This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Professional fund managers tend to be highly educated, hard-working, and extremely smart. But it doesn't take a highly complex trading plan to come out ahead of 98% of professional mutualfund managers over the long run. So, the odds are already against fund managers from the start. Image source: Getty Images.

And in an ironic twist, the less competitive you are, the better you'll be able to stick with a strategy that can lead you to after-tax returns that beat 98% of professionally managed mutualfunds. All you have to do is buy a broad-based index fund and hold it for years. That's why mutualfunds charge fees.

With a traditional 401(k), the more you put in, the more income you can potentially shield from taxes, up to the yearly IRS limit. First, by limiting you to investment funds, 401(k)s make it difficult to build a customized retirement portfolio. If you want to handpick a portfolio of stocks based on your own research, you can.

The emergence of spot Bitcoin exchange-traded funds (ETFs) has opened up a new avenue for investors to enter the cryptocurrency market without the complexities of managing crypto wallets and navigating exchanges. Fortunately for me, my full-time employer sponsors a tax-advantaged retirement account, and offers a contribution-matching program.

So if you want the option to retire at, say, age 52, then you'll need to keep some of your long-term savings outside of a tax-advantaged account. First, if you can't build your own stock portfolio, you give up control over your investments to some degree. Sure, you could choose one specific mutualfund over another in your 401(k).

If you contribute some of your earnings to an IRA, you can shield some income from taxes. They give you a limited penalty-free withdrawal to buy a home If you're funding an IRA to have savings down the line in retirement, then it's generally best to leave that money alone until retirement. IRAs allow you to buy stocks individually.

Would you like to diversify but also defer paying big capital gains taxes? But suddenly they find themselves sitting on an uncomfortably large percentage of their portfolio in a single name. The fund runs 15 ETFs and manages nearly 3 billion in assets. It gets to be a bigger, bigger percentage of your portfolio.

Minimize your investment fees Most 401(k)s give you a choice between a variety of mutualfunds or index funds your employer chooses. Most mutualfunds charge expense ratios , which are listed as percentages in your prospectus. However, your personal contributions are always yours to keep.

Create a diversified portfolio One of the easiest ways to build wealth is to create a diversified portfolio. Although some exposure to these stocks is OK, I'd encourage passive investors to opt for index funds that focus on broader growth markets such as cybersecurity, cloud computing, or artificial intelligence (AI).

They invest heavily in stocks and mutualfunds Baby boomers have the largest percentage of their wealth in stocks and mutualfunds. Many experts recommend subtracting your age from 100 to determine the percentage of your portfolio that should be in stocks.

Even if you add investments outside of retirement accounts, like individual stocks, bonds, and mutualfunds, 50% of American households have less than $9,000 invested. The IRA comes with tax incentives. For every dollar you contribute to a traditional IRA, you can deduct it from your tax return. That's a far cry from $1.46

Average 401(k) balance for 55 to 64 year olds Mutualfund company Vanguard crunches the numbers every year using data from its own clients. Don't undermine your eventual nest egg by underexposing yourself to growth and overexposing your portfolio to safer havens like bonds. investor stands. Ten years is a long time!

I've since contributed to those accounts every year, generally striving to max out my state's tax deduction over the course of a year. Until the need to spend the money in their accounts became clear, I invested those contributions in stock-based index funds. What stocks should you add to your retirement portfolio?

If you're really lucky, you could have the temperament to build and maintain a balanced and diversified portfolio, getting the best of both worlds. There's nothing wrong with dipping your first toe in Wall Street's waters through a low-cost exchange-traded fund (ETF). You don't have to pick a strategy right away.

The 401(k) is a cornerstone of retirement planning -- it's tax-friendly, hands-off, and convenient. Contributions to a traditional IRA may be deductible, and earnings grow tax-deferred until you take withdrawals in retirement. Contributions to a Roth IRA are made with after-tax money, and withdrawals are tax-free in retirement.

