This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Solid Q1 results Enterprise once again turned in solid results when it reported its first-quarter results, as its total gross operating profit rose 7% to $2.5 Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, rose 6% to nearly $2.5 It generated distributable cash flow of $1.9

Best-in-class profitability In addition to this advantage from monetizing the by-product of its core collections business, Waste Management has historically held higher return on invested capital (ROIC) figures than its two most prominent peers. ROIC shows that it is the best in its industry at reinvesting in its business.

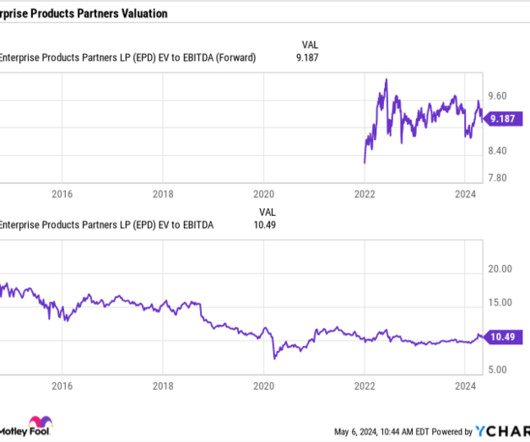

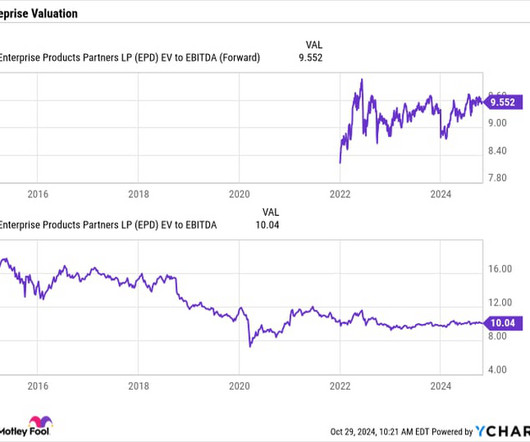

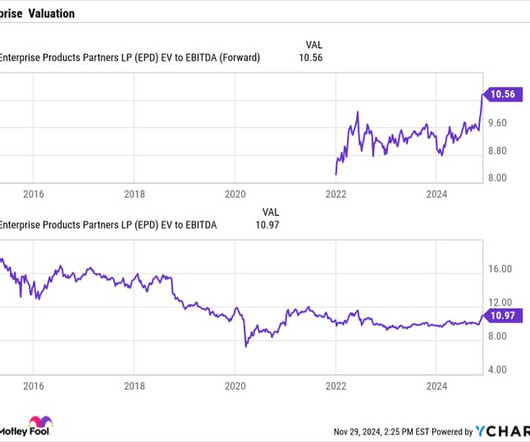

It has averaged a return on invested capital (ROIC) of about 12% over the past decade. Enterprisevalue takes into consideration a stock's net debt, while EBITDA removes non-cash expenses. The company currently plans to spend between $3.25 billion to $3.75

Generating positive free cash flow (FCF) every year since the turn of the century, the stock has delivered total returns of 3,600% over that time -- or seven times the S&P 500 index's return. Compared to its weighted average cost of capital (WACC) of 7%, the company consistently creates value for investors.

From 2014 to 2019, Paycom's annual revenue grew at a compound annual growth rate (CAGR) of 37% while its adjusted earnings before taxes, depreciation, and amortization ( EBITDA ) rose at a CAGR of 64%. At its peak, its enterprisevalue hit $31.9 Image source: Getty Images. Why did the bulls love Paycom?

A consistent performer The key to Enterprise's success over the years has been consistency, which has helped the pipeline company increase its distribution for 26 straight years through various ups and downs in the energy markets. For Q2, the Enterprise saw its total gross-operating margin increase nearly 11% to $2.4

In its third quarter, Enterprise's total gross operating profit increased 5% to $2.45 Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) also rose 5% to nearly $2.44 Enterprise currently has $6.9 It noted that it has produced about a 12% return on invested capital over the past decade.

Since 2018, Enterprise has averaged an approximately 13% return on invested capital (ROIC) on its growth projects. Attractive valuation Despite its strong performance this year, Enterprise's stock still trades at an attractive valuation from a historical perspective. It currently has $6.9

The fourth quarter comes in ahead of plan Earlier this year, Carnival CEO Josh Weinstein unveiled a new three-year plan called SEA Change, which stands for Sustainability, EBITDA per available lower berth day (ALBD), and Adjusted return on invested capital (ROIC). Based on the company's forward guidance, Carnival shares trade at 20.6

Paycom's adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) margin rose from 39.3% Based on those estimates and its enterprisevalue of $2.5 in 2020 to 42.2% in 2022, and it expects that figure to expand to a midpoint of 42.5%

Ricky Mulvey: Well, one thing that Mauboussin has said on some podcasts is that investors have to earn the right to use yardsticks like a price to earnings multiple and enterprisevalue, to EBITDA multiple earnings before interest, taxes, depreciation, and amortization. Compare the price to its return on invested capital.

compounded annually, which will allow us to use our cash flow generation to pay down debt and rebuild the balance sheet as we work toward investment-grade leverage metrics. Essentially, we've pull forward our most important sustainability goal and expect a step change in both profitability and return on invested capital in just three years.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content