This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A reader asks: As a long term investor (10-20 year horizon) is it worth selling portions of a stock when it’s up and taking some profits, maybe reinvesting when the price goes down or pocketing the money? Or, is it best to stay “all in” regardless of the ups and downs? There are two different ways to think about this question. One is the Charlie Munger approach.

After yesterday’s discussion on the uncertainty monster , a friend who “loves perspective changers” reached out with a challenge: “Most people rarely question their own basic ideas,” he said, He challenged me to find 10 concepts to do just that. I agreed to give it a shot, assembling a list of my own, filling it out with a few classics from others: Uncertainty : Objectively speaking “uncertainty” does not increase or decrease – by definition, the future is always inherently uncertain.

Typically, investors don’t take a board seat until you raise your first equity round—which means that it could be *years* before you have a real board meeting: A year of nights/weekends work researching, prototyping, and fundraising. You raise your pre-seed round and if you're lucky and good, you can get to an equity round in 12-18 months. Many people extend this round and don’t get there for two years.

By Bryce Sanders Financial advisors are trained to ask clients for referrals, and so from time to time we ask, “Do you know anyone I can help?” Put on the spot, though, sometimes our clients’ minds go blank. Yet, happy clients can be your best advocates. How can we do a better job at asking for referrals? Who wants an extra slice of pie? Your client asked about a specific product.

Put this phrase in your vocabulary for the second half of the year because you are going to be hearing it everywhere: “a mild recession.” This is where the puck is going. All of Wall Street’s chief strategists and chief economists are going to be pivoting to this case if they haven’t already. The “soft landing” idea is going to fade away.

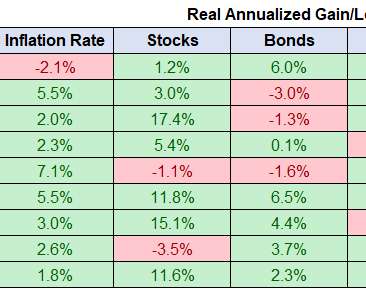

A reader asks: Many right now are saying real estate is the only way to get a real return in a safe manner. Will you post some data on real estate vs. bonds vs. stocks? You always have to be careful when you use the word “safe” when it comes to investing. An investment that feels safe now could be very risky in the future and vice versa.

For the first half of this year, I have steadfastly refused to join Club Recessionista. I have not believed we were already in a recession, and I was hopeful that a moderate Fed gradually raising rates to throttle inflation could execute that soft landing. No longer. As I mentioned to Tom Keene last week, Nick Timiraos in the Wall Street Journal revealed the Fed’s intention to raise rates 75 basis points brought a reckoning to my hopes of a non-recessionary growth slow down.

As strange as it may sound, earning financial freedom is a lot easier for certain people than claiming that freedom once they have earned it. And if the following statement rings true to you, you may be suffering from this same hardship: “I think I’m close to having enough money to jump into early retirement, but not quite. So I’m just working one more year and starting one more side hustle and buckling down extra hard to be more certain.”.

By Bryce Sanders Do you remember your first day of school when you were surrounded by new faces and how overwhelming that felt? Eventually, you made friends and felt more comfortable. Now let’s fast forward to today — you’re a successful financial advisor who’s involved in the community and attending social events. It could be a wedding, an art gallery opening night or a fundraiser.

It’s been an honor and a pleasure writing, recording and filming for you guys all year. 2022 has been incredibly challenging as an investor, a financial advisor, an investment advisory CEO and a professional market commentator. Tough all around. Like everyone else, I’ve gotten some stuff right and some stuff wrong this year. Based on this week’s reaction to large cap technology company earnings and the F.

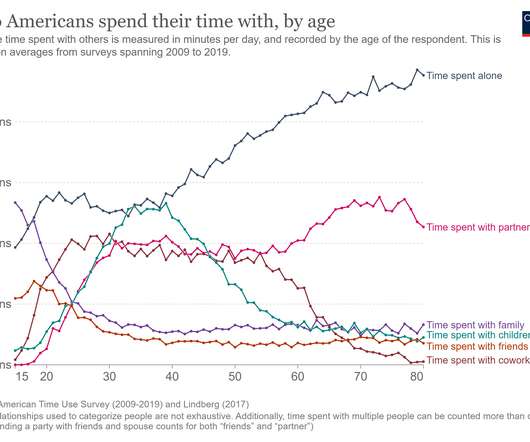

Derek Thompson posted this incredible chart from Our World in Data on who Americans spend their time with, by age: These are average numbers but based on this chart the time spent with: Your family peaks at around 15 years old. Your friends peaks at around 18 years old. Your co-workers peaks at around 30 years old. Your kids peaks at around 40 years old.

