This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

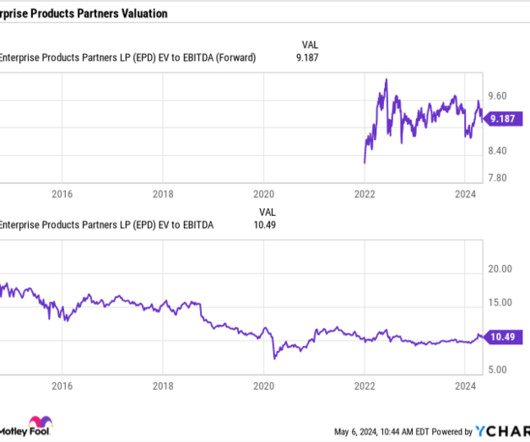

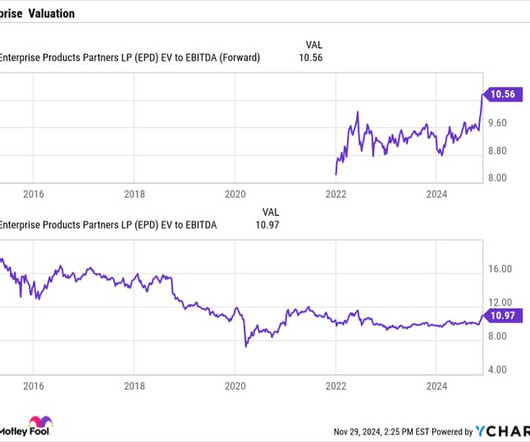

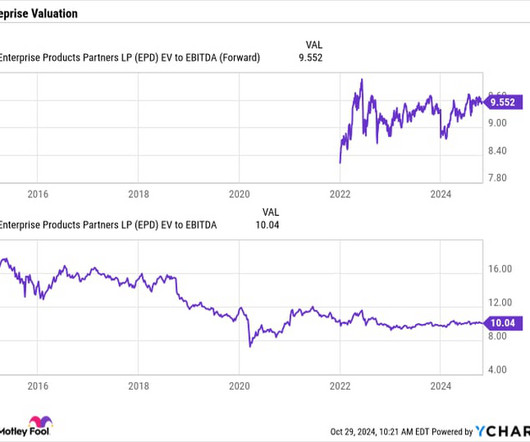

Enterprise ended the quarter with leverage of 3x. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. What this means for investors in simpler terms is that Enterprise's distribution payout is well covered by its cash flow. cents per unit.

I consider Enterprise's distribution extremely safe. The two biggest areas to look at when it comes to dividend safety are its distribution coverage ratio and leverage ratio. On that front, Enterprise had a robust 1.7x When the leverage at companies gets too high, there's a risk they may cut their dividend. billion to $3.75

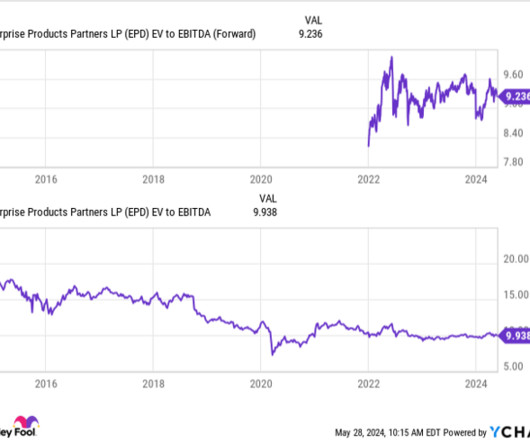

The company generates a lot of cash flow, and has historically taken a conservative posture with leverage , which is also why it has been able to consistently increase its distribution. Leverage currently stand at 3, which is low for the midstream industry. Enterprise currently has a robust forward yield of 7.2%

The company generates a lot of cash flow, and has historically taken a conservative posture with leverage , which is also why it has been able to consistently increase its distribution. Leverage currently stand at 3, which is low for the midstream industry. Enterprise currently has a robust forward yield of 7.2%

Over the past five years, Enterprise has averaged about a 13% return on invested capital, so these growth projects should provide meaningful growth to the company in the years ahead. At a similar return, the approximately $10.5 It ended the quarter with leverage of 3 times.

Enterprise's consistency stems from its largely fee-based model, where the company only takes on minimal commodity or spread risk. Meanwhile, it has historically been conservative with its leverage, distribution coverage ratio, and growth capital expenditure (capex) spending. Currently, the stock carries a forward yield of about 6.2%.

Based on its DCF, Enterprise's distribution coverage ratio was 1.7x. It ended the quarter with leverage of 3x, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. Enterprise currently has $6.9 billion in projects that are under construction.

compounded annually, which will allow us to use our cash flow generation to pay down debt and rebuild the balance sheet as we work toward investment-grade leverage metrics. We are also working to further leverage and monetize our industry-leading land-based assets in the Caribbean and Alaska. And then -- is that the right math?

And following the Fitch upgrade in July, our balance sheet now has two investment-grade ratings and our dividend yield is in line with the S&P 500. Around the world, we're continuing to develop our JV partnerships and leveraging our strengths. Gross leverage ended the quarter at 2.9 After reinvesting $3.6 Operator Thank you.

My main problem with priced earnings is again, there's no leverage consideration. But then, so whether that's price or whether it's enterprisevalue, we can, there's applications for each. Here's our target return on invested capital. Jim Gillies: Sure or against its own history. But what are you doing with it?

It's a lot like return on invested capital. But I think looking at cash flow metrics, if you want to compare forward cash flow to a company's enterprisevalue, so that common stock, market capitalization, plus the debt piece, those are not bad to pair together. But I'll say this. ROUNTA can't give you everything.

And as with our Lumos JV, T-Mobile will leverage our scale, brand, distribution and existing customer relationships to grow faster and to do it smarter. It's doing it with partners so that we can get more leverage on our equity dollars. We think our unique asset set allows us to drive enterprisevalue and gives us advantage in fiber.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content