, here's what we are seeing.

Cloud infrastructure and IT outsourcing organic revenue declined 7%, an improvement from double-digit declines we saw in the prior three quarters due to a significant resale transaction delivered in the quarter. Modern Workplace organic revenue declined year to year in the mid-teens impacted by resale revenue, which was down 30%.

homebuilding debt-to-total cap ratio with $6.3 billion plus or minus of net cash flow over the next year, we have the flexibility to invest capital strategically and growth while retiring debt as it matures and repurchasing shares of Lennar stock, which we expect to repurchase at least $2 billion of stock over the next year.

And finally, Q1 industrial resales of $215 million declined 6% year on year. In fiscal '24, we continue to expand industrial resales to be down high single digits year upon year. billion of gross debt. The weighted average coupon rate and years to maturity of our $48 billion in fixed-rate debt is 3.5% years, respectively.

By this, I mean further reducing low-margin resale revenue and driving a higher level of services, including those directly associated with AI and automation. Our results continue to be impacted by the year-to-year decline of resale revenues, which was 90 basis points of the 4.5% Our financial focus is on improving the business mix.

Finally, Q3 industrial resales of $236 million declined 3% year on year, reflecting weak demand in China. And in Q4, though, we expect an improvement with industrial resales up low single-digit percentage year on year, reflecting largely seasonality. billion of gross debt, of which 1.1 We ended the third quarter with 12.1

These tenants allow us to target the biggest piece of the potential homebuyer pool by effectively competing its resale inventory, not just in today's environment that favors builders but also when the resale market returns to historical averages. We issued $575 million in new 1.75% convertible debt due 2028. as of June 30, 2024.

billion, and we returned all of the cash we generated this year to shareholders through repurchases and dividends. We remain focused on enhancing the capital efficiency of all of our operations to produce consistent, sustainable returns and cash flows so that we can return more capital to shareholders through share repurchases and dividends.

As our enhanced operating model gains traction, we believe it positions us well to deliver greater value for our customers, improve financial performance, and drive long-term shareholder value. Non-GAAP net income attributable to DXC shareholders was $2 million year over year. Non-GAAP EPS was $0.74, up 17% from $0.63 Moving to GIS.

Forestar had approximately $800 million of liquidity at quarter end with a net debt to capital ratio of 16.4%. Debt at the end of the quarter totaled $5.9 First, on the resale market, I'm curious some of your thoughts there. 310 million of the finished lots we purchased in the second quarter were from Forestar.

year to year organically and services revenue was down approximately 7% and resale fell approximately 16%. 3Q resale was down approximately 2%, improving from steeper declines in recent quarters, and we continue to be selective on our resale opportunities based on deal economics. The book-to-bill ratio of 1.51 That's helpful.

debt to total capital capitalization ratio, down from 14.2 If we reflect on our second-quarter results, we not only accomplished excellent cash flow and bottom-line results, but we repurchased $208 million of stock and we also repurchased approximately $158 million of senior debt due in fiscal 2024. We've repaid about 5.6

Further, it ensures we sustain our strong margins and generate value for shareholders over a longer period, balancing today's performance with tomorrow's opportunities. billion of debt outstanding, including $863.3 million drawn on our revolver, resulting in a debt-to-capital ratio of 43.6%, and net debt-to-capital ratio of 42.7%.

Forestar had more than $840 million of liquidity at quarter-end with a net debt to capital ratio of 14.9%. Debt at the end of the quarter totaled $5.3 We also have a sizable debt maturity that's very early in fiscal '25 of $500 million in October. Obviously, resale inventory was incredibly tight. billion of cash and $3.1

During the spring selling season with a healthy supply of move-in ready inventory, we were able to capitalize on strong market conditions generated by the increasing need for housing for millennials and Gen Zs as well as the move-down Baby Boomers who continue to find our limited inventory, limited availability of resale housing supply.

As our shareholders know well, we announced Vision 2025 in July of 2022 in response to one of the most abrupt and significant contractions in housing and mortgage volumes in a generation. And obviously, new build has been a really bright spot in the market over the last couple of years versus what we're seeing in resale.

