This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Investing in certain types of accounts can not only help you build wealth, but can save you money on taxes right now. Here are two of those types of accounts that millions of Americans can use to invest thousands of dollars and get a bigger tax refund in 2024 and beyond. The main difference between the two is the tax treatment.

Both offer excellent tax advantages. One of the drawbacks of 401(k)s, in the eyes of some investors, is that they tend to offer a limited menu of investment choices -- perhaps just a dozen or so mutualfunds or exchange-tradedfunds (ETFs). Your taxable earnings shrink by $7,000, shrinking your tax bill.

There's nothing wrong with dipping your first toe in Wall Street's waters through a low-cost exchange-tradedfund (ETF). What's an exchange-tradedfund? An exchange-tradedfund is a collection of securities that you can buy or sell through a brokerage firm on a stock exchange.

The bulk of them are managed by mutualfund companies, with most of those companies limiting your investment choices to their family of funds. In fact, you may not even have access to that fund company's entire fund lineup. But there are scenarios in which you might be better off doing exactly that.

The emergence of spot Bitcoin exchange-tradedfunds (ETFs) has opened up a new avenue for investors to enter the cryptocurrency market without the complexities of managing crypto wallets and navigating exchanges. After doing so, however, I could buy whatever ETFs, stocks, or mutualfunds I wanted.

For example, a Roth IRA offers exceptional tax benefits, making it an outstanding retirement planning tool. It also comes with immediate tax benefits. For example, taxes on 401(k) contributions are deferred until retirement, meaning you can lower your taxable income during your working years by contributing more to your 401(k).

Not only do the holidays inspire goodwill and cheer, but many people are interested in writing off their donations as we close out the tax year. But there's also a lot of confusion about charitable donations and when you can write them off for tax purposes. To write off a charitable deduction, you'll need to itemize your tax return.

The 401(k) is a cornerstone of retirement planning -- it's tax-friendly, hands-off, and convenient. Contributions to a traditional IRA may be deductible, and earnings grow tax-deferred until you take withdrawals in retirement. Contributions to a Roth IRA are made with after-tax money, and withdrawals are tax-free in retirement.

Even if you add investments outside of retirement accounts, like individual stocks, bonds, and mutualfunds, 50% of American households have less than $9,000 invested. The IRA comes with tax incentives. For every dollar you contribute to a traditional IRA, you can deduct it from your tax return. That's a far cry from $1.46

Many people also have a tax refund coming their way in the next few months. If you choose the IRA route, you'll be able to decide how you want to invest your money and when to pay taxes on it. Mutualfunds and exchange-tradedfunds (ETFs) charge expense ratios, which are an annual fee you pay the fund manager.

Here's how I plan to retire as a millionaire and pay no taxes. Once it's open, you can contribute up to $7,000 in 2024, and the amount typically stays the same or rises every tax year. The beauty of that is you don't pay taxes on your distributions in retirement. So let's walk through this together.

A family office may offer financial planning, investment management, tax expertise, and charitable giving opportunities. Hedge funds are often far riskier than investing in a mutualfund, and they are exclusively for people with at least $200,000 in income or $1 million in net worth.

Exchange-tradedfunds, or ETFs, can be superb investing vehicles. ETFs are both cost- and tax-efficient, and they can instantly diversify a portfolio across a broad swath of the equity markets or within a specific sector/theme. The fund's popularity comes from its impressive performance.

Money market funds A money market fund is a mutualfund that invests in low-risk securities. For example, a money market fund might invest in municipal debt, corporate bonds, or Treasury bills. There are two types of annuities: income annuities and tax-deferred annuities.

The program could increase its revenue by increasing tax rates or raising the payroll income tax cap. Investors should build a portfolio of stocks, bonds, mutualfunds, exchange-tradedfunds (ETFs), and other securities. There are a few different options to overcome the projected solvency issues.

It's smart to make good use of tax-advantaged retirement savings accounts such as 401(k)s and IRAs. In an IRA, you can invest in individual stocks and/or in mutualfunds and exchange-tradedfunds (ETFs). However much you're investing these days, consider investing more.

