This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

ITW Return on Invested Capital data by YCharts. The company has prudently acquired companies over the years (more than two dozen acquisitions), steadily increasing its return on invested capital (ROIC). Illinois Tool Works has an A+ rating from S&P Global , putting it firmly in investment-grade territory.

But we can discuss why the company's immense cash generation ability leaves it positioned to be a winning investment over the next two decades. WM Return on Invested Capital data by YCharts Measuring the company's profitability to its debt and equity, Waste Management's 10.5% Generating $4.4

Given our conservative capital structure and strong liquidity position, we remain very well positioned to continue the growth of our investment portfolio over the next few quarters. We've also continued to produce positive results for our asset management business.

Today, investors have thousands of publicly traded companies and exchange-traded funds to choose from when putting their money to work. Hartford Funds found that publicly traded companies without a dividend generated a modest average annual return of 4.27% over 50 years and were 18% more volatile than the benchmark S&P 500.

And with the federal funds rate on a downward trend, this should be relatively easy for Carnival to pull off. However, one goal may be even more important than all of these : reducing debt. However, the good news is that management can easily kick the can down the road by refinancing the debt. Is Carnival stock a buy?

Generating positive free cash flow (FCF) every year since the turn of the century, the stock has delivered total returns of 3,600% over that time -- or seven times the S&P 500 index's return. is down 40% from its high. Though this $686 million in debt may look alarming, the company maintains a debt-to-adjusted EBITDA ratio of 2.6,

billion, up 14%, with the increase driven primarily by content acquisition costs, followed by depreciation, as well as the impact of the Canadian Digital Services Tax, which was applied retroactively. As you will see in the 10-Q, we have chosen to commit to a new multiyear investment of $5 billion. billion, up 11%.

Top-tier cash generation funds this serial acquirer However, just because Motorola can typically count on its customers to sign new contracts with them every few years, the company doesn't rest on its laurels. Half of Motorola's sales come from recurring revenue tied to the software and services needed across its three product categories.

Depreciation of the quarter was $104.8 million year-over-year improvement, driven by lower depreciation of $7.8 million increase in depreciation for the regulated business. And then, as you know, there'll be differences on things like depreciation no longer occurs. How are those returns moving today as well?

To bring awareness to our innovation and product offerings, our marketing and creative teams ramped up our investments in social influencers, which delivered meaningful engagement and strong growth from new younger consumers. EPS was weighed down by noncash depreciation expenses from infrastructure investments. million or 5.2%

million, producing a core margin of 16.2%, and an annualized return on invested capital of 14.9%. This indicator has a long-lead time, because once the project has been designed, it generally moves to budgeting, funding, and letting phases. million, or 1.63 per diluted share. million related to energy cost rebate programs.

The average daily balance of funds held on behalf of clients was approximately $2.3 Craig just on gross margin, they compressed this quarter at similar levels to what we saw last quarter, even when I take into consideration higher depreciation costs. Turning to the balance sheet. It's fun to do. Kevin McVeigh -- Analyst It's helpful.

First-quarter funds from operations were $1.33 Gains from investment activity in the first quarter were approximately $0.75 Funds from operations from our real estate business was $2.91 And I'll just give you a good example of -- and again, FFO, as you know, is net income plus depreciation. billion or $3.56 OPI had a $0.02

and a trailing 12-month return on invested capital of 10%. This hesitancy is widespread across most segments of the construction markets with the notable exception of publicly funded work, such as infrastructure and institutions. million, excluding depreciation. Including depreciation, costs amounted to $25.3

One important component of this strategy is innovation to solve customers' most pressing needs, aligned with market growth trends, and generate a strong return on investment. independent dealers and distributors take advantage of inventory floor plan financing programs to fund their purchases as customary in our industry.

In line with our stated financial strategy after funding our dividend, Core continued to dedicate free cash to paying down debt. Depreciation and amortization for the quarter was $3.8 The company will remain focused on maximizing free cash and returns on invested capital. million or 10%. last quarter. Christopher S.

