This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

During 2023, Medical Properties has found itself in need of de-leveraging and has sold off some properties to do so. One such sale was the sale of three hospitals to Prospect Medical Holdings. However, that sale was conditioned on Prospect then selling the hospitals to Yale New Haven Health. What can turn the situation around?

It might have balance sheet issues, lack growth prospects, or have a more complex corporate structure. Energy Transfer: A low value gives it a high yield Energy Transfer expects to generate $13.1 The master limited partnership (MLP) currently has an enterprisevalue (EV) of $95.2 billion to $13.5 times EV to EBITDA.

That leverage gives Carnival a high debt-to-equity ratio of 4.6. Nevertheless, investors should still take into account Carnival's debt -- which is reflected in its higher enterprisevalue instead of its lower market capitalization -- when valuing its stock. It ended fiscal 2019 with $9.7 billion in cash and equivalents.

When Energy Transfer cut its distribution in 2020, it was because its leverage became too high, and it needed to pay down debt. After getting its leverage down, it was able to not only return its distribution to pre-cut levels, but its quarterly distribution of 31.5 cents is now higher than the 30.5

BigBear.ai's prospects sounded promising, but it broadly missed its rosy pre-merger targets. Its low enterprisevalue of $670 million might even make it a compelling takeover target for a larger tech company. That flexible approach helped the company carve out a tiny niche in the crowded analytics market. wasn’t one of them.

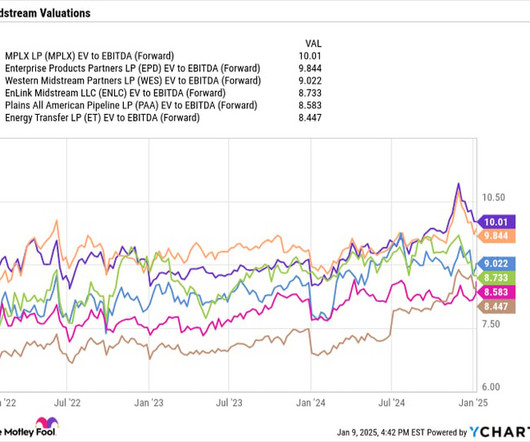

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 It and Enterprise also have the most attractive yields of the group at 8.1% and 7.2%, respectively.

Without reducing debt any further, the company is on track to get to 3 times leverage (net debt/adjusted EBITDA) by year end. At that point, Western Midstream will have reached its leverage goal and be set up to pay out enhanced distributions above its base distribution in 2025. or more a quarter in enhanced distributions.

Let's size up Royal Caribbean's prospects heading into its quarterly update and see where the potential headwinds can shift the stock out of cruise control. However, it commands a higher market cap and enterprisevalue than its larger rival Carnival. The tailwinds are there. Image source: Getty Images.

The company's balance sheet is currently in good shape, with leverage (as used by rating agencies) toward the low end of its 4x to 4.5x Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple. target range. times distribution coverage ratio in the second quarter.

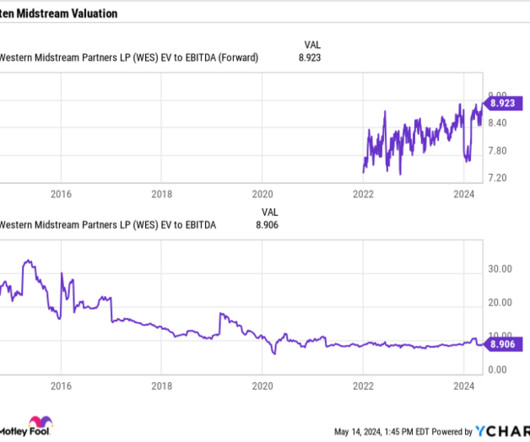

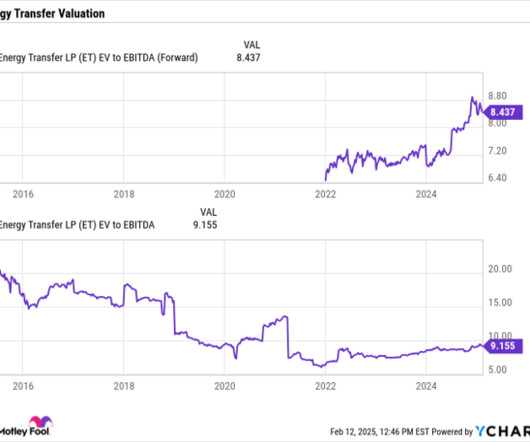

The value proposition While Energy Transfer's unit price has surged this year, it still trades at a reasonable valuation compared to its peers: ET EV to EBITDA (Forward) data by YCharts As that chart shows, Energy Transfer trades at less than 9 times its forward enterprisevalue -to-EBITDA, which is near the bottom of the barrel in its peer group.

