This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

According to the National Association of Realtors, the median price of a house in the United States is worth $190,000 more than it was a decade ago. If you’ve owned a house for more than 3 years or so, you’re likely sitting on some nice gains. Those gains were not evenly distributed but across the various income levels, homeowners have made a good chunk of change: The pandemic-related housing gains are unlike.

In my role as Mr. Money Mustache, I do my best to be your one-stop-shop for Lifestyle Guru ideas. So over the years we’ve covered not just the Money side of life, but also the even more important stuff like health and fitness and the psychology of better, happier living. But there’s one single area of life where all of these factors come together with an almost Nuclear Fusion level of synergy and effectiveness.

U.S. Bureau of Labor Statistics: The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.1 percent in March on a seasonally-adjusted basis, after increasing 0.4 percent in February. Over the last 12 months, the all items index increased 5.0 percent before seasonal adjustment. ( April 2023 ) As much as I want to jump up and down about 0.1% seasonally adjusted (after a 0.4% prior month), the big number is not so big: 5.0% A 5 handle is a huge development, even with the core remaining sligh

I get a lot of emails and LinkedIn messages about our “funnel” these days. Hiring funnel, sales funnel, etc. Usually it’s coming from well-meaning companies who are focused on recruiting and headhunting or lead generation and prospecting. A typical firm in our industry is probably in need of what they’re offering. I have tried to build an atypical firm.

Your LinkedIn headline is a 120-character “hook” that appears right under your name on your profile and in search results. Similar to a newspaper or magazine headline, yours should be catchy, interesting, and easy to read. Your headline is your opportunity to capture interest and invite users to learn more about you. You may not realize that headlines show up along with your name during an active search, meaning that as I type into the LinkedIn search bar, profiles and their corresponding headli

Last year the Nasdaq Composite was down more than 32%. This year the Nasdaq is up nearly 16%. Last year the S&P 500 was down 18%. This year the S&P 500 is up more than 8%. Last year the Nasdaq experienced 46 down days of 2% or worse, including 18 trading days of down 3% or worse. There were also 40 days with positive returns of 2% or better, including 16 daily gains of 3% or more.

This is Midjourney AI’s imagined version of my new car. I’ll update this picture once I take delivery and head out on my first real camping trip! As I type this, I’m jumping through the various hoops involved in buying a 2023 Tesla Model Y, a spectacularly expensive, large luxury “crossover” that is absolutely loaded to the gills with excess: all wheel drive, faster acceleration than a Lamborghini, enough space for seven people and enough computer gadgetry to function as a small Goog

This is Midjourney AI’s imagined version of my new car. I’ll update this picture once I take delivery and head out on my first real camping trip! As I type this, I’m jumping through the various hoops involved in buying a 2023 Tesla Model Y, a spectacularly expensive, large luxury “crossover” that is absolutely loaded to the gills with excess: all wheel drive, faster acceleration than a Lamborghini, enough space for seven people and enough computer gadgetry to function as a small Goog

Check out these recent headlines about the classic 60/40 investment strategy 1 : The 60-40 Investment Strategy Is Back After Tanking Last Year BlackRock Ditches 60/40 Portfolio in New Regime of High Inflation Why a 60/40 Portfolio Is No Longer Good Enough The 60-40 portfolio is back Sorry, but all of these headlines utterly miss the point. No, the 60/40 mix of stocks and bonds is not dead; No, this is not the first time we had a regime of high inflation, transitory or otherwise.

The prompt: The output, copy-pasted into my blog’s CMS: This is a rainbow stripe! Obviously anyone who knows how to code could have knocked this out in a second without even having to think about it. But how many people don’t know how to code? Most? We’re heading into a future in which not knowing how to do a thing is going to matter much less than ever before.

In this blog post, we will explore the taxation of stock options and provide an overview of how it works. Stock options are a common form of compensation for employees, particularly in startup companies. They give employees the option to purchase company stock at a predetermined price, allowing them to share in the company’s success as its value increases over time.

Can you spot what’s wrong in the image below? Please post your answer as a comment. I think this month’s mistake is pretty easy to spot. I post these challenges to raise awareness of the importance of proofreading. The post MISTAKE MONDAY for April 24: Can YOU spot what’s wrong? appeared first on Susan Weiner Investment Writing.

Whenever there is an extreme move in the economy or markets most people want a simple explanation. We want a single variable to explain what just happened. Interest rates rose because of X. We went into a recession because of Y. Stocks crashed because of Z. But when it comes to something as complicated as the economy or markets, it’s never just one variable.

My fishing pal Sam Rines has spent much of this year pushing a thesis of “ Price over Volume” ; I found it a compelling narrative, one that fits in nicely with an apsect of inflation that I had originally underestimated: “Greedflation.” The Price over Volume thesis is both compelling and underappreciated. I hope you find his take thought provoking… -Barry Price over Volume remains a key theme this earnings season with PG’s earnings report the tip of the iceberg.

I spent the week in Paris with the family and it was really an amazing trip. As you guys know I’m big on history and art and food and stuff so I had been looking forward to it for a long time. And the city did not disappoint. Other than the lack of ice cubes Some shots: The Hall of Mirrors at Versailles, which played host to some amazing moments in the history of the world.

