This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

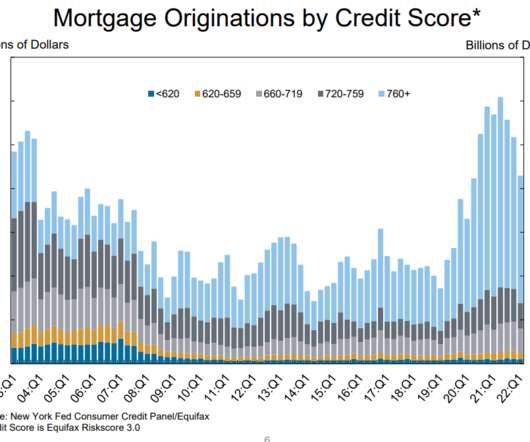

Consumer debt is on the rise. This comes from a recent report by the New York Fed: Total household debt rose $312 billion, or 2 percent, in the second quarter of 2022 to reach $16.15 billion, according to the latest?Quarterly Report on Household Debt and Credit. Mortgage balances—the largest component of household debt—climbed $207 billion and stood at $11.39 trillion as of June 30.

“I constantly remind our employees to be afraid, to wake up every morning terrified. Not of our competition — but of our customers.” -Jeff Bezos, 1998 Amazon shareholder letter. We all know how much FAANMG stocks have faltered this year, but there is a bigger story brewing: The companies themselves seem to have…lost their way. What once made them great has slipped into their historical legacy, with less innovation and far less delight to its end users.

Why did the stock market bounce this summer? Everyone has their explanation: The Fed might pivot! Inflation readings have now peaked! Oil prices are down 25%! China is ending the lockdowns! The labor market is staying strong! Earnings are still coming in better than expected! All true. But there’s an even better reason that doesn’t invalidate any of the ones I’ve posted above.

Tech:NYC is the industry association for NY’s tech sector. They play a number of important roles and one of them is to educate and inform about the impact of the tech sector in NY. To that end, they launched a valuable resource last month called Innovation Indicators. Innovation Indicators is a dashboard that shows the latest data on the impact of the tech sector on the NY economy.

A recurring theme in my articles has been the importance of industry-level economics to the success of an investment; it is not uncommon for all participants in an industry with favorable dynamics to outperform, and, similarly, it is all too common for even the best operators in a poor industry to underperform. However, industry importance is not limited to economics; competitive structure is crucial as well.

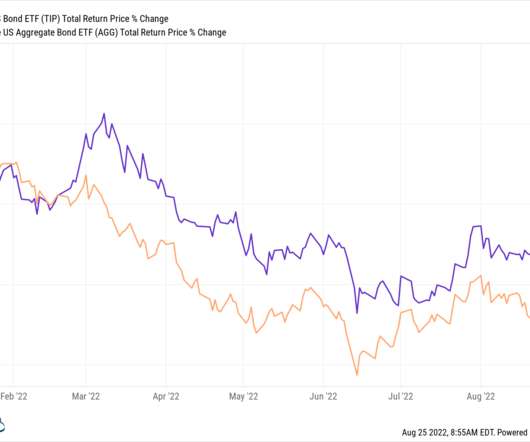

A reader asks: Hey guys please explain why an inflation-linked bond could have lost money this year with inflation at 9%. I’ve been getting this question a lot lately. How could bonds that have an implicit inflation kicker be down almost 7% this year? Treasury inflation-protected securities (TIPS) are one of the most peculiar assets in the investment universe.

Source: AgWeb. If you are interested (as I am) in Real Estate , then allow me to suggest you consider exploring the world of Farmland. It is something I have done for a while, and it is a fascinating rabbit hole to fall into. Not so much as an investor, but as someone interested in how agriculture works (but yes, there is an investor angle here as well).

