This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many of these companies are structured as master limited partnerships (MLPs), which pass through their profits to their unitholders and as such don't pay corporate taxes. This portion is tax deferred until the stock is sold and reduces the owner's cost basis. This is a nice benefit, although it does add some paperwork come tax time.

Additionally, its breadth gives it leverage in distribution agreements for better positioning and promotions. It can also use that leverage to get new products on shelves and in front of potential customers, enabling it to expand its product lineup more easily than smaller competitors.

Private equity firms Apollo Global Management and BC Partners have joined forces to agree a deal to acquire GFL Environmentals Environmental Services business at an enterprisevalue of CAD8bn ($5.59bn). GFL expects to realise cash proceeds from the transaction of approximately CAD6.2bn net of the retained equity and taxes.

Those entities have some tax complexities, which tend to weigh on their valuations compared to traditional corporations. In addition, some already tax-advantaged accounts (IRAs) don't allow investors to hold partnership units, and many stock market indexes don't allow partnerships. They're both publicly traded limited partnerships.

At a stock price of around $39 per share, DraftKings trades for an enterprisevalue roughly 21 times management's 2025 outlook for earnings before interest, taxes, depreciation, and amortization ( EBITDA ). All three expand its data expertise and will integrate with new bet options.

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 < Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6

It's trading for 26 times trailing earnings, and given its debt-bloated balance sheet, that multiple jumps to nearly 60 if you swap out market cap for enterprisevalue as the numerator. Carnival has only been profitable twice in the past 18 quarters. Carnival also isn't exactly out of favor right now. It has bought back $6.6

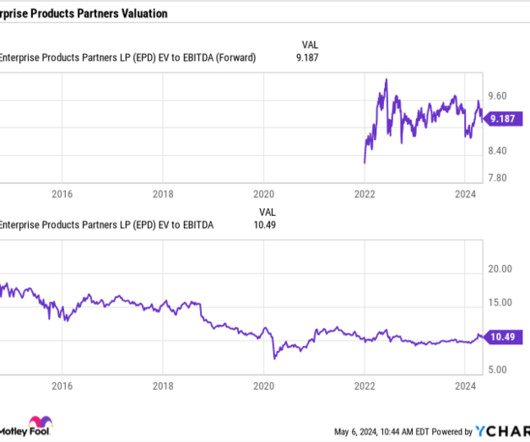

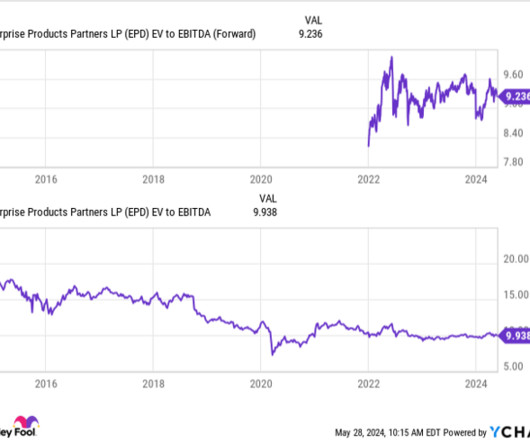

Solid Q1 results Enterprise once again turned in solid results when it reported its first-quarter results, as its total gross operating profit rose 7% to $2.5 Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, rose 6% to nearly $2.5 Enterprise ended the quarter with leverage of 3x.

Energy Transfer is structured as a master limited partnership (MLP), so investors will get a K-1 and have unique tax advantages (and obligations). Approximately 90% of Energy Transfer's 2024 earnings before interest, taxes, depreciation, and amortization ( EBITDA ) is projected to come from fee-based activities.

On an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) basis, it generated a profit of $3.3 That leverage gives Carnival a high debt-to-equity ratio of 4.6. With an enterprisevalue of $48 billion, Carnival doesn't seem expensive at 2 times next year's sales and 9 times its adjusted EBITDA.

However, there's much less of a tax drag on the transaction. Share repurchases incur a 1% tax (paid by the business); qualified dividends are taxed at the long-term capital gains tax rate (paid by the shareholder). The shares trade for an enterprisevalue- to- EBITDA ratio of 11. and Verizon (8.2).

