This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The leading North American pipeline and utility operator generates very durable cash flow and has very visible growth prospects. Enbridge currently gets 98% of its earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA) from stable cost-of-service or contracted assets. times target range.

The sector has gone through a transformation in the past decade, with midstream companies reducing leverage and being more disciplined when it comes to funding growth projects. Even better, the company has said it could pay excess distributions once its leverage is below 3 times and it has excess free cash flow.

It might have balance sheet issues, lack growth prospects, or have a more complex corporate structure. billion of adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) this year. Many factors can cause a company to trade at a relatively lower valuation. billion to $13.5 times EV to EBITDA.

KMI Financial Debt to EBITDA (TTM) data by YCharts That said, a part of the problem was Kinder Morgan's more aggressive use of leverage than its peers'. Kinder Morgan's leverage is lower today, but it still tends to use more leverage than Enterprise.

It recently added more fuel to its growth engine by making a $2 billion acquisition that will supply it with incremental cash flow while enhancing its growth prospects. The company is paying about 10 times estimated 2024 earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) for these assets.

Analysts expect its revenue to grow at a CAGR of 33% from 2022 to 2025, and for its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) to rise at a CAGR of 54%. It currently serves more than 6,000 customers, including 30% of the Fortune 500, and secures over 300 billion transactions daily.

The table below shows the company's improvements in earnings and cash flow. I've also included its adjusted debt to earningsbeforeinterest, taxation, depreciation, amortization, and rent ( EBITDAR ) multiple. Delta's valuation remains highly attractive Trading on a forward price-to-earnings ratio of just 6.8

billion in adjusted earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA) and $1.2 However, growth prospects haven't improved as the country returns to normal. Sirius XM is also starting to pay down its long-term debt since that bearish leverage peaked in 2022. The model works.

BigBear.ai (NYSE: BBAI) and SoundHound AI (NASDAQ: SOUN) are two small-caps attempting to leverage unique AI-powered applications into long-term growth. The company reported a loss on Q2 adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) of $3.7 Image source: Getty Images. BigBear.ai

But some top consumer-oriented companies quietly delivered market-beating gains and still have bright prospects. Looking ahead to 2024, Carnival expects adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) to reach $5.6 billion, and it expects adjusted net income of $1.2

In fact, management thinks that Carnival will produce adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) of $4 billion (at the midpoint) this fiscal year. Ford battled supply chain issues, rising costs, and rapidly rising interest rates that hurt the company. Revenue of $41.5 were up 66%.

The best way to ensure you're always a step ahead of Wall Street is to hold shares of quality companies with great prospects for long-term growth. The stock returned 450%, beating the major indexes, as the company grew revenue and earnings at double-digit percentages on an annualized basis.

On an adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) basis, it generated a profit of $3.3 That leverage gives Carnival a high debt-to-equity ratio of 4.6. But as its business recovered, it narrowed its net loss to $6.1 billion a year earlier. It ended fiscal 2019 with $9.7

The company claimed it could deliver a compound annual growth rate (CAGR) of 40%, taking revenue from $140 million in 2020 to $388 million in 2023 while expanding its gross margin from 30% to 50% and keeping its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) margins in the high teens.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprise value (EV) -to- EBITDA (earningsbeforeinterest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower. and 7.2%, respectively.

That's exactly when and why you should step into a position in a company with real prospects like Chewy, however. better than 2021's sales, and despite brisk inflation being a problem for the better part of the year, Chewy pumped up 2021's earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA) from $78.5

It has continued to reduce its leverage and now plans to finish the year with a net debt-to-adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) ratio of just 3.9. yield, another factor driving Kinder Morgan is its future earningsprospects.

Approximately 90% of Energy Transfer's 2024 earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) is projected to come from fee-based activities. When Energy Transfer cut its distribution in 2020, it was because its leverage became too high, and it needed to pay down debt.

Revenue increased 27% year over year, and adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) increased 121% to $98 million, driven by increases in non-lending segments. billion with a net interest margin of 37.4%. It added 717,000 new members for a total of 6.9

Upstart bounces back Upstart, which uses an AI-based model to screen prospective lenders to better assess creditworthiness and default risk, has struggled with the high-interest-rate environment like most lending platforms. As of 12:51 p.m. ET, the stock was up 48.6%. Image source: Getty Images.

The company specializes in more complex transactions such as leveraged buyouts , for example. Revenue, EBITDA (earningsbeforeinterest, taxes, depreciation and amortization), and free cash flow saw some dips that resulted in a modest sell-off of the stock. Kinder Morgan: 6.5%

These growth drivers have the MLP on track to increase its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) by 12% at the midpoint of its guidance range this year. Meanwhile, its leverage ratio is trending toward the low end of its 4.0 times target range. per share by 2027.

The company has won over investors excited about its strong financial performance and growth prospects. million in annual sales volume, with an outstanding restaurant-level earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) margin of 26.5% (this figure excludes corporate expenses).

Adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) surged 39% to $180 million. The Trade Desk's prospects in the next few years The Trade Desk executed well over the last few years, growing revenue by 412% from $308 million in 2018 to $1.6 Discovery and Walmart , to its list of partners.

Let's take a closer look at the midstream company's Q2 results, distribution, long-term prospects, and whether now is a good time to buy the stock. Its adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, climbed 10% to nearly $2.4 It ended the quarter with leverage of 3 times.

