This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Uber (NYSE: UBER) has taken investors on a wild ride since its IPO on May 9, 2019. But at its current price of about $71 and enterprisevalue of $153 billion, Uber's stock still looks reasonably valued at 31 times forward earnings and 17 times next year's adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ).

in enterprise-value- to- EBITDA (earningsbeforeinterest, taxes, depreciation, and amortization), the most common way to value these stocks. However, the stocks surprisingly trade at a discount today compared to where they traded under the old, unfavorable model.

Cracker Barrel finds its footing Sometimes, investors have such low expectations for a business that anything positive can send its shares soaring. But weighed against investors' low expectations, the company's results looked relatively strong. As of this writing, its enterprisevalue is just $1.4

Lemonade (NYSE: LMND) dazzled investors when it went public nearly three years ago. Investors soured on Lemonade as its growth cooled off, its losses widened, and macroeconomic headwinds rattled the market. Rising interest rates also deflated its frothy valuations. At its peak, Lemonade had an enterprisevalue of $9.8

Buying back more than 55% of its outstanding shares over this time has made the company an unlikely multibagger for buy-and-hold investors. The power of share repurchases Best of all for investors, Murphy's fuel margin has been above $0.30 Should investors buy shares, too? MUSA PE ratio data by YCharts; EV = enterprisevalue.

The donut slinger reported fourth-quarter earnings this week, and investors were clearly left wanting. However, as growth has stalled over the past couple years, investors may want to see how management puts the cyber incident behind it and assess the benefits of the McDonald's partnership before taking a bite of the stock.

billion acquisition, finalized its CEO transition plan, and set long-term financial targets in its investor-day presentation. Management hoped to inspire investors. The transaction has an enterprisevalue of $2.5 The company announced financial results for the fourth quarter of 2024, made a $2.5

Bad news for dividend investors On the surface, it would seem like business is fine for Cracker Barrel. Investors didn't like that, and it's why shares are down. But investors still didn't like it now that it's here. As of this writing, the company has an enterprisevalue (EV) of $1.7 billion, according to YCharts.

Lyft disappointed many early investors, but it's starting to look undervalued relative to its growth potential. With an enterprisevalue of $4.5 Uber, which has an enterprisevalue of $139 billion, is valued at nearly three times next year's sales. Where to invest $1,000 right now? How fast is Lyft growing?

Those AI-driven technologies sound promising, but both stocks disappointed their early investors. Should investors buy either of these out-of-favor stocks as a turnaround play? It cut costs to stabilize its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) and cash flow.

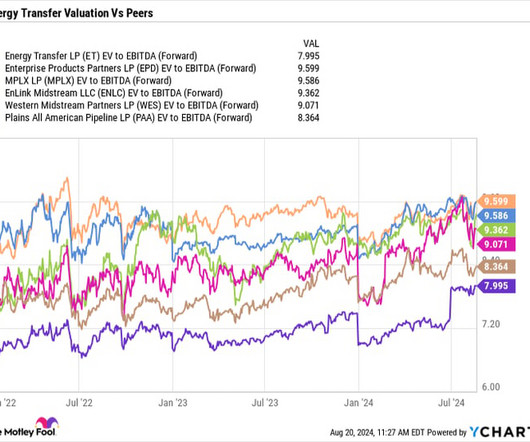

Most investorsinterested in Energy Transfer (NYSE: ET) are attracted to its high yield , which currently sits around 7.9%. This would happen through a combination of growth projects, as well as modest multiple expansion, which is when investors assign a higher valuation metric to a stock. billion in minority interest.

They represent three great value stock options for investors looking for AI exposure. Alongside the other two featured stocks, Johnson Controls trades on an undemanding ratio of enterprisevalue to earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) and is worth picking up on a dip.

Its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) margin also came in at negative 37% in 2023, well below its original forecast of positive 10%. Those numbers disappointed Rocket Lab's investors, even though it signed an additional 17 launch contracts in the first half of 2024.

Warren Buffett famously told investors to "be fearful when others are greedy and to be greedy only when others are fearful." However, investors who buy the right stock as the bulls are heading for the exits can generate some life-changing returns. EBITDA = Earningsbeforeinterest, taxes, depreciation, and amortization.

Income investors will want to plug into this utility Scott Levine (American Electric Power ): Powering past the impressive rises of both the S&P 500 and the Nasdaq Composite, shares of electric utility stock American Electric Power have soared more than 27% since the start of the year. Image source: Getty Images. AEP data by YCharts.

Revenue soared 89% in 2017 and 79% in 2018 before slowing to a 32% clip in 2019. Sensing that it needed a spark to keep wooing growth investors, Teladoc used its rising share price as a way to lock in the equally disruptive health-tech specialist Livongo Health. The transaction was valued at $18.5 billion at the time.