At the Money: MutualFunds vs. ETFs with Dave Nadig, Financial Futurist for Vetta Fi (December 13, 2023) What’s the best instrument for your investments? Mutualfunds or ETFs? But over the past few decades the mutualfund has been losing the battle for investors attention. Dave Nadig : Absolutely not!

They built their wealth by consistently investing in index funds or exchange-tradedfunds (ETFs). For example, a fund that tracks the S&P 500 gives you a very small piece of the top 500 U.S. But you might instead look to a gold ETF or mutualfund. But you don't have to. companies.

Image source: The Motley Fool/Upsplash There are many ways you can invest your money, from traditional options like stocks and mutualfunds to more recent options like cryptocurrency. These are a must, because they help you save on taxes. But anybody who is working can open an IRA and start making tax-deductible contributions.

Using a strategy called tax-loss harvesting, you can earn capital gains tax credits on your investment losses. What is Tax-Loss Harvesting? This strategy is when you sell stocks, mutualfunds, exchange-tradedfunds (ETFs), and other investments carrying a loss to offset gains from other investments sold.

Sometimes, you may not even realize how much you're losing, especially if you're primarily focused on an investment's nominal return -- that is, its return before accounting for taxes, inflation, and investment fees. Here's a closer look at how you might be hurting your savings' growth without even knowing it. Image source: Getty Images.

Market: The stock market is made up of thousands of choices and one easy way to gain exposure to it is via mutualfunds. Costs/Expenses : ETFs typically have lower expense ratios compared to mutualfunds. Tax Efficiencies : ETFs are generally more tax-efficient than mutualfunds.

Joining an index tends to provide a short-term boost to a stock, as mutualfunds and exchange-tradedfunds (ETFs) tracking the index are required to buy shares of added companies. With the U.S. home market underbuilt by upwards of 3.5 Is Builders FirstSource stock a buy ahead of its inclusion in the S&P 500?

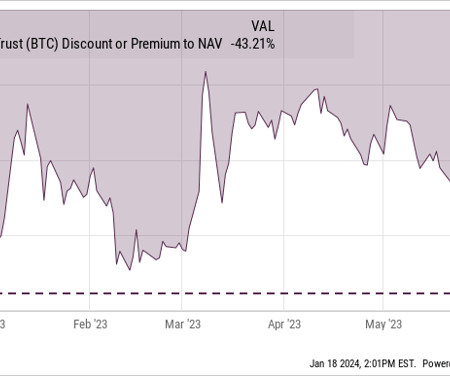

From the fund's public market entrance in May 2015 to the end of 2020, the Grayscale fund averaged a 37% price premium over its holdings in pure Bitcoin (CRYPTO: BTC). Early Bitcoin adopters appreciated the Grayscale fund's availability in ordinary stock-exchange accounts. in the ETF era.

Most employers and their plan providers will give investors a menu exclusively of mutualfunds and exchange-tradedfunds to pick from. Some of those mutualfunds, such as target date funds, can carry relatively high fees. All you'll have to worry about are capital gains taxes.

You can invest the money you deposit in the account in almost anything you choose, including stocks, bonds, mutualfunds, exchange-tradedfunds, and CDs. It's a powerful retirement savings vehicle because it offers important tax advantages.

When you enroll in an employer's 401(k) plan, you're generally given a "menu" of investment funds to choose from -- usually a few dozen at most. While some 401(k) plans offer excellent index funds and mutualfunds, my IRA allows me to invest in virtually any stock, bonds, exchange-tradedfunds (ETFs), or mutualfunds I want.

The best way to save for retirement is with tax-advantaged retirement accounts. If you only save through a regular brokerage account, you won't get any tax benefits. Roth IRAs let you make tax-free withdrawals in retirement. If you haven't set up an IRA already, do so immediately so you can start saving on taxes.