While this industry has proven to be more cyclical than investors had hoped, its long-term prospects are favorable. In Roku's case, this means it needs to start producing positive earnings sooner rather than later. The company also is benefiting from the rise of digital advertising. This puts Roku in an advantageous position.

This year, management believes Cava will produce adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) of $89 million (at the midpoint), which would be higher than last year's total. Investors need to pay close attention to earnings trends going forward.

While Energy Transfer cut its distribution in half in 2020 to help repair its balance sheet, the distribution is higher today than before the cut. The company's balance sheet is currently in good shape, with leverage (as used by rating agencies) toward the low end of its 4x to 4.5x target range. It plans to spend around $3.1

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017.

Roughly 98% of its earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA) comes from cost-of-service or contracted assets, which are highly stable and predictable. The company also has a strong investment-grade balance sheet backed by a leverage ratio currently in the lower half of its 4.5

Profitability has risen at an even faster pace, showing the operating leverage in the company's business as it gains scale. Adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, soared 80% to $601 million. Gross margins for the quarter came in at 73.8%, a huge jump from 65.5%

But that path can only go so far before growth has to be driven in a different manner, and Kraft Heinz ended up stumbling as it tried to shift gears. Notably, leverage is back to manageable levels, with the company's debt-to-EBITDA ( earningsbeforeinterest, taxes, depreciation, and amortization ) ratio of around 3.6

Just as important as the revenue growth, the company has also seen a lot of operating leverage in its business as well, which is leading to even stronger profitability growth. This led AppLovin's earnings per share (EPS) to more than quadruple from $0.30 Last quarter, gross margins improved to 77.5% from 69.3% from 69.3%

And since the fiscal 2025 second-quarter earnings release on Nov. Let's take a closer look at the cosmetic company's most recent results and prospects to see if now is a good time to buy the stock. Adjusted earnings per share (EPS), meanwhile, fell from $0.82 Sales continue to surge For its fiscal second quarter, ended Sept.

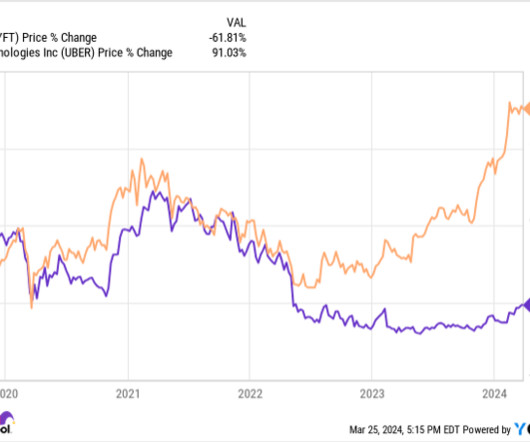

Why Lyft is not (necessarily) the same as Uber To evaluate its turnaround prospects, investors need to understand the differences between Uber and Lyft. And through its larger size, Uber has better leveraged such improvements to its advantage. In contrast, Uber has now turned profitable, earning almost $1.9

billion of adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) last year. Meanwhile, it has a strong investment-grade balance sheet, with its leverage ratio in the lower half of its target range of 4 to 4.5 See the 10 stocks What has fueled Energy Transfer's rally? billion and $15.5

Notably, the second quarter of 2023 marked DraftKings' first quarter of positive adjusted earningsbeforeinterest, taxes, depreciation, and amortization (EBITDA), a milestone that strengthens its standing in the market. This efficiency-oriented approach has been instrumental in driving the company toward profitability.

The company also dramatically improved its adjusted EBITDA (earningsbeforeinterest, taxes, depreciation, and amortization) margin by 14 percentage points to 37% in the quarter. The company is leveraging next-generation AI to give better and more relevant recommendations to users. Pinterest is currently trading at 7.2

billion acquisition, at a 38% premium to the share price before the announcement, with Owens Corning taking on $3 billion in debt financing. Still, suppose you are bullish on the housing market's long-term growth prospects and are willing to tolerate some near-term risk due to its current weakness. The details of the deal: A $3.9

Additionally, the average home in America is nearly 40 years old, so future needs for remodeling should help support Home Depot's long-term business prospects. Additionally, the 73% dividend payout ratio and stellar balance sheet, leveraged at just 1.6 The stock yields 2.8% at its current share price.

It quickly grew in popularity for this cohort of young professionals and university students, and it leveraged that popularity to expand its services, offering the same consumer-centric and easy-to-use digital tools that appeal to its clientele. It's not very expensive at this point, trading at under 4 times trailing-12-month sales.

per share in the most recent quarter and an adjusted earningsbeforeinterest, taxes, depreciation, and amortization ( EBITDA ) of $128 million. Wayfair's business is likely to struggle while the housing market is slow and interest rates are high, but that won't last forever. Earnings per share improved to $0.08

On the earnings call , management expressed optimism for Free Fire as a core "evergreen" franchise that will last a long time. This is because management can leverage local nuances and social media trends and incorporate them into the game itself, constantly refreshing Free Fire and keeping customers coming back.

These advisors leverage their HVAC industry expertise in two critical ways: Theyll have data on other HVAC deals theyve worked on. By working with an advisor who has insider knowledge of past transactions, you can effectively leverage recent deal data to refine your valuation.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content