Let's take a closer look at the midstream company's Q2 results, distribution, long-term prospects, and whether now is a good time to buy the stock. It ended the quarter with leverage of 3 times. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA.

As restaurant volumes climb, Chipotle will enjoy more operating leverage over its fixed cost base, which shows up in an expanding operating margin. The stock is expensive, despite its growth prospects Clearly, Chipotle has a bright future ahead of it. The price of a stock doesn't matter -- its market cap and enterprisevalue do.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017.

Profitability has risen at an even faster pace, showing the operating leverage in the company's business as it gains scale. The company's legacy apps business, meanwhile, saw revenue increase 7% to $369 million. Overall revenue climbed 44% to $1.08 Gross margins for the quarter came in at 73.8%, a huge jump from 65.5% a year ago.

Add that to its high-yielding payout (currently 8.9%) and growth prospects, and the MLP could continue producing strong total returns in 2024 and beyond. As the chart in the upper left-hand corner of that slide shows, the MLP trades at about 8 times its enterprisevalue to EBITDA. There's no discernable reason for the discount.

billion HEYDUDE buyout , but its leverage is more than manageable. It's easy to see why this was a hot IPO in 2018 given its heady growth prospects at the time. Huya trades at an enterprisevalue of negative $490 million. You can buy Crocs stock for just 7 times its earnings guidance for 2023.

The deal values Masonite at an enterprisevalue (market cap plus net debt) of 8.6 Still, suppose you are bullish on the housing market's long-term growth prospects and are willing to tolerate some near-term risk due to its current weakness. times adjusted EBITDA, or around 6.8

Increased M&A activity is generally a positive sign that management sees good prospects ahead. As a starting point, the XTO Energy deal was big , working out to more than 11% of ExxonMobil's enterprisevalue at the time. of Exxon's enterprisevalue based on the terms of the deal. Let's take a closer look.

per share in cash, representing a total enterprisevalue of approximately $4.6 We will continue to aggressively invest in the innovative solutions organizations need to more deeply engage with their customers, prospects, and employees that are so critical to their success.”

Some of the information we provide during today's call regarding our future expectations, plans, and prospects may constitute forward-looking statements. MicroStrategy is well-positions how our organizations build and deploy AI applications to users by leveraging the core capabilities of our leading BI platform.

As you think about all these comments, we're super excited where we are with the business and the prospects for the future. One is the enterprisevalue that we're creating by making investments in the Sculptor franchise should lead to a higher overall equity valuation for Rithm at the parent level.

In the broad strokes, the earnings multiple valuation method involves applying an industry-based multiple to the earnings of a business to arrive at an implied enterprisevalue. From this enterprisevalue, subtracting net debt gives the equity value.

C3 AI's customer base continues to expand, both within and across industries, while maintaining exceptional levels of customer satisfaction by our continued focus on delivering measurable, significant enterprisevalue. We leverage all layers of the AI tech stack, silicon cloud infrastructure services, and foundation models.

There is a cliche that price is what you pay, and value is what you get. All a stock price tells you is what other investors or prospective investors or soon to be former investors are willing to transact at the moment. My main problem with priced earnings is again, there's no leverage consideration. That's actually not bad.

“It gets back to the ability to grow the operating performance of the companies and making sure that returns” come from that rather than from “financial leverage,” he tells Bloomberg. And the use of PIK and other forms of so-called “back leverage” makes it even more difficult to get a clear picture on the state of privately owned companies.

We have acquired PDP for an enterprisevalue of $118 million in a combination consisting of roughly one-third stock and two-thirds cash. As part of the transaction with PDP, we have entered into a debt facility that will have less than one times leverage for the pro forma company at close. times next 12 months EBITDA.