As we previously discussed, two of the largest population cohorts, the millennials and recently Gen Zs are having life events lean to increased levels of need-based housing that currently cannot be met by the constrained resale of home supply in the market. times, reflecting impressive growth in shareholder value. times to 1.4

billion in cash to our shareholders through dividends and stock buybacks. Industrial resales were 962 million. In fiscal '24, we expect industrial resales to be down low single digits year on year. billion of gross debt, of which 1.6 billion, or 49% of revenue. We returned $13.5 We ended the fourth quarter with 14.2

During the first half of the year, we generated roughly $200 million of free cash flow and returned $311 million to shareholders, nearly half of which consisted of share repurchases. That said, the balance sheet remains an important priority, and I will talk about plans for further debt reduction in a few minutes. Thanks a lot.

And lastly, the resale home market remains tight as existing buyers are hesitant to leave their low rate mortgages, which limits available inventory and helps to increase new home demand. We strive to balance growth in the business with returning cash to shareholders. billion and net debt to cap of negative 0.2%

The strong cash generated drove a reduction in net interest expense by about $20 million compared to the fourth quarter of 2022 as we repaid some high variable cost debt during the quarter. Two, how does the M&A market look today, say, relative to returning more cash to shareholders this year? I guess, three very brief questions.

The balance sheets just bulking up over time, 6 billion bucks, rough numbers of retained earnings and super cash flow, no long term debt, working capital, six $7 billion, and they don't have a need for it. Winmark is a resale franchiser of companies like Played Against Sports, Plato's Closet. As a shareholder, I hope so.

billion in long term debt, just $2.5 It certainly seems a little bit more shareholder-friendly, whereas, you know what, Redstone may be pursuing, this is totally understandable, but it seems to be more tilted toward her self-interests or her family's self interests. It's because there's just not that much resale activity.

APA remains committed to returning at least 60% of our free cash flow this calendar year to shareholders. During the first half of the year, we generated $366 million of free cash flow, 94% of which we return to shareholders via dividends and stock buybacks. billion to shareholders via share repurchases and dividends.

Let's first talk about our resale business. Total debt outstanding was $465.8 We will continue to evaluate all opportunities to bolster shareholder value, and we believe this recent repurchase activity is evidence of our conviction in our long term strategy. In total, our U.S. We ended the second quarter with $38.8

We will maintain our disciplined approach to investing capital to enhance the long-term value of our company, including returning capital to our shareholders through both dividends and share repurchases on a consistent basis. Horton and had more than $780 million of liquidity at quarter end, with a net debt to capital ratio of 19.1%.

Our strengthening market position, profitable and growing business, and debt free balance sheet, all enabled our recently announced first-ever share buyback authorization. Last week, we launched our resale platform piloting with our own associates before launching a customer facing experience in the near future.

Total debt, excluding unamortized deferred financing fees and finance leases was $84 million, compared to $101 million at the end of last year's second quarter. And coupled with the recent changes to our credit facility, we believe this will provide additional flexibility as we look to drive future shareholder value.

In the interim term, our expected cash flow generation boosted by our robust new build pipeline, along with normal course debt installment payments are expected to result in significant organic improvement in our net leverage. Turning our attention to the balance sheet and our debt maturity profile on Slide 20.

We've also demonstrated our commitment to returning capital to shareholders. billion to shareholders in the last three years. As we move forward to 2025, we are excited about our opportunity to increase our market share as we compete against new build and resale homes alike. And with that, I'll now turn it over to Phillippe.

billion to shareholders through share repurchases and dividends. Over the past 12 months, we returned essentially all of the cash we generated to shareholders through repurchases and dividends. Four Star had approximately $640 million of liquidity at quarter end with a net debt-to-capital ratio of 29.5%.

Having those shares available in public will help broaden our shareholders base, and a wider range of our shareholders can support us for medium and long-term perspective. The bad debt, for instance, or the residual value losses or the procurement situation, they get confused, so on. And we did have some impact as well at Honda.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content