On an adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) basis, it generated a profit of $3.3 Should investors expect smooth sailing over the next three years? They just revealed what they believe are the ten best stocks for investors to buy right now. billion a year earlier.

That's still a near-four bagger gain in less than seven years, but the company lost its luster as its sales growth slowed down, it racked up steep losses, and rising interest rates popped its bubbly valuations. Image source: Getty Images. That 550% gain could turn a $50,000 investment into more than $325,000.

A May filing revealed that Duquesne Family Office had purchased a position in the iShares Russell 2000 ETF (NYSEMKT: IWM) , roughly valued at $700 million right now. Most investors are aware of the S&P 500 -- an index of 500 of some of the largest companies on the stock market. The company isn't profitable yet.

Like many other SPAC-backed companies, Rocket Lab set the bar too high during its pre-merger investor presentation. Rising interest rates exacerbated that pressure by crushing its valuations. Its share count only rose by about 10% over the past three years, so it isn't severely diluting its investors with new stock offerings.

At the same time, a pricey valuation warrants some caution and could be one reason for investors to avoid chasing this caffeine buzz. Earnings per share (EPS) of $0.09 Separately, adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) grew by 120% to a record $52.5 in Q1 2023.

Compared to a challenging last couple of years pressured by disappointing earnings and soft trends from the wireless business, the latest results have presented an improving outlook. Oftentimes into a sharp rally, investors may wonder how much more upside shares can offer or whether it's too late to jump in. billion was up $0.4

The first few months of 2025 have been a rocky ride for investors. While it might feel scary to put your money to work in stocks amid the current environment, smart investors will find opportunities during the current sell-off. Stock prices have become increasingly volatile in recent months amid growing economic uncertainty.

Three such stocks that investors have been feeling bearish about of late are Apple (NASDAQ: AAPL) , Starbucks (NASDAQ: SBUX) , and Prologis (NYSE: PLD). It's trading at 26 times its trailing earnings, which isn't a steep multiple for one of the most valuable stocks in the world. Investors have become concerned about iPhone demand.

That same investment would have withered to roughly $137,000 as the company disappointed its investors with its slowing growth, shrinking moat, and persistent losses. Rising interest rates also squeezed its valuations. That mix of slower sales and rising expenses drove away a lot of Roku's early investors.

Coinbase's revenue soared 514% in 2021 as stimulus checks, social media buzz, and a fear of missing out ( FOMO ) drove more investors into the cryptocurrency market. Coinbase's adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) margin also turned positive again in 2023 as it aggressively cut costs.

Anticipation is building for Block (NYSE: SQ) to report its third-quarter earnings (for the period ended Sept. Despite strong, profitable growth from the financial technology (fintech) leader over the past year, the stock has likely frustrated investors, down 5% in 2024. 30) on Nov.

Celsius (NASDAQ: CELH) and Coca-Cola (NYSE: KO) are both beverage makers, but they attract different types of investors. They also expect its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) to increase at a CAGR of 11% during those three years. With an enterprisevalue of $6.7

times their enterprisevalue -to-rate base and 16.5 times price-to-earnings. The fuel to grow shareholder value Enbridge expects to close the other two gas utility acquisitions from Dominion later this year. The transaction will create North America's largest natural gas utility platform with 7 million customers.

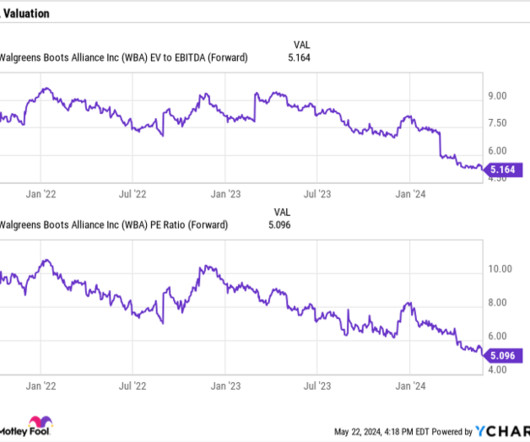

With the stock now trading where it was in 1998, let's look what has gone wrong for the company and whether investors should consider picking up shares in the stock at these levels. At a forward price-to-earnings (P/E) ratio of about 5 and enterprisevalue (EV)- to-EBITDA ratio of 5, Walgreens stock is inexpensive.