Its balance sheet isn't pretty ChargePoint insists it can turn profitable on an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) basis by the fourth quarter of calendar 2024 (which lines up with the third and fourth quarters of fiscal 2024).

Q3 earnings preview for Block For the third quarter, Block has guided for a headline 17% year-over-year increase in the gross profit while forecasting $695 million in adjusted earnings before interest, tax, depreciation, and amortization ( EBITDA ), accelerating by 46% from last year.

Shares currently trade for an enterprisevalue/earnings before interest, taxes, depreciation, and amortization (EV/ EBITDA ) multiple of just 5x. That leverage puts added pressure on management if oil prices decline in the future, making it less profitable to drill. By comparison, Chevron trades for a 6.6x

billion of adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) this year. With an enterprisevalue (EV) of $96.6 Meanwhile, it expects its leverage ratio to be at the lower end of its 4x-4.5x Low valuation = high yield Midstream giant Energy Transfer expects to produce $13.1 billion to $13.5

The company claimed it could deliver a compound annual growth rate (CAGR) of 40%, taking revenue from $140 million in 2020 to $388 million in 2023 while expanding its gross margin from 30% to 50% and keeping its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) margins in the high teens.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower.

It's leveraging its AI investments to grow two businesses at scale. Meanwhile, it's using the considerable cash flows it generates to buy back shares, boosting the value of future earnings to shareholders. Microsoft's forward P/E ratio sits around 31.5, as of this writing. Most recently, it acquired medical waste specialist Stericycle.

Its leveraged exposure to oil production has pushed down Occidental's share price to levels it hasn't seen since the beginning of 2022. Occidental's current share price of about $50 gives it an enterprise-value -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just 5.3.

The company generates a lot of cash flow, and has historically taken a conservative posture with leverage , which is also why it has been able to consistently increase its distribution. Leverage currently stand at 3, which is low for the midstream industry. Enterprise currently has a robust forward yield of 7.2% That's right.

The company generates a lot of cash flow, and has historically taken a conservative posture with leverage , which is also why it has been able to consistently increase its distribution. Leverage currently stand at 3, which is low for the midstream industry. Enterprise currently has a robust forward yield of 7.2% That's right.

I consider Enterprise's distribution extremely safe. The two biggest areas to look at when it comes to dividend safety are its distribution coverage ratio and leverage ratio. On that front, Enterprise had a robust 1.7x When the leverage at companies gets too high, there's a risk they may cut their dividend.

While similar, distributions include a return on capital that is untaxed until the units are typically sold, making them tax-deferred. However, investors do receive what is called a K-1 and must fill out some extra tax forms. Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple.

The MLP has grown its adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) from $13.1 Its earnings growth has also helped drive down its leverage ratio , which it expects will be toward the low end of its 4.0-4.5 What has fueled Energy Transfer's rally? billion in 2022 to $13.7 billion-$14.8

for adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). For perspective, its enterprisevalue is just $6.2 For years, PayPal's leadership has talked about leveraging its consumer data. It wants to find ways to grow its enterprise business, and Chriss' expertise in this area will help.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) increased 20% in the second quarter to almost $3.8 Energy Transfer's leverage ratio is now in the lower half of its 4.0 It's even cheaper when looking at its forward enterprisevalue (EV) to EBITDA multiple (less than 8.0

That rising leverage made Carnival a risky stock to hold as interest rates rose, and its stock sank to a 30-year low of $6.38 Carnival's exposure to macro headwinds and high leverage still make it a tough stock to love, but I believe it has a viable path toward generating a 10-bagger gain within the next 20 years. per share on Oct.

The deal puts an enterprisevalue of $16.5 Novo Nordisk, for its part, will leverage Catalent's status as a key manufacturing subcontractor to expand its fill-finish capacity to better meet the high demand for its popular obesity drug, Wegovy. per share in cash -- a 16.5% billion on Catalent. "We

It recently announced it was buying PFSweb for $181 million, or an enterprisevalue of $142 million, which includes the company's cash balance of $39 million. However, its PFS Operations' adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) were $23.2 Now, GXO has made another promising deal.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017.