Over 91 million American households have already received a tax refund in 2024. Just 9% of Americans plan to invest their tax refund, according to a January survey from Bankrate. You don't need to be a genius to take your tax refund and turn it into a much more valuable asset. Should you invest your tax refund all at once?

Whatever your risk-tolerance is, your portfolio is probably intended to generate a certain amount of income every month, or at least every calendar quarter. Create a hypothetical, income-producing portfolio using the amount you've got saved up. That said, there are some tax implications to consider.

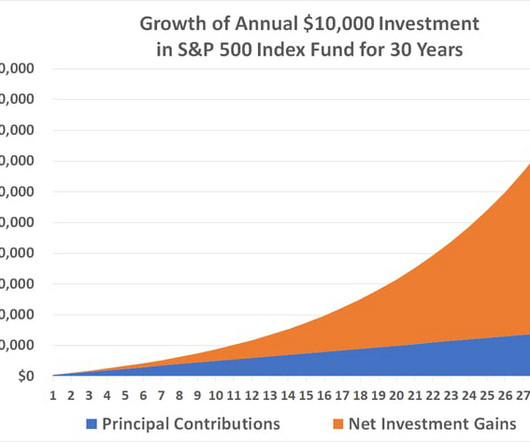

However, if you withdraw that $10,000 now, not only do you lose that potential growth, but you may also face early withdrawal penalties and taxes (which could be between 20% and 30%, depending on your tax rate), leaving you with only $7,000. thanks to compound interest.

At the Money: How to Pay Less Capital Gains Taxes (January 24, 2024) We’re coming up on tax season, after a banner year for stocks. Successful investors could be looking at a big tax bill from the US government. On this episode of At the Money, we look at direct indexing as a way to manage capital gains taxes.

You can also buy bonds through ETFs or mutualfunds. Funds are baskets of securities and can be a more accessible and affordable way to add bonds to your portfolio. There will be years when the market drops and your portfolio loses value. You can buy treasury bonds through a broker or directly from the government.

So if you, say, lose your job or face an unexpected medical bill, you are less likely to have to dip into your portfolio. REITs are companies that own and often manage a portfolio of income-producing properties. I hold a couple of REITs in my portfolio. But you might instead look to a gold ETF or mutualfund.

The program could increase its revenue by increasing tax rates or raising the payroll income tax cap. Investors should build a portfolio of stocks, bonds, mutualfunds, exchange-traded funds (ETFs), and other securities. There are a few different options to overcome the projected solvency issues.

Breathe Easier Next Tax Season with These Planning Strategies Every year, most of us smile when we see April 15th in the rearview mirror. The completion of our tax returns being filed marks the beginning of a nine month period where we don’t need to think about funny acronyms and form numbers.

The average 401(k) balance for retirees age 65 and older The data comes from mutualfund giant and retirement plan manager Vanguard. Between these two scenarios, investing $400 in the market every month for 25 years should result in a portfolio worth approximately $530,000. And yes, delaying retirement is one of those choices.

Exchange-traded funds, or ETFs, can be superb investing vehicles. ETFs are both cost- and tax-efficient, and they can instantly diversify a portfolio across a broad swath of the equity markets or within a specific sector/theme. The fund's popularity comes from its impressive performance.

But while there are clear benefits to funding a 401(k), you may not want to keep all of your retirement savings in one for a couple of good reasons. IRAs offer more investment options One downside of 401(k)s is that they generally limit you to investment funds, like index and mutualfunds , and do not allow you to invest in individual stocks.

Even for people at or over the age of 65, mutualfund company Vanguard reported that their clients' average 401(k) balance in 2022 stood at just a tad over $230,000. Last year's average contribution was on the order of 4.8%, according to mutualfund company and plan manager Fidelity. Over the past 15 years, 88% of U.S.

Tax-loss harvesting If you're an investor, you may already know that you might have to pay capital gains tax on profitable investments. What you might not know is that any investment losses can be used to help offset gains for tax purposes. This is known as tax-loss harvesting. Consider this example. Think of it this way.