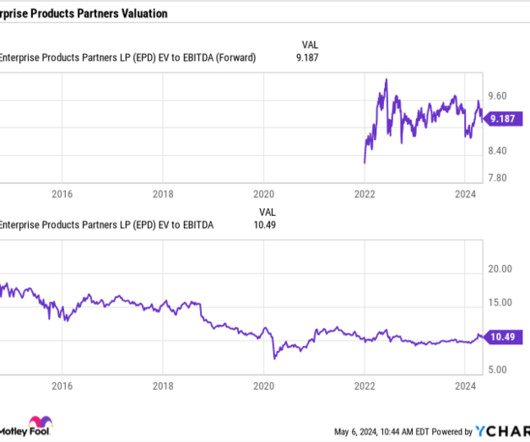

yield, which is an attractive payout for investors looking for income. With its first-quarter results, Enterprise once again showed the steadiness of its business model. However, the company is set to go into growth mode, which should excite investors even more. Enterprise ended the quarter with leverage of 3x.

However, those lower valuations enable investors to lock in a higher income yield, which can make them richer over time. That higher yield would turn every $1,000 invested in the partnership into $43 of annual dividend income, versus $34 for investors in the corporation. They're both publicly traded limited partnerships.

Investors were initially impressed by the gaming platform's rapid growth, and its stock hit an all-time high of $134.72 It lost its luster as it faced tough year-over-year comparisons against its growth spurt during the pandemic, and rising interest rates further compressed its valuations. Image source: Getty Images.

And investors should expect even more dividend increases for years to come. An income stream that can easily beat inflation One of the most attractive factors for Enbridge is that 80% of its earnings are protected against inflation. EBITDA = earningsbeforeinterest, taxes, depreciation, and amortization.

In terms of revenue, Marvell looks a bit cheaper than Broadcom relative to its enterprisevalue ( EV ). But if we look at their projected gains in adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ), Broadcom looks like the better value. FY = fiscal year.

It crashed and burned as rising interest rates rattled the housing market, throttled its growth, and drove investors toward more conservative investments. Nevertheless, Opendoor might be an undervalued growth play for investors who can tune out all the near-term noise. And with an enterprisevalue of $3.27

It appears as though investor optimism is surging, with the Nasdaq Composite index up 35% so far this year. This is exactly the type of rebound that investors wanted after the market tanked in 2022. But investors tend to overreact in the short term and underreact in the long term.

While interest in the metaverse cooled down substantially in the past couple of years, I don't think investors should completely ignore this potentially game-changing technology. A virtual world It's understandable if many investors still can't wrap their heads around what exactly the metaverse is.

Its top investor is the auto giant Volkswagen , which started working with the battery maker more than a decade ago. It also declared its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) would turn positive by 2027. Based on its current enterprisevalue of $2.54

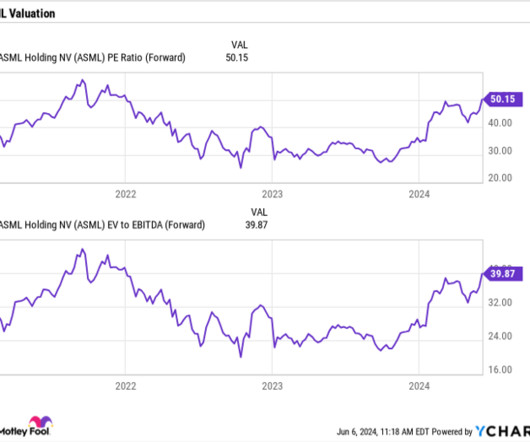

Looking at valuation, ASML stock is not cheap on the surface, trading at a forward price-to-earnings (P/E) multiple of about 50 times and an enterprisevalue (EV) -to- EBITDA multiple of 40 times. Is now a golden opportunity to buy ASML stock? ASML PE Ratio (Forward) data by YCharts. this year to $32.23 billion in 2024.

Bill Ackman is one of the best-known billionaire investors in the world. His hedge fund, Pershing Square Capital, focuses on a few high-quality businesses where Ackman feels the stock has become mispriced, relative to its value. He will then buy shares and use his influence to unlock shareholder value.

Over the next year, the company consistently reported negative adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) until it broke the streak in the third quarter of 2023. At around 50% platform gross margins and ARPU near $40, that's a four-year payback on each user before corporate costs.

As such, the stock remains an excellent choice for commodity investors. Freeport's management estimates its earningsbeforeinterest, taxation, depreciation, and amortization ( EBITDA ) will be $10 billion per annum in 2025/2026 at a copper price of $4 per pound. The company's realized price of copper per pound was $3.85

The three reasons to buy Symbotic Investors should still consider buying Symbotic's stock because it's growing rapidly, its profitability is improving, and its core market is still expanding. Its enterprisevalue of $4 billion, which doesn't include all of those shares, might seem cheap at 2 times this year's sales.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content