This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Learn More Ares Capital fills a hole left by banks Ares Capital Corporation is a business development corporation (BDC) that provides financing to middle-market companies -- those with earnings before interest, taxes, depreciation, and amortization ( EBITDA ) ranging from $10 million to $250 million.

Fortunately for shareholders, Carvana's management renegotiated some of its debt. This pushed some of its liabilities out, buying it time. Carvana does expect to make a profit of $75 million for Q3 in adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). Can Carvana create shareholder value now?

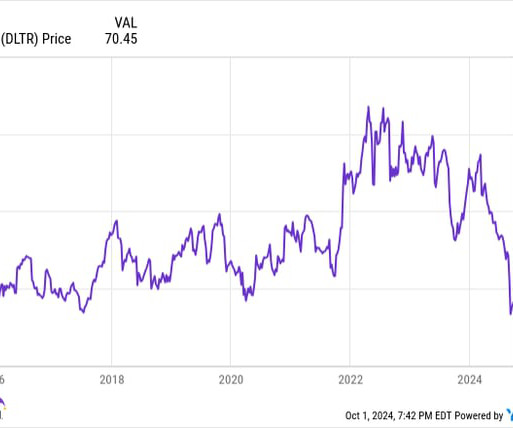

The company blamed rising depreciation expenses, "unfavorable" news on liability claims, the cost of rolling out its new pricing plan, and other factors. Fortunately for its shareholders, Dollar Tree appears ready to rid itself of Family Dollar. Despite that increase, net income fell 13% to $433 million.

In the second quarter, adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) increased by 2.6%, while free cash flow of $4.6 Long plagued by a heavy burden of liabilities, AT&T is managing to deleverage with a decline in net debt supported by positive free cash flow. billion was up $0.4

billion and negative shareholder equity of $217.7 You can calculate it by dividing the company's total debt by shareholder equity. When a company shows a negative D/E ratio, its liabilities exceed its assets -- a sign of potential problems. DOCN shareholders equity (quarterly) data by YCharts.

The increase was attributable to several factors, including lower cultivation and post-harvest costs, higher international sales, reduced inventory provisions, and lower depreciation resulting from impairment charges recorded last year. Included in the efficiency gains was the achievement of 9.1 million in Q4 compared to $3.5

NAV is defined as total assets minus total liabilities and is also reported on a per share basis. We remain confident that these strategies, together with our cost-efficient operating structure, will allow us to continue to deliver superior results for our shareholders in the future. per share.

As noted at our analyst day in late 2023, in our previous earnings call, our story is about the value of long-term strategic decision-making, underpinned by differentiated technology and business model, which endeavors to drive value creation for our shareholders and partners. Net sales in the third quarter were $0.9

And with ROIC ending 2024 at 11%, comfortably above our cost of capital, we are already delivering long-term value for our shareholders as we lay the foundation we'll build upon in 2025 and beyond. Please see our Terms and Conditions for additional details, including our Obligatory Capitalized Disclaimers of Liability. The remaining 2.2-point

Adjusted SG&A expenses increased primarily from ongoing labor investments, higher incentive compensation, unfavorable general liability claim development, and depreciation, partially offset by leverage from additional sales from the extra week. Our adjusted effective tax rate was 23.1%, compared to 23.4%. million, compared to $1.4

Our ultimate goal remains positioning both banners for long-term success and unlocking value for Dollar Tree shareholders. The guideposts of the review remain, as always, to maximize shareholder value through finding the optimal structure for each banner. At the Dollar Tree banner, we're converting stores to our in-line multi-price 3.0

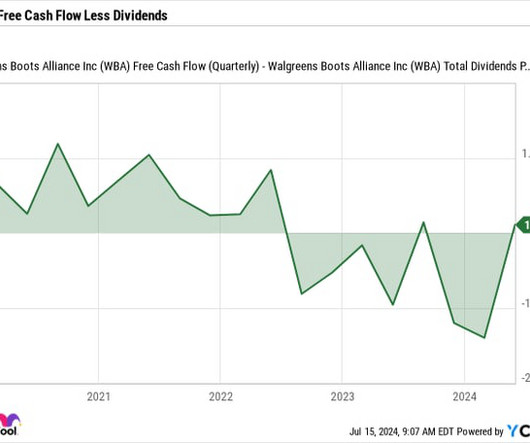

After falling from around $36 per share to reach near $22 in the last 12 months, there may not be much of a reprieve in sight for shareholders of Walgreens Boots Alliance (NASDAQ: WBA). According to an updated price target issued by financial analyst Daniela Bretthauer at HSBC , the stock could fall even further soon, to $20.