Here's how I plan to retire as a millionaire and pay no taxes. Once it's open, you can contribute up to $7,000 in 2024, and the amount typically stays the same or rises every tax year. The beauty of that is you don't pay taxes on your distributions in retirement. By age 65, my portfolio should be worth approximately $1.6

This is why Peter Lynch, the legendary investor who crushed the market when running his mutualfund, Fidelity Magellan, has it as one of his top criteria when evaluating a stock. Here's why growth investors should consider both Remitly and Rocket Lab for their portfolios. Durable growth is a wonderful thing.

Image source: The Motley Fool/Upsplash There are many ways you can invest your money, from traditional options like stocks and mutualfunds to more recent options like cryptocurrency. Here's what it found and how to choose the right investments for your portfolio. These are a must, because they help you save on taxes.

Interval funds are closed-end investment companies that might appeal to investors looking for different ways to diversify their portfolio by providing access and exposure to illiquid strategies or alternative assets. In addition, you can purchase shares in an interval fund on a daily basis at NAV, similar to an open-end mutualfund.

And some plug-in hybrids can qualify for a pre-owned EV tax credit of up to $4,000 -- making them an even better deal for your budget and the planet. The biggest immediate impact on your personal finances from going solar is that the federal government is offering a generous tax credit for installing residential solar.

Generally, savers are advised to use tax-advantaged plans for retirement savings purposes because, well, they come with tax breaks. A traditional IRA or 401(k) lets you shield some of your income from the IRS by offering tax-free contributions. A Roth IRA or 401(k) gives you tax-free investment gains and withdrawals.

These things can definitely hurt your portfolio, but smaller, regular losses can also be hard on your retirement savings over time. For retirement savers investing things like mutualfunds or exchange-traded funds, you'll probably come across what's known as an expense ratio. Image source: Getty Images.

Market: The stock market is made up of thousands of choices and one easy way to gain exposure to it is via mutualfunds. Costs/Expenses : ETFs typically have lower expense ratios compared to mutualfunds. Tax Efficiencies : ETFs are generally more tax-efficient than mutualfunds.

A portfolio of stocks is going to do well over time. If your kid's 14 right now, don't put their college fund in the stock market. Robert Brokamp: The key there, remember with the IRA and it stands for individual retirement account, is that you get tax benefits by putting it into an IRA. I mentioned saving for college.

They allow you to save for retirement, while also saving on taxes. Your contributions are tax-deductible, and you only pay taxes when you withdraw your money in retirement. The great thing about IRAs (besides the tax savings) is that they let you buy almost any type of investment.

Mutualfunds have been a popular way to invest, but are they what’s best for your financial plan? Brian talks about what happens with a mutualfund, who has them, and what might be a better fit instead. According to Brian, mutualfunds are kind of like driving a 1987 Astrovan. What can you do about taxes? (6:01).

Compare this strategy with going the active route and giving your money to a mutualfund manager. And to add insult to injury, over a 10-year period, 85% of these funds lagged the S&P 500. This has the added benefit of deferring taxes until you sell the index fund, which is likely decades in the future.

These numbers also assume you'll continue adding money to your retirement fund in the meantime, and invest the bulk of it in the stock market. Mutualfund company T. times and six times your annual salary tucked away in a retirement fund by the time you're 50; the midpoint of that range is 4.75 So what's the number?

Between life's ordinary expenses like food, housing, and taxes, there's just not always much money left over from the average individual's annual income of around $41,000 (according to the Census Bureau), or the country's typical household income of just a little over $75,000 per year. That's easier said than done, especially these days.

Maximize your tax savings There are many types of accounts you can use to invest. Some of them help you save on taxes, so it usually makes sense to contribute to these first. With a traditional 401(k), you contribute pre-tax income, and you're taxed on withdrawals in retirement. You don't need to do this yourself.

From the fund's public market entrance in May 2015 to the end of 2020, the Grayscale fund averaged a 37% price premium over its holdings in pure Bitcoin (CRYPTO: BTC). Early Bitcoin adopters appreciated the Grayscale fund's availability in ordinary stock-exchange accounts. The mutualfund was converted into a proper ETF on Jan.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content