By Matt Pais, MDRT Content Specialist There are many strategies MDRT members use to reach Top of the Table-level production, and some are simply a matter of small adjustments in perspective. George D. Goulet, TEP, CFSB , a 27-year MDRT member from Calgary, Alberta, Canada, recommends these two ways to elevate your practice. 1. Creative positive focus and urgency on a daily basis Benjamin Franklin, a founding father of the United States, is credited with saying, “Early to bed and early to rise ma

USV’s current thesis is: Enabling trusted brands that broaden access to knowledge, capital, and well-being by leveraging networks, platforms, and protocols. [link] That last word is powerful but unfortunately less understood than the other words in that sentence. Protocols have been around forever and are well-understood codes of conduct between people.

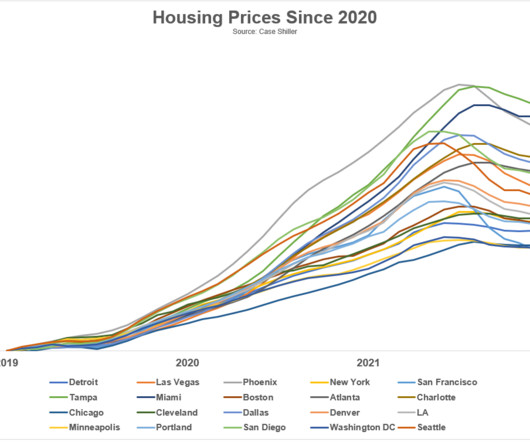

I don’t know if this is my finance brain at work or just hitting middle age but anytime I travel now there invariably comes a point where I pull up home listings in the area on Zillow to get a sense of the local housing market. My family was in Marco Island, FL last week for spring break so of course I had to do some channel checks on housing prices in the area: Two things stand out here: (1) There are tons of list.

I mentioned a few weeks ago how much better Europe ‘s return to office rate was doing versus ours : 90+% RTO, while the USA is ~60%. I cannot speak to Europe, but that U.S. number is an average across all regions, industries, age groups, etc. In some parts of the country, it is appreciably higher or lower; as you might imagine, it varies greatly.

A must-attend event for every RIA owner and practitioner, featuring Michael Kitces, Josh Brown, and Penny Phillips. Register here to secure your spot Michael Kitces is known as every financial advisor’s favorite financial advisor, with Kitces.com serving nearly 3,000 members and his Nerd’s Eye View blog reaching more than 200,000 unique visitors monthly.

By Bryce Sanders Financial advisors need new clients. To do this, they need to keep their prospecting pipeline filled. Financial advisors, coaches and other experts often offer systems for this. It can be confusing, however, to know what to look for in a successful prospecting strategy. Over the years, these are the five criteria I’ve learned to look for: It must be proactive.

A reader asks: I just read Nick’s latest and I’m feeling a bit ashamed. Nick is awesome and Just Keep Buying is my investment motto. I’m 34, my wife is 28 and, not to brag, we make ~$590k a year with a net worth of ~$1.2 million. We max out our 401ks and take the employer match (~$55k / year) and we also save between $20k-$40k, if not more. Our savings rate in my monthly budget is about 24%.

Nonfarm payrolls came out Friday, and once again they impressed with their underlying strength: 236,000 new workers were added in March, with February NFP revised upward to 326,000, as the unemployment rate fell to 3.5%. But there remains nearly two job opening for each unemployed worker, and despite rising wages, lots of decent positions remain unfilled.

And if you haven’t subscribed yet, don’t wait. Check it out below or wherever fine podcasts are played. . The post This Week on TRB appeared first on The Reformed Broker.

When I work with advisors to grow their businesses, we always start with assessing their email list. Email is still the bread and butter of marketing. But if you’re not growing your email list, it’s probably shrinking due to a small number of people unsubscribing each month. Here are my tips for growing your email list, as well as two videos to show how to add people to your email list in both Constant Contact and MailChimp!

A reader asks: I manage my investment portfolio, largely with a very boring mix of three funds: U.S. index fund, international index fund and a total bond fund. Looking at the yield on my bond index fund, it looks like I may be able to get I better yield in a money market fund. Is there any reason to keep my bond allocation where it is rather than moving it into a money market fund?

The consulting firm Global SWF tracks all the important info about Sovereign Wealth Funds (SWFs) and Public Pension Funds (PPFs). Its an amazing collection of charts and data. The asset value peak was $33.6 trillion (USD) in 2021; that’s down only slightly to $31.4 trillion as of the end of 2022. Given the rough year markets had in 2022, including all of the held asset classes, it is an impressive, albeit curious showing.

And if you haven’t subscribed yet, don’t wait. Check it out below or wherever fine podcasts are played. . The post This Week on TRB appeared first on The Reformed Broker.

Some of my advisor clients are incredibly successful on Facebook, and for some it’s a waste of time. What’s the difference? Demographics. Facebook marketing is not for everyone. In fact, our own Facebook business page is not a core focus of our marketing efforts because most of our target prospects are more active on LinkedIn. But for advisors with retired, predominantly female, or younger target audiences, Facebook can be the most cost-effective way to get in front of new prospects (often less

By Antoinette Tuscano While there’s nothing comical for financial advisors about attracting prospects, you can use comic books to capture their attention on social media. A sample from one of the comics Glen Winata uses on Instagram to explain insurance and related concepts. As part of a social media marketing strategy, 10-year MDRT member Glen Alexander Winata , of Jakarta Selatan, Indonesia, hired an illustrator to create several comic books to easily explain insurance and financial products t

The stock market crashed more than 85% from 1929-1932 during The Great Depression. Millions saw their finances get decimated in that period but for most people it was from the economy getting crushed, not their portfolios. Back then the stock market was a place reserved only for the wealthy and bucket shop speculators. In fact, less than 1% of the population was even invested in the stock market heading into the great c.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content