This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Buyout firms have long relied on controversial loans backed by equity stakes to enhance fund returns, but growing investor criticism has triggered a slowdown, according to a report by Bloomberg UK. Many firms borrowed against their portfolio companies to sustain the private market boom while dealmaking dwindled.

This occurs when the value of bonds and shares of publicly listed firms decline, as they did recently, bringing down the total assets of a pensionfund. Canadian pensionfunds are among the largest private equity investors in the world. Denominator effect The first is what’s known as the “denominator effect.”

Our ambition is to democratise the rental market for students and other renters alike by leveraging our operational scale and delivering inspired intelligent design experiences at value,” Scape’s Carracher said.

It is not monolithic and includes such varied enterprises as pensionfund investment managers such as AIMCo , insurance companies, investment banks, broker dealers, hedge funds, mortgage investment companies – and still others. Those are the publicly traded asset classes that private credit is most comparable to.

Sarah Rundell of Top1000Funds recently interviewed Suyi Kim, Global Head of Private Equity at CPP Investments to go over what drives success at their giant PE portfolio: Suyi Kim, global head of private equity at CPP Investments manages quite possibly the largest private equity allocation in the world.

CDPQ's own public equities portfolio saw its performance "driven by growth stocks, as well as by large positions in Quebec companies, which performed well." The private equity portfolio was affected by interest rate hikes as well as by an increase in financing costs, which affected certain privatecompanies.

Michiel Willams of Net Zero Investor reports OMERS’ sustainability chief on why the C$127bn fund’s green investment spree will not slow down: OMERS, the defined benefit (DB) plan for municipal employees in Ontario, is increasingly positioning itself as one of Canada's greenest pensionfund investors. to sell its 24.5%

Moving into 2023, he set a goal of reducing the pension’s PE allocation to 18 percent within three years, primarily by selling companies and exiting fund stakes via the secondaries market. These professionals had been trained to spot top privatecompanies and PE funds, rather than to sell their investments.

They’re talking about asset management firms, in which public pensionfunds often have investments, supporting shareholder proposals meant to achieve social justice or climate objectives yet of dubious financial value. Let me begin by stating the only thing I can't stand more than left-wing drivel is right-wing drivel.

The company is still in talks with its shareholders about raising as much as £1 billion in fresh funds following a £500 million injection agreed last year. Its largest shareholder is Canadian pensionfund Ontario Municipal Employees Retirement System (Omers), which holds a nearly 32 per cent stake.

With the completed acquisition of Burgiss, MSCI can now provide additional clarity and transparency highly needed by investors across private and public assets in their portfolios. Our product lines are increasingly interconnected, which means our work in private assets reinforces our work in climate and vice versa. We are delevering.

“The renewable energy, telecommunications and transportation sectors, to which (the Caisse) has been exposed for many years, are significant vectors of performance,” the pensionfund said. In the first half of 2023, higher financing costs hurt the Caisse’s private-equity portfolio, which posted a return of 1.4 per cent. “In

I told him he acts like the ambassador of CDPQ to the outside world and in his role as Head of CDPQ Global and Global Head of Sustainability he meets with many different stakeholders across the private and public sector. He told me he tries to leverage the institution to form solid partnerships and add meaningful value.

00:08:30 The odd company that went bankrupt would need to get sold. But there wasn’t an active m and a business, there wasn’t a leveraged finance business. But there came to be, in certain situations, buyers that were bootstrap, buyers that were, we would call ’em today, they then leveraged buyout financiers.

00:05:21 [Speaker Changed] No income taxes for the company and, and 00:05:23 [Speaker Changed] Then Koch Industries, I I, I don’t think a lot of people realize one of the largest privatecompanies in the United States and maybe even the largest, they’re, they’re giant energy powerhouse. Oh, really?

The exposure you get in investment banking, I was a leveraged finance banker by background. CHABRAN: Maybe because I come from a leverage finance background, as I told you, I tend always to focus on the downside. I think it was a great training. I think we learned a lot. How do you look at those?

CPP Investments invests in private equity in two ways. The first is via direct investments, where it holds ownership stakes that vary from passive, minority positions, up to 100% control of privatecompanies. The second is through private equity funds run by private equity firms, such as KKR and Blackstone.

Ted Seides : Hedge funds often are quarterly liquidity, depending on the underlying. You get into a private equity or venture capital fund, now you’re generally talking about 10 to 15 years. Barry Ritholtz : Because you have to wait for that privatecompany to have some liquidity event to free up the cash.

So it used to be within private markets that you would find a good business, apply quite a bit of leverage to it, at least in the private equity business, and be able to make a pretty good return by buying good solid businesses as they are. Leverage levels have come down materially. LAYTON: Leverage levels have changed.

So the theory was that’s great that you’re providing a loan, but if you can co-invest with them and get the upside of partnering with some of the most successful private equity funds in the United States, you know, a great way to enhance your returns. KENCEL: So, now, leverage is lower. RITHOLTZ: Right.

Paula Sambo of Bloomberg reports Canada Pension Plan Investment Board joins startup at $100 million Reforestation Fund: Canada’s largest pensionfund has joined a project to produce carbon credits by planting more than 100 native tree species on degraded land in Brazil’s Amazon region.

Our private capital fund indices cover more than 13,000 funds that represent more than $11 trillion in AUM and we believe they can help us become a standard setter in private assets. MSCI already supplies carbon emission data on more than 60,000 privatecompanies and more than 7,500 private equity and private debt funds.

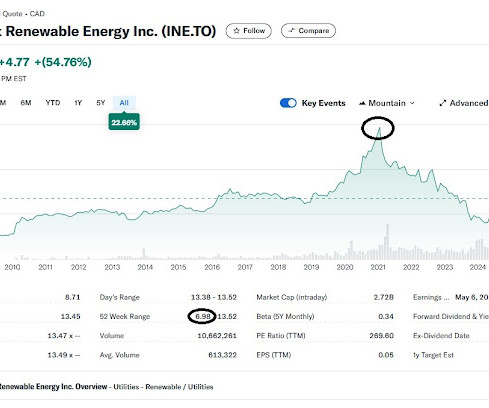

Nicolas Van Praet of the Globe and Mail reports pension giant Caisse strikes deal to acquire Innergex Renewable Energy: Canadian pensionfund giant Caisse de dpt et placement du Qubec has struck a deal to buy Innergex Renewable Energy Inc. The Caisse will pay $13.75

I think that private equity sees this as an opportunity, because they’re not really growing the institutional aspect of their business. Pensionfunds, perhaps, maybe aren’t growing as much as they need them to. MORGENSON: Well, these are privatecompanies, not the firms themselves.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content