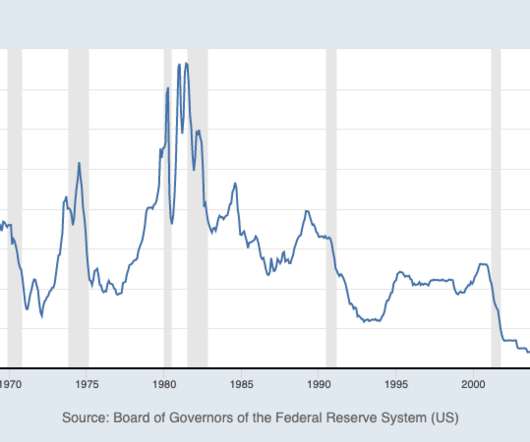

Today is Fed day, when we get the 75 bps increase that dramatically increases the odds of a recession. The main storyline is inflation, but the overlooked subplot here is Wages. I have detailed over the past decade or so the lagging nature of wages in America — deflationary in economic terms — and how that had begun to change in the late 2010s pre-pandemic.

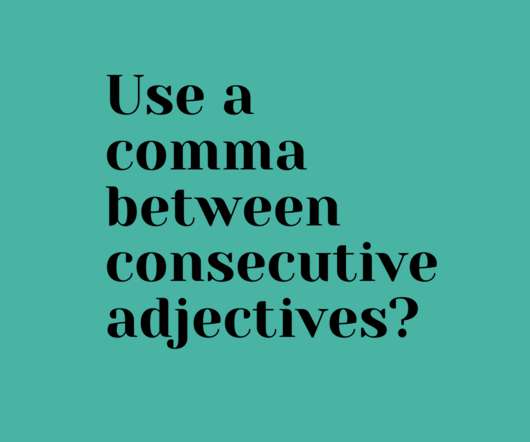

When two consecutive adjectives modify the same noun, you’re supposed to put a comma between them. I sometimes struggle to decide if that’s appropriate. After all, there are cases when the first adjective modifies the second, as in “pale blue paper.” So I was delighted to find this advice from Jan Venolia in Write Right! : One way to determine consecutive whether adjectives modify the same noun ( a young, energetic student ) is to insert the word and between the adjectives.

And if you haven’t subscribed yet, don’t wait. Check it out below or wherever fine podcasts are played. These were the most read posts on the site this week, in case you missed it: The post This Week on TRB appeared first on The Reformed Broker.

Three random thoughts on the current state of the stock market: (1) The top 10 stocks are getting smoked. One of the prevailing theories during this past bull market is the biggest stocks were carrying the S&P 500. The top 10 stocks now make up more than 30% of the index by market cap so it would make sense for this group to have an outsized impact on the performance of the market.

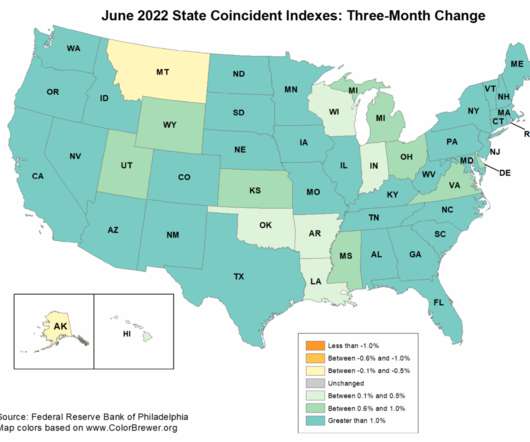

The last time we looked at the State Coincident Indicators Index, all 50 States were in an economic expansion over the trailing 3 months. The diffusion index = 100. That is no longer the case today. The FOMC meeting on May 3-4 raised rates by 50 basis points, which was followed by the 75 basis point increase at the June 14-15 FOMC meeting. Taking rates to the 1.50%-1.75% range had some bite, and we see the impact of this higher cost of credit combined with inflation impacting the economy.