After closing the deal for GIP's interest in EnLink, Oneok plans to pursue the acquisition of EnLink's publicly traded shares in a tax-free transaction (i.e., billion enterprisevalue. leverage ratio after closing its deals with GIP. It anticipates leverage to steadily trend down toward its long-term target of 3.5

These growth drivers have the MLP on track to increase its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) by 12% at the midpoint of its guidance range this year. Meanwhile, its leverage ratio is trending toward the low end of its 4.0 There's no noticeable reason for the valuation discount.

A consistent performer The key to Enterprise's success over the years has been consistency, which has helped the pipeline company increase its distribution for 26 straight years through various ups and downs in the energy markets. For Q2, the Enterprise saw its total gross-operating margin increase nearly 11% to $2.4

With an enterprisevalue of $6.9 billion, Wolfspeed looks reasonably valued at 8 times next year's sales -- and it could climb higher as the silicon carbide market finally heats up. With an enterprisevalue of $21.8 billion, Reddit trades at 14 times next year's sales and 49 times its adjusted EBITDA.

Its adjusted earnings per share (EPS) was flat year over year at $0.25, while its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) edged up 2% to $1.88 Kinder Morgan ended the quarter with a leverage ratio (net debt divided by trailing-12-month adjusted EBITDA) of 4.1.

Adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) and distributable cash flow (DCF), two common metrics used to evaluate midstream companies, also both rose modestly. The company ended the quarter with a leverage ratio (net debt divided by trailing-12-month adjusted EBITDA) of 4.1.

Moreover, management also guided for adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of at least $100 million in 2025, signaling the company's focus on operating leverage. Another metric worth analyzing is its enterprisevalue. Hims & Hers Health has an enterprisevalue of $1.3

Profitability has risen at an even faster pace, showing the operating leverage in the company's business as it gains scale. Adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, soared 80% to $601 million. Gross margins for the quarter came in at 73.8%, a huge jump from 65.5% a year ago.

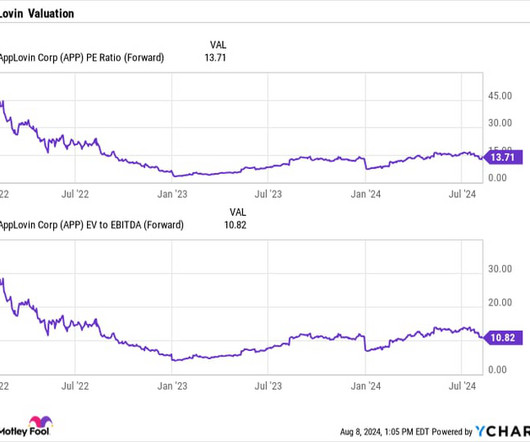

Beyond the core software ecosystem, AppLovin also counts on a portfolio of more than 200 free-to-play mobile games as a separate business driver that leverages the company's marketing capabilities. The stock trades at 30 times its consensus 2024 EBITDA estimate as an enterprisevalue (EV)-to-forward-EBITDA ratio.

As restaurant volumes climb, Chipotle will enjoy more operating leverage over its fixed cost base, which shows up in an expanding operating margin. The price of a stock doesn't matter -- its market cap and enterprisevalue do. The chain is generating just over $3.1 Chipotle's operating margin has expanded to 16.7%

Operating income rose to $560 million from $120 million a year ago, while adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) climbed over 75% to $1.2 CCL PE Ratio (Forward) data by YCharts The company carries a fair amount of leverage (net debt/EBITDA), which would be about 4.8

MidEuropa, a leading European private equity investor with deep roots in Central Europe , today announces that it has entered into an agreement to sell Profi Rom Food (“Profi” or the “Company”), one of Romania’s major food retailers, to Ahold Delhaize for an EnterpriseValue of approximately € 1.3bn pre-IFRS16 (€ 1.8bn post-IFRS 16).

It slightly narrowed its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) loss from $861 million to $860 million.Those headline numbers weren't impressive, but Rivian had already warned investors of a slowdown this year as it focused on upgrading its plants instead of ramping up its deliveries.

But instead of following that trend and expanding into the wireless market, Lumen doubled down on the legacy wireline market through a series of mergers and acquisitions while expanding its portfolio of cloud, security, and collaboration services for enterprise customers. Based on those expectations and its enterprisevalue of $19.4

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content