This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Three thoughts on the trade-offs involved in the economy, markets and life: 1. There is no such thing as a perfect economy. This was the general environment for the 2010s: Low GDP growth Low inflation Stagnating wages A slow labor market High(ish) unemployment rate 0% interest rates A booming stock market This is the post-pandemic 2020s (so far): Higher GDP growth Higher wage growth Higher inflation A booming labor mar.

Click to download Financial Disasters Yesterday was kind of a fun day: Sure, it was a dark, damp, dreary February morn when I showed up at the Brooklyn Bridge Marriot, but it was also the first time I did a new presentation in front of a live audience since before the pandemic. I do a quarterly update for RWM clients that covers the economy, the markets, and our portfolios every three months.

A reader asks: I am in my mid-40s and have been running my own RRSP (Canadian 401k) for a while now. I have almost no exposure to bonds. I ran it by an advisor and her reply was why would you want bonds? They had been paying next to nothing for years. They don’t seem to even go up when stocks are going down. I can see her point. Instead of bonds I have been buying ETFs with a covered call component for what would be the.

Very useful dashboard via the St. Louis Fed, which maintains the fabulous FRED database. With a clean and simple interface, it puts all of the key economic indicators the FOMC tracks — Real GDP Growth, Unemployment Rate, PCE Inflation, Core PCE Inflation, and the Federal Funds Rate — in one convenient location. The Macro Snapshot also dives deeper into three core aspects of the economy: 1.

By Matt Pais, MDRT Content Specialist With all the work advisors do for their clients’ financial health, it can be easy to overlook their own needs. This includes MDRT Past President Brian D. Heckert, CLU, ChFC , a 35-year member from Nashville, Illinois. Earlier in his career, thanks to his professional success, he accumulated other businesses including a car wash and multiple shoe stores.

By Matt Pais, MDRT Content Specialist With all the work advisors do for their clients’ financial health, it can be easy to overlook their own needs. This includes MDRT Past President Brian D. Heckert, CLU, ChFC , a 35-year member from Nashville, Illinois. Earlier in his career, thanks to his professional success, he accumulated other businesses including a car wash and multiple shoe stores.

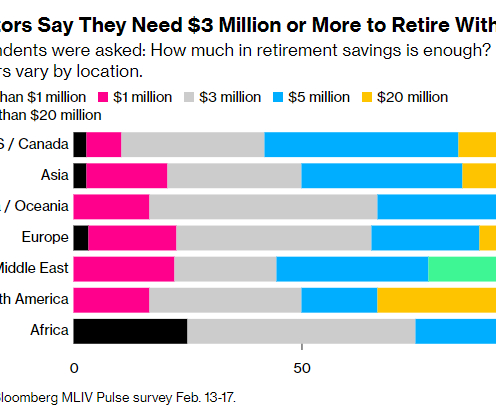

Bloomberg asked investors from around the globe one of the most important questions in all of personal finance: How much is enough to retire comfortably? The results were a tad on the high side: The average number came in somewhere between $3 million and $5 million. One-third of respondents said $3 million while another third said it was closer to $5 million.

My end-of-week morning train WFH reads: • The Fed alone cannot bring inflation down : Management of demand is not efficient in dealing with supply-driven price rises: fiscal policy must play its part.art ( Financial Times ) • When a savings account is very risky : Compound Banc pays an eye-popping 7% on deposits — or at least things that look and feel a lot like deposits.

By David Trusler, MBA I believe you achieve true happiness and prosperity by serving others with honesty and sincerity. I believe true success is measured by the lives we impact and the communities we serve, not just by the amount of premiums we collect in a year. So, what keeps you motivated? Is this motivation enough to keep you going during difficult times?

We bought our first home in late 2007. Our rate at the time for a 30 year fixed was something like 6.25% or 6.5%. It didn’t seem high at the time but then again we didn’t have 3% rates in the rearview mirror to compare it to. Housing prices were obviously a lot lower back then as well (and going even lower for a few more years after that).

This week, we speak with Tim Buckley , who is chairman and chief executive officer of Vanguard. Buckley has been with Vanguard for 32 years and has been CEO for the past 5. Previously, he was chief investment officer and chief information officer, overseeing the company’s internally managed stock, bond, and money market portfolios as well as its investment research and methodology.