What should you focus on if we face a recession? How should your financial plan be revised over time? Find out on today’s show. Experts on divided on whether or not we are headed for a recession (or are already in one). Financial uncertainty in the market is giving a lot of people a lot of anxiety. How does Brian help his clients cope with this? You’ve got to focus more on your particular situation as opposed to the big picture of the country, the economy, or whatever because you can’t do anythi

In many large businesses, it’s common for employees to own stock in the company. Anyone who owns company stock will eventually have to decide how to distribute their assets — typically when there is a job change or retirement involved. When you are presented with the option to distribute your assets, you will have the choice to roll them into an IRA or place the stock into a taxable account and then roll the remaining assets into an IRA or 401(k).

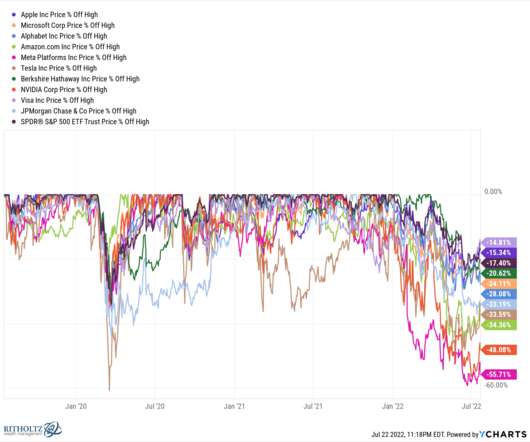

As of the close of the trading day on June 16, 2022, the S&P 500 was down 23% from its all-time highs: The Russell 2000 Index of small cap stocks and the Nasdaq 100 were both down nearly 32% and 33%, respectively, from their highs. That’s a pretty decent bear market. Since that day, the S&P 500 is up 13%. The Russell 2000 has shot up 14% while the Nasdaq 100 has bounced 16%.

?. This week, we speak with Bloomberg Businessweek staff writer Hannah Elliott , who reports on the automotive industry with a special focus on hyper-cars, motorcycles, and electric and luxury vehicles. She lives in Los Angeles, where car culture is enjoying a renaissance. NOTE : During the broadcast portion, we had the usual Q&A but in the podcast portion, this turned into a conversation; Hannah made the mistake of asking me a question and we were off to the races of me babbling about cars

What are the risks of making emotional decisions when it comes to your money? Brian shares what he tells clients about investing and retirement planning. During the football draft, so many decisions are based on emotions. For instance, Tom Brady, the greatest of all time, was 199 th pick when he was drafted in 2000. Similarly, investors who want to plan their own retirement might pick stocks based on emotions that they later regret.

If you haven't already, it's essential to take the time to familiarize yourself with the latest Social Security Trustees report. The solvency issues are a significant concern for people on the cusp of retirement today since the depletion date outlined in the report, 2034, is well within their life expectancy. As you're discussing Social Security benefits and how they fit in the context of the retirement strategy , it's important to note that the Social Security trust fund is scheduled to run out

Frank Rabinovich was a portfolio manager and technology specialist at bond giant PIMCO in the 1990s. The way his colleagues treated him was a microcosm of the culture at the firm in its heyday. Co-workers would douse him with bug spray, claiming he smelled bad. They cut off the bottom of his ties when they didn’t like the look of them. They tackled him relentlessly in games of touch football since he wasn’t as.

This week, we speak with Graham Weaver, who is the founder and CEO of Alpine Investors, a private equity firm in San Francisco that invests in software and services. Graham has been in private equity for over 20 years, having started Alpine in his dorm room at the Stanford Graduate School of Business. We discuss how he launched a PE company in his dorm at Stanford’s GSB, and proceeded to “make every mistake in the book.” But his investors stayed with him, impressed by his commu

Category: Compliance. The Significance Of Financial Compliance Financial compliance requires all actions, procedures, guidelines, and business culture to abide by the rules and regulations set by the regulatory authorities of the financial market. For example, the Securities and Exchange Commission (SEC) in the United States or The Financial Consumer Agency of Canada (FCAC) in Canada.

By Cynthia Nallely Rodriguez Barbosa For some of the people you’re calling, you’re creating a negative experience. It’s not personal. A telecommunications company surveyed thousands of young people and found that 81% of respondents feel anxious about making or receiving a phone call. Why? They consider it a waste of time. They do not like to do favors, and many times when someone calls, it’s to ask for something.

A reader asks: I’ve been buying the dip for the past couple of months in the market and feel pretty comfortable in my positions. Should I continue to buy the dip or invest in my home (ie, new fence, additional rooms/bathroom, etc.? I understand the line of thinking here but I look at the stock market and investing in your home as two separate categories when it comes to capital allocation decisions.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content