The firm is known for its diverse offerings including mutualfunds, exchange-tradedfunds (ETFs) , and its advanced risk management platform, Aladdin. The effective tax rate decreased to 20.9% In recent years, BlackRock has focused on enhancing its technological capabilities and expanding its global reach.

Tax-advantaged accounts There are a few different types of tax-advantaged investment accounts, and not all of them are geared toward retirement. What they have in common is that they can lower your tax bill and help boost your investments. 401(k) : This is a tax-deferred, employer-sponsored retirement plan.

You are limited to a fairly small menu of mutualfund and exchange-tradedfund choices made by your employer and the 401(k) manager. And it also might mean being forced to load up on funds that charge their own excessive fees. That might limit your ability to grow your money.

With a traditional IRA or a traditional 401(k), you get an upfront tax break; the amount you contribute for a certain tax year can be deducted from your taxable income for that year. So if you contribute $7,000 this year, your taxable earnings drop by $7,000, shrinking your tax bill. Available to most people.

To get there, you'll need to consistently invest a decent chunk of your paycheck, find the right investment strategies, and maximize tax benefits from 401(k)s and individual retirement accounts (IRAs). Tax-advantaged accounts can boost your retirement fund, so make sure you understand what's out there. million for retirement.

Exchange-tradedfunds (ETF) continue revolutionizing how investors build their portfolios, offering cost-effective ways to access diverse market segments. Their popularity stems from several key advantages: lower costs compared to mutualfunds, the ability to trade throughout the market day, and tax efficiency.

You have until the end of the year to set aside funds in a 401(k) at work and until April 15, 2025 (tax filing deadline) to make your contributions to an individual retirement account (IRA). You'll be able to invest in a variety of assets such as low-cost index funds , exchange-tradedfunds , growth stocks , and dividend-paying stocks.

More and more investors are discovering the benefits of adding exchange-tradedfunds (ETFs) to their portfolios. While these funds have some similarities to the mutualfunds that are offered by various investment firms, they are quite different overall.

Otherwise, the investment options in a 401(k) plan are limited and typically include mutualfunds, baskets of stocks that either are professionally managed or track a major index. If don't have access to a 401(k) or other employer-sponsored plan, there are other tax-advantaged retirement accounts to consider.

In fact, investing $100 per month in one simple exchange-tradedfund (ETF) will do the trick. It's not a high-flying tech fund. It's not an ETF that employs a complicated "black box" trading strategy either. Most mutualfund managers can't even do it. You can do the same. The only catch?

Regular IRAs don't permit this because these metals are considered collectibles, and the IRS will consider it a distribution if you spend any of your regular IRA funds on coins or bullion. This could trigger tax bills, as well as a 10% early withdrawal penalty if you're under 59 1/2 at the time you make those investments.

Exchangetradedfunds (ETFs) are more popular with investors than ever. Like mutualfunds, ETFs offer the benefit of diversification but with intraday liquidity, potentially lower fees, and tax advantages. Just over the past year alone, the global ETF market grew from $10.1 trillion to $13 trillion.

With that in mind, I've made a somewhat different Magnificent Seven list of the largest exchange-tradedfunds, or ETFs in the market. They are all passive index funds , and track a variety of benchmark indices, and can produce excellent long-term returns without much homework on your part. For example, the $1.55

Securities and Exchange Commission (SEC) has approved a handful of applications to launch exchange-tradedfunds (ETFs) reflecting the spot price of Bitcoin (CRYPTO: BTC) tokens. It's the only asset on this list that was converted from a mutualfund format instead of created from scratch last week.

December is a good time to rebalance your investment portfolio, make tax-management moves, and generally ensure you're in good shape for the next year. Several financial giants have filed the paperwork to create Bitcoin-based exchange-tradedfunds (ETFs). Let me be clear. There's more Bitcoin news on the way.

As exchange-tradedfunds (ETFs) and mutualfunds sell the deleted stocks to rebalance their tracking portfolios, the once-promising businesses tend to plummet into value stock territory. Combined, the three companies account for roughly 75% of cereal sales in the U.S.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content