This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It might have balance sheet issues, lack growth prospects, or have a more complex corporate structure. Those entities have some tax complexities, which tend to weigh on their valuations compared to traditional corporations. Energy Transfer: A low value gives it a high yield Energy Transfer expects to generate $13.1

However, the robust growth prospects of its data center/AI-related business shouldn't detract from the strength of its underlying growth driver coming from the retrofit opportunity in commercial buildings as it seeks to improve efficiency and meet its net zero emissions aims. Data source: Johnson Controls presentations. Chart by author.

On an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) basis, it generated a profit of $3.3 Nevertheless, investors should still take into account Carnival's debt -- which is reflected in its higher enterprisevalue instead of its lower market capitalization -- when valuing its stock.

At its current price, it trades near the high end of its historical enterprisevalue -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) range, excluding the impact of the COVID-19 pandemic. That said, the stock's valuation has grown to reflect the company's strong prospects.

Energy Transfer is structured as a master limited partnership (MLP), so investors will get a K-1 and have unique tax advantages (and obligations). Approximately 90% of Energy Transfer's 2024 earnings before interest, taxes, depreciation, and amortization ( EBITDA ) is projected to come from fee-based activities.

The company claimed it could deliver a compound annual growth rate (CAGR) of 40%, taking revenue from $140 million in 2020 to $388 million in 2023 while expanding its gross margin from 30% to 50% and keeping its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) margins in the high teens.

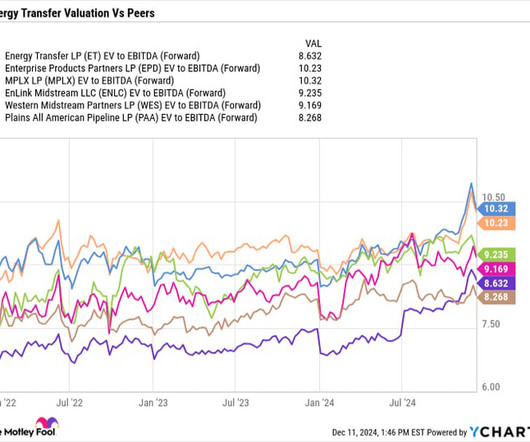

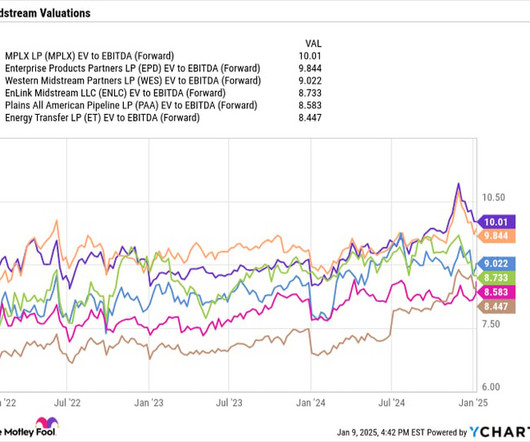

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 It and Enterprise also have the most attractive yields of the group at 8.1% and 7.2%, respectively.

But Buffett would describe the prospects for Coca-Cola as “better than the average American corporation.” and an enterprisevalue -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio of 6, the shares are trading at a fair value. which is roughly in line with the S&P 500.

While similar, distributions include a return on capital that is untaxed until the units are typically sold, making them tax-deferred. However, investors do receive what is called a K-1 and must fill out some extra tax forms. Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple.

These growth drivers have the MLP on track to increase its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) by 12% at the midpoint of its guidance range this year. Further, as noted, the MLP has strong growth prospects that are growing stronger. times target range. per share by 2027.

Let's look at the company's most recent quarterly results, future prospects, and valuation to see if this is a good time to buy the beaten-down stock. It also said that it is seeing success in newer verticals such as enterprise restaurant chains and food and beverage retailers. billion and an enterprisevalue (EV) of about $11.9

The stock is expensive, despite its growth prospects Clearly, Chipotle has a bright future ahead of it. The price of a stock doesn't matter -- its market cap and enterprisevalue do. Assuming operating margin expands to 20% in that period and a 20% corporate tax rate, its net income will eventually hit $5.6