Franchise marketing fund revenue of $8.6 Depreciation and amortization expense was $4.2 Marketing fund expenses were $6.4 million, up 10% year over year, driven by increased spending afforded by higher franchise marketing fund revenue. As the number of studios and systemwide sales grow, our marketing fund increases.

In line with our stated financial strategy, after funding our dividend, Core continued to dedicate free cash to paying down debt. Depreciation and amortization for the quarter was $3.7 The company will remain focused on maximizing free cash and returns on invested capital. last quarter. I'll now turn it over to.

And the services segment adjusted gross profit was negative $7 million, which on a cash basis excluding depreciation is approaching breakeven. The more we can do those types of things, obviously, the better return on investment for our shareholders. So, we're going to be focused on it.

For those who don't know what EBITDA is, it's earnings before interest, taxes, depreciation, and amortization, so think of it as earnings before really everything that matters. Now they're selling a lot of AI services that have a good return on investment. A lot of their incentives are tied to that.

Also, over this period, we increased return on invested capital from 8% to 35% and reduced net shares outstanding by over 30%. Finally, AGS continued to produce more than enough operating profit to fund Applied's growing dividend. Next, I'll summarize our growth thesis. Moving to display. Now, I'll share our guidance for Q2.

Returning to our third quarter results, CMC's reported net earnings of 119.4 and a trailing EBITDA return on invested capital of 11.3%. We believe this trend is transitory given the recent CHIPS Act funding allocations and public commitments by sponsors to expand facilities. million, or $1.02

compounded annually, which will allow us to use our cash flow generation to pay down debt and rebuild the balance sheet as we work toward investment-grade leverage metrics. Essentially, we've pull forward our most important sustainability goal and expect a step change in both profitability and return on invested capital in just three years.

Depreciation expense of $188 million was $14 million lower than last year due to reduced technology capital spend. Year-to-date depreciation expense decreased $46 million to $562 million. During the third quarter, we utilized our revolver to fund seasonal working capital build ahead of the holiday season as expected.

While we aggressively pursue growth opportunities, the company will remain focused on its three long-standing, long-term financial tenants, those being to maximize free cash flow, maximize return on invested capital, and returning excess free cash to our shareholders. Depreciation and amortization for the quarter was 3.9

On some assets, we’ve already reduced the value significantly over the past few years (such as shopping centres and offices), so I believe most of the depreciation linked to structural changes is behind us.” per cent return in the first six months of 2023, outpacing the benchmark of 3.2 Over five years, the annualized return was 9.6

Barbara Shecter of the National Post reports Canada Pension Plan investing board posts 1.3% return for year: The Canada Pension Plan Investment Board posted a net return of 1.3 per cent for the fiscal year ended March 31, ending the year with net fund assets of $570 billion compared to $539 billion a year earlier.

As Brian will detail, in 2025, these actions are expected to result in expanded operating margins and an improvement in return on invested capital. Now I will say within that capex plan, we are fully funding Network of the Future. So we're fully funding that, and we're moving forward with it. We will deliver.

These required significant investment and the markets have not seen the growth in profitability we had expected over the past several years. We see an opportunity to shift these resources toward strategic areas that have a higher potential return on investment, and we continue to drive toward our goal. One is product adoption.

Our third-quarter operating income was $273 million, which included depreciation and amortization and accretion of $78 million, round cost of $25 million, production stage expense of $12 million, and share-based compensation expense of $8 million. It sounds like it's not the most efficient path to fund capex in the U.S.

Over the last four quarters, Airbnb has generated a free cash flow margin of more than 40% as it's capitalized on the travel recovery and earns interest on the funds it holds between guest bookings and stays, an additional benefit from its business model. The company also aims to double its return on invested capital (ROIC) to 12% by then.