Source: AgWeb. If you are interested (as I am) in Real Estate , then allow me to suggest you consider exploring the world of Farmland. It is something I have done for a while, and it is a fascinating rabbit hole to fall into. Not so much as an investor, but as someone interested in how agriculture works (but yes, there is an investor angle here as well).

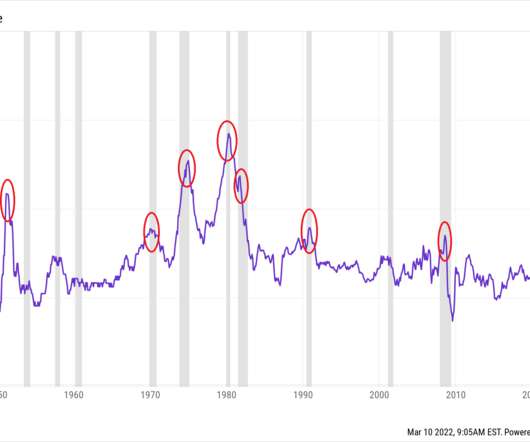

Is this chart going up or down? It’s not a trick question. Just look at it and tell me what primary the trend is. You’d be amazed at how many financial advisors, insurance brokers acting as financial advisors, financial planners, wirehouse wealth managers, financial consultants and other assorted intermediaries in this business could not for the life of them look at this chart and give you a straight answer.

By Antoinette Tuscano You may be a genius financial advisor, but without clients, you won’t be a successful financial advisor. A dynamic marketing strategy is critical to attracting the clients you can best serve. In the following three MDRT videos, you’ll find a variety of ideas to keep your prospecting pipeline flowing and your schedule full: Gain clients through media exposure.

We all know that when it comes to earning interest on your cash, more is better. But not all financial institutions pay the same rate—not even close. Since we launched the Wealthfront Cash Account back in early 2019, many clients have asked us how we manage to offer a rate that’s so much higher than […]. The post Why Is the Wealthfront Cash Account APY So High?

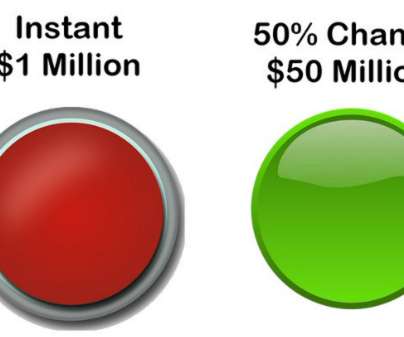

There was a question posed on Twitter this week that caused a stir among finance people: A 50% chance of winning $50 million would equate to an expected value of $25 million. Why would you take $1 million against an expected payout value of $25 million? That doesn’t make any sense. If you understand probabilities, you hit the green button. Easy right?

I had a fascinating conversation with an old friend who has been working in a giant bulge bracket firm his entire multi-decade career. What made this particular conversation so intriguing was his sudden epiphany about the Sell-side. Our previous discussions (debates really) were over the traditional model of brokerage I push back against versus the fee-based fiduciary asset management I embrace.

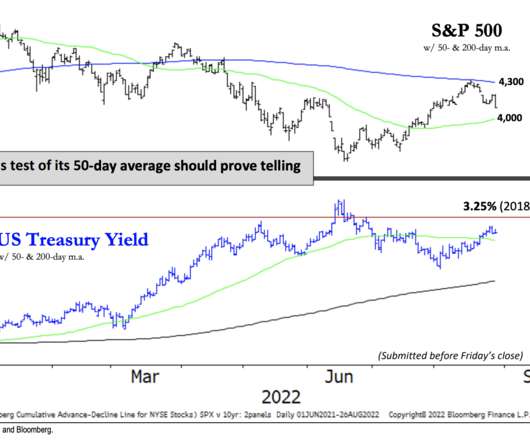

I like the way Ari Wald at Oppenheimer frames the current technical set-up for the S&P 500. Now we’re caught between the declining 200-day and the rising 50-day – the latter might be the next major pivot point for short-term traders and for general sentiment depending on what happens if and when we get there: Here’s Ari: A Bullish Base vs. a Resuming Bear The S&P 500’s rejection from its 200-d.