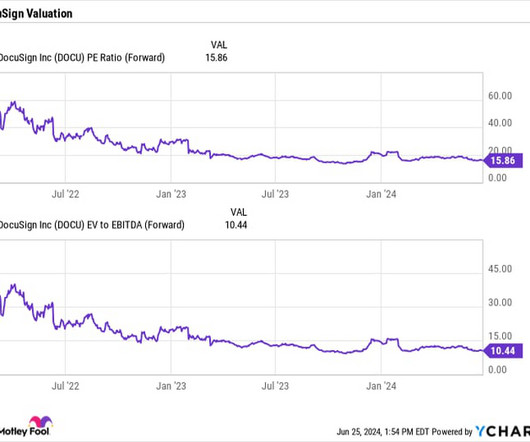

billion in net cash and marketable securities on its balance sheet, the stock trades at an enterprise-value -to-forward-sales ratio of just 3.6 That's just plain cheap for a software company that is still growing nicely and has strong potential prospects ahead. Taking into consideration the $1.9 the stock is cheap.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). Should you invest $1,000 in Enterprise Products Partners right now?

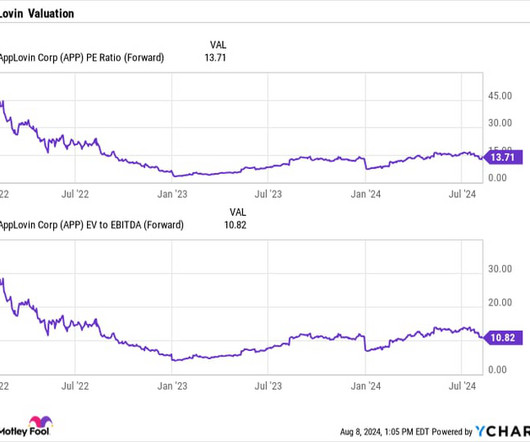

Adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, soared 80% to $601 million. Gross margins for the quarter came in at 73.8%, a huge jump from 65.5% a year ago. In the second quarter, AppLovin's net income nearly quadrupled from $80 million to $309.9

The growth prospects aren't very appetizing Cracker Barrel's management already has a pretty detailed long-term vision in place. Cracker Barrel's growth prospects aren't inspiring. In fiscal 2027, it hopes to earn adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) of about $400 million.

However, management is forecasting a profit on an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) basis by the end of 2025. The business reported an adjusted net loss of $4 million last quarter, but that's where Nvidia's recent investment is pivotal for Applied Digital's growth prospects.

Let's take a closer look at the midstream company's Q2 results, distribution, long-term prospects, and whether now is a good time to buy the stock. For Q2, the Enterprise saw its total gross-operating margin increase nearly 11% to $2.4 It generated distributable cash flow of $1.8

Let's look at the company's most recent quarterly results, future prospects, and valuation to find the answer. The company reported $57 million in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) , compared to a negative $17 million a year ago. With an enterprisevalue (EV) of about $13.7

It has also received requests from more than 40 prospective data centers in 10 states that could use 10 BCF a day of natural gas. Attractive valuation Besides having some of the best growth opportunities in the pipeline space, Energy Transfer is also one of the most attractively valued MLPs. billion and $3.5 Image source: Getty Images.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) also improved from negative $94 million in 2022 to positive $536 million in 2023. Robinhood's prospects are brightening, but investors shouldn't overlook its weaknesses. With an enterprisevalue of $23.4

Do you feel good about T-Mobile's prospects moving forward with that or is that something that you're wary of? That is enterprisevalue to earnings before interest, tax, depreciation, amortization. Jason Moser: I think on the whole you have to be you have to feel pretty good about this.

Investors have gotten more optimistic about the company's prospects as it skirted bankruptcy, refinanced its debt, and inched closer to profitability. Add its net debt of approximately $5 billion, and its enterprisevalue ( EV ) is $15 billion. It is hard to value Carvana, given its inconsistent profitability.

In the broad strokes, the earnings multiple valuation method involves applying an industry-based multiple to the earnings of a business to arrive at an implied enterprisevalue. From this enterprisevalue, subtracting net debt gives the equity value.

There is a cliche that price is what you pay, and value is what you get. All a stock price tells you is what other investors or prospective investors or soon to be former investors are willing to transact at the moment. But then, so whether that's price or whether it's enterprisevalue, we can, there's applications for each.

Or growth may be stymied by an inability to utilize social media and marketing to differentiate and develop new prospects. Even when done successfully, efforts to insulate clients from the firm are at their core counterproductive, since advisors could ideally use this time for prospecting or fostering existing relationships.