In such a volatile environment, some investors are also concerned about the company's $75 billion in planned capital expenditures for 2025, which can lead to higher depreciation expenses and lower margins. Investors are also worried about the potential return on investment of the company's AI initiatives.

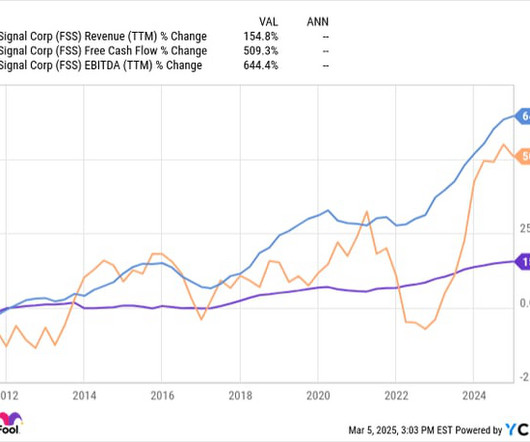

Best yet for investors, Federal Signal has maintained an average return on invested capital (ROIC) of 12% over the last decade. FSS Revenue, EBITDA, FCF (TTM) data by YCharts Powered by this ballooning profitability and cash generation, the company creates ample funding for its M&A ambitions.

In fintech, we upgrade our risk control and optimize payment funding costs, strengthening our overall fintech franchise and profitability. billion renminbi, mainly due to higher staff costs and GPU servers' depreciation related to our AI initiatives. It covers the cost of the GPUs, and therefore, the attendant depreciation.

We're able to make these investments, because of the considerable financial discipline we've exhibited over the past three years as we continually improve multiple areas of the P&L. We hold the high bar and strive to bring intellectual honesty as we evaluate efforts where our investment thesis came to fruition and times that it did not.

It raised guidance for adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) and return on invested capital for the full year. It ballooned when Carnival had no money coming in and needed funds to keep going. It hasn't fully gotten there yet, but it reported positive net income of $1.7

Thus, we are narrowing the focus in our future new store openings to target existing markets and -- in a smaller set of high priority adjacent new markets and that will help us improve new store sales productivity and the return on invested capital. So the other component that's impacting EPS is higher depreciation and amortization.

In line with our stated financial strategy, after funding our dividend, Core continued to dedicate the majority of its free cash to paying down debt. Depreciation and amortization for the quarter was $3.7 Core's team conducted advanced fluid compatibility and core funding experiments in the laboratory. Despite lower U.S.

With respect to share repurchases, we continue to fund buybacks with excess free cash flow while maintaining our leverage goals. We invested nearly $250 million in fiscal 2024 to repurchase about 2.8 million shares, while also paying off our outstanding revolver borrowings and $70 million of term loan.

These drivers will sustain long-term demand as homeowners invest in repairs and upgrades. And we anticipate that some homeowners will begin to tap into record levels of equity in their homes to fund larger renovation projects. times, and we delivered a return on invested capital of 32% for the year.

During the call, Jim, John, and Devina will discuss operating EBITDA, which is income from operations before depreciation and amortization. We prioritize return on invested capital in making these decisions, and we expect all of our investments to provide healthy returns above our cost of capital. times post close.

During the call, Jim, John, and Devina will discuss operating EBITDA, which is income from operations before depreciation and amortization. Our balance sheet remains strong, and we're well positioned to fund the acquisition of Stericycle. Tobey Sommer -- Analyst Thank you. Operator Thank you. Your line is open.

Now in terms of how we are thinking about managing our fleet this year, we have a modest capacity plan of 1% to 2% year-over-year growth, and that growth is fully funded by our efficiency initiatives. As a reminder, the 1% to 2% growth over the next three years does not require additional aircraft as it is funded by efficiency initiatives.

This structure also enables us to seek additional funding options from both strategic and financial partners, which we are now actively beginning to explore. Intel foundry gross margin will improve on EUV mix shift and growth in advanced packaging despite expected depreciation growth in 2025 of roughly 10%.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content