Today’s Talk Your Book is brought to you by Jensen Investment Management: We had Kevin Walkush, Portfolio Manager at Jensen Investment Management on the show to discuss investing in quality businesses. On today’s show, we discuss: Jensens quality thesis What Return on Equity is Sector dynamics within the quality factor Discounted cash flow assumptions How to react when the facts change Forward-looking funds vs backw.

Transcript: Tim Buckley, Vanguard’s CEO The transcript from this week’s, MiB: Tim Buckley, Vanguard’s CEO , is below. You can stream and download our full conversation, including any podcast extras, on iTunes , Spotify , Stitcher , Google , YouTube , and Bloomberg. All of our earlier podcasts on your favorite pod hosts can be found here. ~~~ ANNOUNCER: This is Masters in Business with Barry Ritholtz on Bloomberg Radio.

By Bryce Sanders Have you ever heard a client say, “I never knew you did that! You never told me!” I have. Years ago, when I was a financial advisor at my former firm, the company got into the mortgage business. Advisors would receive notifications when clients applied for a mortgage elsewhere and their in-house assets needed to be verified. The advisor would comply, then call the client and say, “We do mortgages.

The weekend is here! Pour yourself a mug of Colombia Tolima Los Brasiles Peaberry Organic coffee, grab a seat outside, and get ready for our longer-form weekend reads: • How a shipping error 100 years ago launched the $30 billion chicken industry : The accidental origins of the chicken on your plate, explained. ( Vox ) • A twisted tale of celebrity promotion, opaque transactions and allegations of racist tropes : January 2022 was a time capsule showing the temporary alliance between celebrity ma

If you’ve been with Indigo for a while, you may have noticed our logo update and website refresh. We may have a new look, but we are still offering the same great custom content solutions and personalized marketing strategies. In fact, we have even taken this time to expand our services into branding refreshes, logo designs, and updated website copy.

We celebrate many different major life events as we get older—birthdays, weddings, or the birth of children. Something you may want to celebrate is the end of your working years. Now that you’ve worked to set up a great life after working for so long, it can be a great idea to help avoid those retirement blues and start your retirement off with a bang!

As a financial advisor, you know that taxes in retirement are one of your clients’ top stressors. Offering planning services that optimize your client’s tax situation is an excellent way to highlight your expertise — and it makes a compelling selling point for potential clients who are concerned about navigating the tax aspects of their retirement income planning.

8 MIN READ There are a million things to keep track of when running a business. There are customers and employees, marketing and keeping an eye on industry trends, cash flow and compliance. With these come a number of different dates to keep track of, which as a small business owner or a solopreneur can get overwhelming, fast. It’s easy to prioritize items that are more enjoyable than others (prospect lunch or update ADV … hmmm), or those that have an immediate impact on our day-to-day operation

The concept of retirement planning is simple. Despite changes in the economy or in life itself, the concept of planning your retirement has remained unchanged. We work, save, retire, and repeat for generations over. But while the concept may be the same, the puzzle has begun to evolve. In other words, individuals and families currently saving for retirement are facing challenges that were previously never considered.

When a new technology comes to market, we often look for “native” applications of that technology. What is a “native” AI application? What is a “native” Web3 application? I have not seen a better articulation of “native” than my partner Albert’s post from 2009 on native mobile applications. He started out by laying out the new primitives that mobile smartphones made available to developers.

One of the biggest stories in the markets so far this year is the $100 billion in lost market cap ripped out of Alphabet’s stock when it became apparent that the search giant was going to be under siege by Microsoft’s push into AI. How did such a successful, innovative business like this suddenly find itself in this position? Maybe it wasn’t so sudden.

Sonali Basak interviews AQR Capital Management’s Cliff Asness. They discuss AQR’s 60/40 portfolio strategy and the risks facing financial markets, with Sonali Basak and Guy Johnson on “Bloomberg Markets.” AQR’s Cliff Asness on 60/40 Strategy, Market Risks Source: Bloomberg , February 23, 2023 The post Asness on Value Investing & Humility appeared first on The Big Picture.

How much can I contribute to my 401(k) in 2023? If you are under the age of 50, the maximum amount you can contribute (called an elective deferral) to your employer sponsored 401(k) plan is $22,500. This is an increase from the $20,500 you could contribute in 2022. If you are age 50 or older you are eligible to contribute an extra $7,500 for a total of $30,000 in 2023.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content