We have acquired PDP for an enterprisevalue of $118 million in a combination consisting of roughly one-third stock and two-thirds cash. We are enthusiastic about this new, refreshed, and transformed Turtle Beach and its future prospects for shareholders, employees, and customers. times next 12 months EBITDA.

This helps support the franchise, generates great returns for the house, and should increase enterprisevalue for both Sculptor and Rithm at the top of the house. Our second-quarter pre-tax income was $248 million, delivering a 23% ROE, excluding mark-to-market on the owned portfolio.

This in itself should drive long-term enterprisevalue creation through earnings outperformance. The Compass reverse prospecting tool is a powerful new tool that enables agents and their homeowners to identify which of the 33,000 Compass agents and their millions of buyers have viewed, shared, favorited or commented on their listing.

We understand and appreciate the complexities of our clients’ enterprises, and we unwaveringly espouse to our motto of doing good work for good people.” In order to do that, you need a succession plan that fulfills your desires and addresses all the issues of estate planning and taxes.

If Congress is unable to reach an agreement within the next 10 days, the federal government could once again be funded under a short-term or a long-term continuing resolution or face the prospect of a government shutdown. We expect our effective tax rate for the full year 2023 to be approximately 29%, exclusive of any discrete items.

So, in February 2022, at our year-end results presentation, we noted the prospects of a global economic downturn post the invasion of the Ukraine by Russia. So in November 2023, we announced the acquisition of Reldan at a $211 million enterprisevalue. It's anticipated to be value accretive on day one.

Enterprise-value-to-EBIT ratio 714 12.3 EBIT = earnings before interest and taxes. This growth stock may have a very different investment thesis than TSMC's more value-oriented buy-in thesis, but it is no less interesting. The stock is also far more affordable as measured by several key metrics. Price-to-sales ratio 7.9

Buyers who purchase items through Etsy's mobile app have a 40% higher lifetime value, making this ongoing shift very important to its prospects. In Etsy's case, customer lifetime value equals the present value of all the future revenue it would generate from a given user.

The stock is down 95% from the all-time high it hit three years ago when the growth prospects for the leading provider of remote medical consultations were far kinder. The transaction was valued at $18.5 Today you can buy all of Teladoc at an enterprisevalue barely above $3 billion. billion at the time.

He began as an attorney working on things like taxes and, and trusts in estates and consulting for various RIA firms when he became an RIA and eventually bought creative planning when it had, you know, a handful of, of clients and, you know, 30, $35 million. This is Masters in business with Barry Ritholtz on Bloomberg Radio.

We provide guidance on several other inputs in our earnings release, including acquisition and disposition volume, general and administrative expenses, non-reimbursable real estate expenses, and income and other tax expenses. times, which is flat quarter-over-quarter. With that, I'd like to turn the call back over to Joey. Haendel St.

The difference between the two is tax-related, as distributions have a return of capital component that is tax-deferred. While it involves a little extra paperwork come tax time, this part of the distribution reduces an investment's cost basis and is not taxed until the stock is sold, which is a nice added bonus.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) and free cash flow ( FCF ) also turned positive in 2023 as it streamlined its spending. Based on these expectations and its enterprisevalue of roughly $8 billion, Roku's stock looks reasonably valued at less than 2 times next year's projected sales.

However, with an enterprisevalue of $21.6 That's why Toast's adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) finally turned positive in 2023 and grew more than eightfold year over year in the first nine months of 2024. billion,Toast looks pretty cheap at 3.5 times next year's sales.

Does Alphabet have below-average long-term prospects? billion in adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). Considering it has an enterprisevalue of $62 billion, it trades at just 10 to 11 times this year's EBTIDA. Those are quality financial results as far as I'm concerned.

However, its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) broadly missed its initial expectations. With an enterprisevalue of $268 million, it looks dirt cheap at less than 1 times this year's sales. Are brighter days ahead for EVgo? billion loan facility from the U.S.

However, the underlying strong business prospects of those stocks still make them great picks for long-term investors. But have ExxonMobil's long-term business prospects faltered? Graham also knew, though, that business fundamentals matter over the long term. Sometimes, investors' "votes" temporarily cause good stocks to decline.

Their growth prospects Enbridge projects adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) between CA$19.4 Over the longer term, the growth prospects for these two companies should be similar because they face many of the same industry dynamics and opportunities. impact Enbridge's business?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content