Overall, we are proud of the continued progress we're making and are pleased with how it has positioned us to drive profitable sales growth and capture growth opportunities while creating long-term shareholder value. During the quarter, we returned cash to shareholders through a quarterly dividend of $0.59 per share.

NAV is defined as total assets minus total liabilities and is also reported on a per-share basis. for the full year, strong levels of NII per share and DNII per share to fund our record level of annual shareholder dividends, and a new record for NAV per share for the 10th consecutive quarter.

We have a packed agenda lined up for the next three days, and we're excited to see our customers, partners, analysts, shareholders, and employees, all in person to share our passion for BI, AI, bitcoin, and innovation. billion in equity in a manner that we believe to be creative to existing shareholders. Equity issuances.

We further advanced our brewery capacity investments and returned nearly $220 million to shareholders through share repurchases and over 180 million in dividends in Q3. billion to shareholders in dividends and share repurchases through November of 2024, and continue to advance our brewery investments in a disciplined and agile manner.

As I mentioned during our last call, shareholders rightfully expect both short- and long-term results. Excluding live streaming revenue, gains in emerging brands over the past few quarters have largely been offsetting declines from the Evergreen brands as we illustrated in the shareholder letter. Turning to our outlook.

Very few public companies offer monthly dividends, and the ones that do are typically real estate investment trusts (REITs) because they are legally required to pay out 90% of their taxable earnings to shareholders. times its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) over the past few years.

It's normally when a business is doing well and has strong enough financials to support recurring and regular distributions to shareholders that it makes sense for it to pay a dividend. billion are far below the company's current liabilities, which total more than $25 billion, meaning it has a negative working capital.

billion to shareholders via dividends and share repurchases. This is just a start as our goal is to get to 75 days, freeing up cash for our capital deployment priorities, which include returning cash to shareholders. billion to shareholders, $2 billion in dividends, and $1.8 billion to shareholders in 2024.

Excluding Farfetch, net income attributable to Coupang shareholders was approximately $108 million for the quarter and diluted earnings per share was $0.06. So, I think this amortization and depreciation question is a little bit surprising for us. So, this is not an issue of amortization, depreciation reflecting here.

We have a five-year capital plan that addresses replacing key aged and fully depreciated assets in our manufacturing facilities. million, compared to a depreciation and amortization expense of 8.9 That depreciation and amortization expense represents 57% of capital invested. Year to date, we've made capital investments of 15.5

American Tower is a real estate investment trust, or REIT , so it's required to pay out at least 90% of its taxable income to shareholders in the form of dividends each year. American Tower: A leading wireless infrastructure play With a 3.4%

And Energy Income Partners is a pooled investment vehicle that is one of the largest shareholders in Magellan. However, as an "owner" of this energy infrastructure business, a unitholder benefits from things like depreciation. Magellan is an oil and refined products-focused midstream master limited partnership (MLP).

Depreciation expense was $183 million in Q4 and was $743 million for the full year. As compared to last year, depreciation expense declined $4 million and $6 million, respectively, driven by reduced technology capital spend. In 2024, we retired $113 million of funds and returned $222 million to shareholders through the dividends.

On the liabilities side, current liabilities decreased by 56 billion NT, mainly due to the decrease in accounts payable. Next, let me talk about our 2024 capital budget and depreciation. Our depreciation expense is expected to increase close to 30% year over year in 2024, mainly as we ramp up our 3-nanometer technologies.

However, Walt Disney World is still performing well above pre-COVID levels, 21% higher in revenue and 29% higher in operating income compared to fiscal 2019, adjusting for Starcruiser accelerated depreciation. These drivers were partially offset by favorable performance at our Cruise Line and at the Disneyland Resort.