When fundraising gets tougher for startups, the existing investors (insiders) will often provide a bridge loan to the company to extend the runway for getting another round done. There is more of this sort of thing happening in today’s fundraising market and I thought I’d share some of the things I have learned about setting up bridge loans.

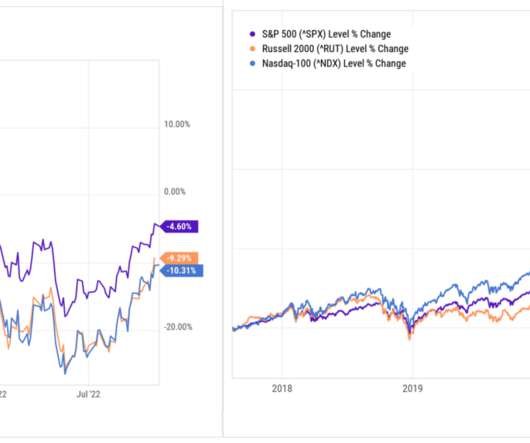

Ryan Detrick shared a stat last week that should put stock market investors at ease with the recent rally: Here is Ryan’s data to back this up: And the chart: This sounds pretty good to me and it makes sense intuitively. Bear market rallies are a common occurrence but not to this degree. So are we out of the woods? Maybe? The problem is that although it appears we have skirted a recession for the time being, it&#.

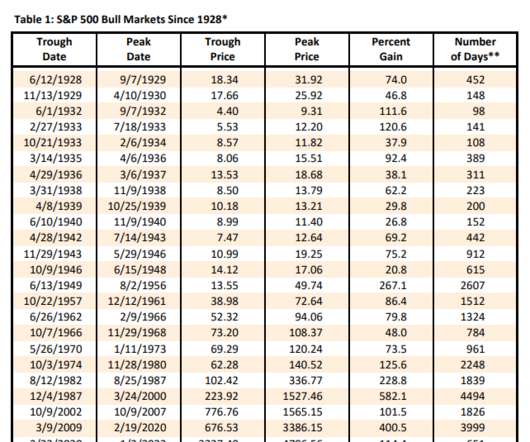

Over the years, I have been involved in a fair share of investment conferences. This began with the Big Picture Conference at the New York Athletic Club, post-GFC. I had flipped bullish in March 2009, but I have vivid recollections that Fall of listening to Jim O’Shaughnessy of OSAM explain the history of markets following a 50+% crash. He was even more bullish than I was, and had the data to back it up.

By Mariam Tinwala As a financial advisor, how you handle objections shows clients how you prioritize their best interests. The following method of objection handling, which is a two-pronged approach of process and then mindset, can help you become a more effective advisor who communicates care and concern for clients. The process. Concerns and objections from the client are expected.

You don’t have to go checking to see all the other performances from last night’s Music Video Awards on MTV, you can just take my word for it – RHCP was the highlight. Nice to see Generation X is still in the conversation <laugh cry emoji>, very quietly being talented and capable while the Boomers and Millennials continue their culture war blood feud.

I don't think any financial advisor wakes up in the morning and intentionally sets out to fail. But I can think of many examples of advisors who unwittingly find ways to sabotage their efforts to build a successful practice. It's often the little things they are either unaware of or don't recognize as problems. But they're big enough to turn prospects and clients away from you.

Historically, financial advisors have relied on word of mouth and cold-calling to generate new leads and grow their business, but consumer preferences have changed. Today’s consumers generally don’t respond well—if at all—to cold calls, and online business reviews have become the new word of mouth.

A reader asks: So I know you guys have talked a lot about are we in a recession now and being in a bear market (equities declining 20%). When is a bear market by definition over? For instance if we just trade flat for the next year and then do enter a recession does this correction still count as part of that? The short answer is, yes, if we don’t reach all-time highs and rollover again at some point in the coming m.