Leveraging our industry-leading interoperability engine, we enable partners to embed our HCM solution within their platform for a seamless client experience. Higher lead generation investments, leveraging interest income last year, and driving productivity as we scale and moderate sales head count growth this year.

This in itself should drive long-term enterprisevalue creation through earnings outperformance. Beyond just a market-driven increase in earnings, we have also proven that we can outperform the industry by leveraging our structural advantages and intend to continue doing so going forward.

There's a lot of interesting things that look fun that just don't have the value quite yet, that folks especially from a business, enterprisevalue really ready to go spend significant dollars on. There's a lot of co pilot capabilities. That actually has been significantly better than what we had anticipated.

Theres no universally agreed-upon definition of the middle market, but typically it includes companies with annual revenues in the low hundreds of millions and enterprisevalues that dont quite reach the stratosphere. Leveraging Technology and Data Gone are the days when deal sourcing was solely about handshakes and business cards.

This helps support the franchise, generates great returns for the house, and should increase enterprisevalue for both Sculptor and Rithm at the top of the house. And one of the things you'll see is the leverage of the overall platform. Very excited for the prospects of that business.

Sean Klimczak, global head of Blackstone Infrastructure and Nadeem Meghji, global co-head of Blackstone Real Estate, said: “Prior to AirTrunk, Blackstone’s portfolio consisted of US$55bn (€49.8bn) of data centres including facilities under construction, along with over US$70bn in prospective pipeline development.”

We remain cautiously optimistic about the long-term prospects of our defense business, and we believe we can progress toward a more historical level of performance over time. billion with a total enterprisevalue of approximately $8.3 As you know, operating leverage in our business is meaningful.

By bringing together complementary leading data assets across a broad range of industries on the most innovative, sophisticated data visualization platform, the combined business will empower brands and retailers to collaborate, better service their customers, respond to trends and leverage more powerful insights to drive growth.

We can help formulate acquisition strategies, identify prospective acquisition targets, initiate contact, assist in negotiating terms of an acquisition, and help obtain acquisition financing when necessary.” At ABI, we start every review of a prospective sale engagement from a buyer’s perspective.

If Congress is unable to reach an agreement within the next 10 days, the federal government could once again be funded under a short-term or a long-term continuing resolution or face the prospect of a government shutdown.

As we enter the back half of '23, we remain bullish on our full-year prospects and believe we are well-positioned to achieve continued overall record revenues for the full year. As you can see, 2023 is off to a strong start with first-half revenue up 61% over the first half of 2022.

So, in February 2022, at our year-end results presentation, we noted the prospects of a global economic downturn post the invasion of the Ukraine by Russia. So in November 2023, we announced the acquisition of Reldan at a $211 million enterprisevalue. It's anticipated to be value accretive on day one.

Wolfspeed's prospects should brighten as the macro environment improves and more companies shift from traditional silicon chips to silicon carbide ones. With an enterprisevalue of about $7 billion, Wolfspeed trades at nearly 7 times that estimate -- so it still isn't a screaming bargain after its latest post-earnings decline.

While the net lease transaction market continues to sort itself out, our team is doing a tremendous job leveraging our relationships and uncovering unique opportunities. Simultaneously, we have ramped up our efforts and leveraged our tenant relationships, exemplifying how we create proprietary deal flow and accretive off-market opportunities.

It's also nicely improved its balance sheet over the past few years so that its leverage is now in the lower half of its targeted 4 times to 4.5 Meanwhile, it plans to buy back stock once its leverage target is achieved. times range. It is looking to grow its distribution by 3% to 5% a year moving forward. Image source: Getty Images.

However, the company said it now has requests from more than 70 prospective data centers in 12 states. With its balance sheet and leverage in good shape, it appears well positioned to tackle this growth opportunity. From a valuation perspective, the stock trades at an enterprisevalue (EV) -to-EBITDA multiple of about 8.5

So again, really, really excited with the prospects of Sculptor and the overall team. So when you think about growth there, we're not just going to grow a business if we think we could deploy capital better in another area to increase enterprisevalue for the overall franchise. Performance is the No. AUM is going to follow.

At year-end, leverage stood at just 3.3 billion this year, while staying within our target leverage range of four to five times net debt to EBITDA without raising any additional equity. How would you sort of view that given your recent conversations with current and prospective tenants? We can deploy over $1.5 billion and $1.3

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content