While we were not actively looking to sell the ship, the offer was in the best interest of our shareholders. While charter hire costs increased cruise costs, they are offset by lower depreciation expense. And if it's the right thing to do for the shareholders, then we'll do it. Now, operator, let's open the call for questions.

On the liability side, current liabilities increased by TWD 31 billion, while long-term interest-bearing debt decreased by TWD 38 billion. This change was primarily driven by the reclassification of TWD 42 billion in bonds payable from noncurrent to current liabilities. This is also to maximize the value of our shareholders.

Looking ahead, we plan to deploy RT6, our sixth generation Robotaxi in our Wuhan Apollo Go operation this year which will significantly reduce hardware depreciation costs. In 2023, we made a large purchase which has arrived at different times and the different depreciation start dates. My question is about shareholder return.

With his financial and operational expertise, I'm confident that Adrian will support our growth objectives to create sustainable value for our shareholders. As this will be my last earnings call with Yum China, I want to express my sincere gratitude to Joey, my colleagues and shareholders, and our analysts. billion to shareholders.

As we continue to make progress on our plan, we're even more excited about our future and confident that we have the right strategy to capitalize on the next wave of digital advertising and deliver value for our shareholders. We remain open and we'll continue to consider all opportunities to create further value for shareholders.

NAV is defined as total assets minus total liabilities and is also reported on a per share basis. for the quarter, a new record for NAV per share and NII per share and DNII per share that significantly exceeded the dividends paid to our shareholders. per share or 9%. per share or 9%.

shareholders' returns. Looking ahead, our initiatives to become an even more nimble and data-driven organization are underway, and I'm excited for the shareholder value we will create. I will reiterate that our capital priorities are guided by maximizing shareholder value. With that, Chris, over to you.

billion, up 9%, with the increase primarily driven by content acquisition costs, primarily for YouTube, followed by depreciation due to increasing investments in our technical infrastructure. In Q4, we returned value to shareholders in the form of $15 billion in share repurchases, and $2.4 Other cost of revenue was $25.8

We drove strong wholesale GPU despite experiencing steep depreciation, and we stabilized CAF's net interest margins while we maintained penetration. We achieved this despite experiencing steep depreciation that was concentrated primarily in June and July. Wholesale gross profit per unit was $963, up from $881 a year ago.

Our capital allocation strategy is consistent with our historical framework as we continue to take a disciplined approach to maximizing shareholder value. We also continued to return excess cash to shareholders. Please see our Terms and Conditions for additional details, including our Obligatory Capitalized Disclaimers of Liability.

It's important to note that the hydro business represents an annual EBITDA run rate of approximately $25 million, and we intend to only enter into a transaction if it creates value for our shareholders. Our opportunity is to more effectively standardize and apply best practices to create additional value for our customers and shareholders.

We'd like to welcome all of our shareholders, analysts, and most importantly, our employees to Core Laboratories' second quarter 2024 earnings call. Chris will then give a detailed financial overview and have additional comments regarding shareholder value. Depreciation and amortization for the quarter was $3.8 Christopher S.

We'd like to welcome all of our shareholders, analysts, and most importantly, our employees to Core Laboratories third-quarter 2024 earnings call. Chris will then give a detailed financial overview and have additional comments regarding shareholder value. Depreciation and amortization for the quarter was $3.7 Christopher S.

We continue to significantly reduce capital intensity while returning capital to shareholders. billion to shareholders in FY '25. billion, supporting strong free cash flow and shareholder returns. Those assets are mostly depreciated, but have some useful life left in them and can support our profitable growth strategy.

This came from lower rent and depreciation expenses, as well as more efficient management of marketing and advertising expenses. There's no better investment than investing in our own organic growth while delivering excellent returns to our shareholders. In 2024, we plan to further accelerate return to shareholders to around $1.5

Prismic will enhance our mutually reinforcing business system and drive future growth by leveraging our differentiated brands, global asset and liability origination capabilities, and multichannel distribution. In the fourth quarter, we returned over $700 million of capital to shareholders. Turning to Slide 5.

NAV is defined as total assets minus total liabilities and is reported on a per share basis. Our DNII in the second quarter exceeded the monthly dividends paid to our shareholders by 66% and the total dividends paid to our shareholders by 24%. Our DNII per share for the second quarter exceeded our total dividends paid by $0.22

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content