Yesterday I spent some time with Eric Balchunas recording a Masters in Business podcast. Balchunas is Senior ETF Analyst for Bloomberg Intelligence and the author of “ The Bogle Effect: How John Bogle and Vanguard Turned Wall Street Inside Out and Saved Investors Trillions.”. It’s a fun conversation I’m sure everybody will enjoy. There are parts of our discussion I thought were obvious, but he convinced me as underappreciated: First and foremost, the intense disruption of low-c

By Matt Pais, MDRT Content Specialist With seven advisors and six support staff in the office, Carrie Rae Mullins recognizes how essential it is to get some space – away from client meetings, operations questions and more – for strategic planning. So since 2019 the three-year MDRT member from Tigard, Oregon, USA, and her business partner, Sara, have spent two days twice a year at a resort or hotel, utilizing a pre-made agenda and accomplishing as much as possible in their window of time.

Sharing this chart from Guggenheim showing that the S&P 500’s bear market bounce literally stopped on a dime and was turned away at the 200-day moving average. It’s almost too perfect. We manage our tactical portfolio based on technically-oriented rules not because it always works (it doesn’t!) but because it eliminates feelings like fear or fear of missing out from the decision-making process.

Dear Mr. Market: Dividends! Journalists write about you daily. Investors constantly think and talk about you. Analysts and economists spend their entire careers trying to figure you out. You’re a complex yet simple character, Mr. Market! All that said, today we want to share with our readers a substantial part of you that doesn’t get enough appreciation (pun intended).

There were a lot of predictions at the outset of the pandemic about how the world would be changed forever. Some were kind of right. Others were very wrong. So it goes with these things. The one that never made sense to me is how colleges were going to get disrupted by online classes once students saw how pointless it was to go to class. If anything, the pandemic proved how necessary it is for young people to interact wit.

One of my favorite ways to contextualize market trends is to divide long periods of time into secular bull and bear markets. When we look at the past century, we can see decades-long eras where the economy is generally robust, supporting markets trending higher, with expanding multiples. We call these eras Secular Bull Markets. The best examples are 1946-66, 1982-2000, and 2013 forward.

By Xiao Chen, CFP This is one of the major decisions I had to make during my business career. When I started in the financial services profession, I was with a mentor, and she was a very warm person. She taught me a lot — everything that I needed to know to get started. But later on, as I took on more of a management role within the company, there were some fundamental philosophical differences on in how we run our businesses.

And if you haven’t subscribed yet, don’t wait. Check it out below or wherever fine podcasts are played. These were the most read posts on the site this week, in case you missed it: The post This Week on TRB appeared first on The Reformed Broker.

Did you know that “OK,” not “okay” is the correct spelling of that familiar expression? If you didn’t know how to spell OK, you have plenty of company, as I discovered when I ran a LinkedIn poll. Origins of OK. The term OK is an initialism. It comes from the misspelling “oll korrect” for “all correct.” Apparently such misspellings were popular in the 1830s, when this term originated, according to “ The Hilarious History of ‘OK’: The English language’s most successful export is a jok

A reader asks: For all these new home buyers who bought at massive house prices due to ultra-low rates…will they then get screwed when house prices normalize with ~6% rates being the norm? So like when they sell their home to move, they may be selling at a loss? Is this not a bubble waiting to pop? This is always a possibility. There was a massive pull forward in housing returns these past couple of years.

When it comes to integrating data with investing insights, no one is better than Ben Carlson. I direct you to today’s “ Exceptions to the Rule, ” where Ben dives into the nitty gritty of the conflicting data between market action and inflation data: BULL : The S&P 500 has recovered half of its 2022 bear market losses. When this has occurred in the past, stocks have never moved back to new lows, and have been higher every time a year later.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content